So, you’re trying to figure out the "magic number" for your retirement. Honestly, everyone wants to know exactly how much Social Security is going to land in their bank account every month. But if you've ever tried to look it up on the official government sites, it can feel like you're reading a manual for a 1980s VCR.

It’s confusing.

The short answer? For most of us, that check just crossed a pretty big milestone. In 2026, the average Social Security benefit for a retired worker officially hit $2,071 per month. That's up from about $2,015 last year, thanks to a 2.8% cost-of-living adjustment (COLA) that kicked in this January.

But "average" is a tricky word. You might get way more. Or, unfortunately, you might get less.

The $5,251 Unicorn: Who Actually Gets the Max?

You’ve probably seen headlines about the "maximum" Social Security benefit and thought, Hey, I want that. For 2026, the maximum monthly payout is a staggering $5,251. That is over $63,000 a year just from the government.

But here is the reality check: almost nobody gets it.

To see that $5,251 check, you basically have to be the perfect "Social Security student." You have to work at least 35 years. You have to wait until you are 70 to claim. And most importantly, you had to have earned the "taxable maximum" every single year for those 35 years. In 2026, that taxable maximum is **$184,500**.

Basically, if you didn't spend the last three decades making a high-end corporate salary, you’re not getting the unicorn check. And that’s okay. Most of us are living in the world of the average, which is still a vital safety net.

Why Your Check Might Look Different

Everything comes down to three main levers.

🔗 Read more: Who is Actually Running Coca-Cola? A Look at the Coca Cola Executive Team

The Age Lever This is the big one. If you claim at 62, the earliest possible age, you’re taking a massive permanent haircut on your benefits. If you turn 62 in 2026 and file immediately, your max possible benefit is only $2,969.

If you wait until your Full Retirement Age (FRA)—which is now 67 for everyone born in 1960 or later—that number jumps to $4,152.

Wait until 70? You get the "delayed retirement credits" of about 8% per year. That's why the difference between age 62 and age 70 is so drastic. It's essentially a choice between a smaller check now or a much bigger one later.

The 35-Year Math Social Security looks at your 35 highest-earning years. If you only worked 30 years? The SSA puts in five big, fat zeros for those missing years. That drags your average down significantly. If you’re at 33 years of work right now, staying in the workforce for just two more years can move the needle on your monthly payment more than you’d think.

The COLA Factor Every October, the Social Security Administration (SSA) looks at inflation (specifically the CPI-W) and decides how much to raise benefits for the next year. The 2026 increase of 2.8% was decent—it adds about $56 a month for the average retiree—but experts like those at The Senior Citizens League often point out that this doesn't always cover the actual rising cost of things like eggs, gas, or Medicare Part B premiums.

💡 You might also like: Dassault Systemes Share Price: Why Most Investors Are Missing the Big Picture

What About the "Other" Social Security?

We focus on retirees, but Social Security is a massive umbrella.

If you are looking at Social Security Disability Insurance (SSDI), the average check in 2026 is roughly $1,630. It’s lower than retirement because it’s based on your earnings up until the point you became disabled, and those are often interrupted years.

Then there is Supplemental Security Income (SSI). This is for people with very limited income and resources. For 2026, the maximum federal SSI payment for an individual is $994. It's not much, but for millions, it’s the difference between having a roof and not.

