If you look at the U.S. Treasury’s official ledger right now, the number is staggering. As of mid-January 2026, the US national debt is roughly $38.43 trillion.

It’s a figure that feels fake. How do you even wrap your head around twelve zeros? Honestly, most people can't. If you tried to count to 38 trillion, one second at a time, it would take you about 1.2 million years. We’re talking about a mountain of IOUs that has grown by more than $2.25 trillion in just the last twelve months.

Every single day, the balance grows by about $8 billion.

That’s not a typo. $8,000,000,000. Every. Single. Day.

Basically, the government is spending money it doesn’t have, and it’s doing so at a pace that has economists, politicians, and regular folks at the grocery store getting kinda nervous.

How Much Is The US National Debt Today and Who Do We Owe?

When we talk about how much is the us national debt today, we aren't just talking about one big credit card bill. It’s actually split into two main buckets that are worth looking at if you want to understand the "why" behind the crisis.

💡 You might also like: Dealing With the IRS San Diego CA Office Without Losing Your Mind

First, you have Debt Held by the Public. This is currently sitting around $30.81 trillion. This is the debt owned by individual investors, pension funds, the Federal Reserve, and foreign governments like Japan and China. When you buy a US Savings Bond for your nephew’s birthday, you are technically a part-owner of the national debt.

Then there’s the Intragovernmental Holdings, which is about $7.62 trillion. This is basically the government borrowing from itself. For years, the Social Security trust fund and Medicare trust funds had more money coming in than going out, so the Treasury "borrowed" that cash to pay for other things, leaving behind a stack of special-issue bonds.

The Interest Trap

The real kicker isn't just the total amount; it’s the cost of keeping the lights on. Because interest rates have stayed higher than they were in the "free money" era of the 2010s, the US is now spending roughly $2.6 billion every single day just on interest payments.

In the 2026 fiscal year, net interest is expected to account for nearly 14% of all federal outlays. To put that in perspective, the government is now spending more on interest than it does on many major agencies combined. It has officially become the second-largest federal expense, trailing only Social Security.

Why the Debt Skyrocketed So Fast

A lot of people think the debt is a recent "spending spree" problem. Kinda, but it's deeper than that. We haven’t seen a budget surplus since the late 1990s. Since then, we've hit a series of "once-in-a-century" events that each cost a fortune.

📖 Related: Sands Casino Long Island: What Actually Happens Next at the Old Coliseum Site

The 2008 financial crisis required massive bailouts. Then, the COVID-19 pandemic hit, and the government pumped trillions into the economy to keep things from collapsing. More recently, 2025 saw a massive government shutdown that lasted over 20 days, which actually made the debt situation worse by stalling tax revenue and increasing the "catch-up" costs once the doors opened again.

Here is the breakdown of why the needle keeps moving:

- Tax Revenue Gaps: The government generally collects about 17% of GDP in taxes but spends over 23%.

- The Graying of America: As Baby Boomers retire, the cost of Social Security and Medicare naturally climbs.

- The Debt Limit Battles: We just saw a massive debt limit hike of $5 trillion in July 2025, raising the ceiling to **$41.1 trillion**. These battles often lead to market uncertainty, which can actually drive up the interest rates the government has to pay.

- Defense and Tariffs: While new tariffs in 2025 and 2026 have boosted customs duties revenue significantly—up nearly 300% in some months—that extra cash is still being outpaced by rising costs in national defense and healthcare.

What This Actually Means for You

You’ve probably heard people say the debt will "bankrupt our grandkids." While the US can’t really "go bankrupt" in the traditional sense because it prints its own currency, the debt still hits your wallet in subtle, annoying ways.

When the government borrows trillions, it competes with everyone else for capital. This can push up interest rates for your mortgage, your car loan, and your credit cards. It also creates a persistent "inflationary pressure." If the government has to print or borrow more to pay the interest on what it already borrowed, the value of the dollar in your pocket can start to feel a little thinner.

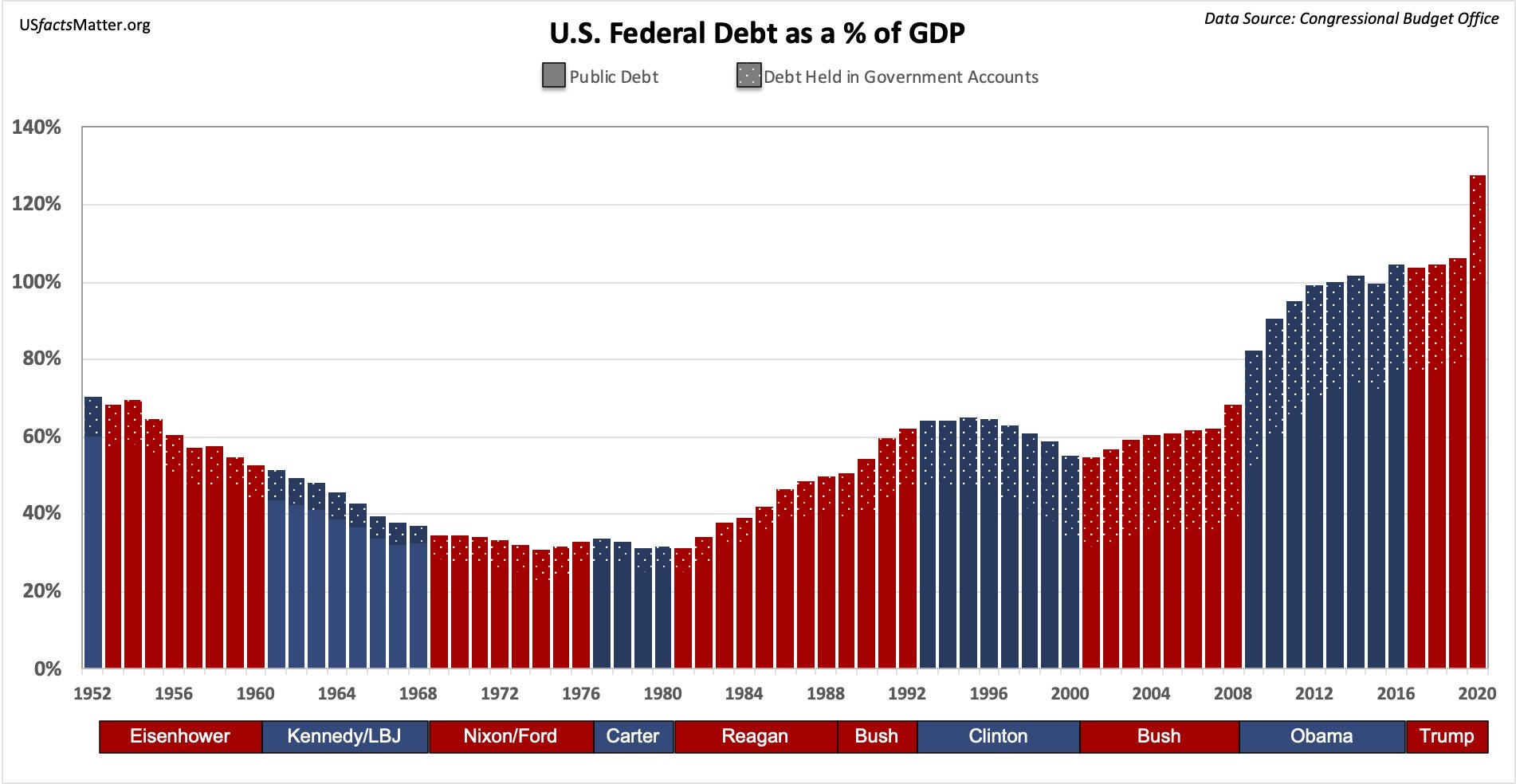

Currently, the debt-to-GDP ratio is roughly 124%. That means the country owes 24% more than the value of everything it produces in a year. Most economists agree that once you cross the 100% threshold, you’re in the "danger zone" where the debt starts to act like an anchor on economic growth.

👉 See also: Is The Housing Market About To Crash? What Most People Get Wrong

Actionable Insights: What Can You Do?

You can’t balance the federal budget yourself, but you can protect your own finances from the ripple effects of a $38 trillion debt.

1. Diversify your assets. Since a high national debt can lead to currency devalued over time, don't keep all your eggs in a standard savings account. Consider a mix of stocks, real estate, or even inflation-protected securities (TIPS).

2. Lock in fixed rates. If you’re planning on borrowing money for a home or a car, do it when rates dip. Floating-rate debt is dangerous when the government’s own borrowing costs are pushing the entire market's rates higher.

3. Watch the "Debt-to-the-Penny" updates. The Treasury updates these numbers daily. Staying informed helps you understand why the Fed might be raising or lowering interest rates, which directly affects your retirement portfolio.

4. Prepare for tax shifts. With the deficit for FY 2026 projected at $1.7 trillion, it’s highly likely that tax laws will continue to shift as the government looks for more revenue. Talk to a pro about tax-advantaged accounts like Roth IRAs to shield yourself from future hikes.

The national debt isn't going away anytime soon. In fact, we’re on track to hit $39 trillion by April 2026. Understanding the scale of the problem is the first step toward making sure it doesn't sink your personal financial ship.