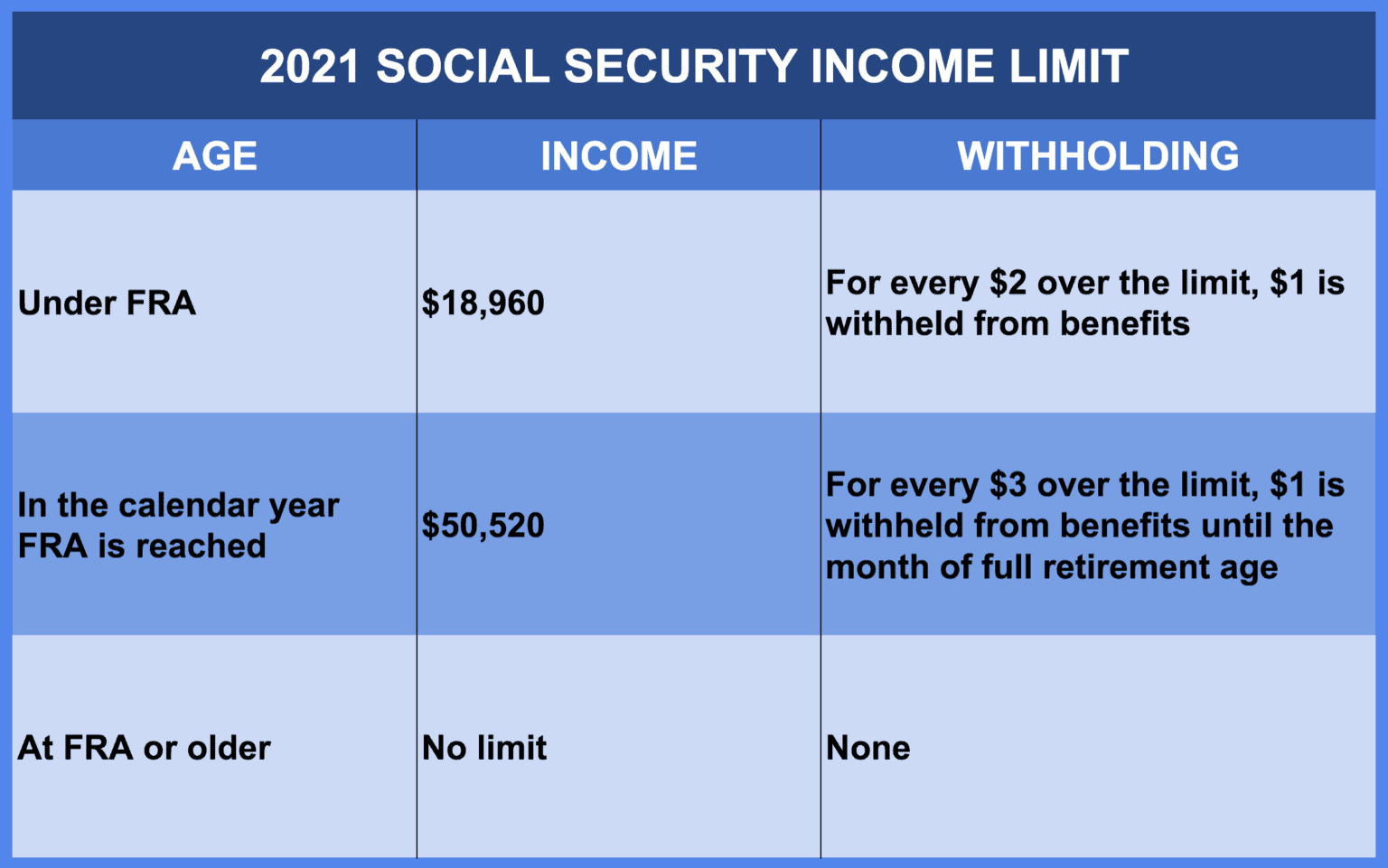

Real-World Earnings Test: The "Work" Trap

A lot of people think they can take their Social Security at 62 and just keep working their full-time job. You can... but it’s gonna cost you.

📖 Related: Trump Tax Plan Calculator Explained: How New 2026 Rules Change Your Paycheck

In 2026, if you are under your Full Retirement Age and you earn more than $24,480, the SSA will hold back $1 of your benefits for every $2 you earn over that limit.

They don't keep it forever—they eventually give it back to you once you hit 67—but it can be a nasty surprise when your January check doesn't show up because you earned too much at your part-time gig at the hardware store.

How to Get Your Actual Number

Stop guessing. Seriously.

Go to SSA.gov and set up a "my Social Security" account. They have a "Quick Calculator" and more detailed tools that pull your actual earnings history. It will show you three bars: what you get at 62, 67, and 70.

Seeing the actual gap between $1,800 a month and $3,100 a month usually changes how people think about their retirement date.

Actionable Next Steps

- Check your 35-year count: If you have 34 years of work, staying one more year to replace a "zero" in your history is the easiest raise you'll ever get.

- Audit your earnings record: Login to your SSA account and make sure they didn't miss a year of your income from 2005. Mistakes happen, and it’s your job to catch them.

- Calculate your "Gap": If your estimated benefit is $2,100 but your monthly bills are $3,500, you need to know that now so you can beef up your 401(k) or IRA contributions while you're still working.

- Factor in Medicare: Remember that Medicare Part B premiums are usually deducted directly from your Social Security check. Your "net" pay will be lower than the number on your statement.

The 2026 numbers show a program that is still a bedrock of American life, but it’s a bedrock you have to understand to actually use it correctly. Knowing how much Social Security you'll get isn't just about the check—it's about the math of your life.