Buying a home used to feel like a predictable rite of passage. You worked a decent job, saved up a bit, and the bank handed you a set of keys. Honestly, those days are gone. If you’re trying to figure out how much income to buy a house in the current market, you’ve probably realized the old "three times your salary" rule is basically dead. It’s been buried under a mountain of high interest rates and inventory shortages that have turned the housing market into a bit of a battlefield.

It’s frustrating.

You see a listing for $400,000 and think, "I make eighty grand, I should be fine." Then you run the numbers and realize that between the property taxes in your specific county and the current 6% or 7% interest rates, your monthly payment is suddenly half your take-home pay. That’s where the math gets messy.

The 28/36 Rule Is Your Starting Line

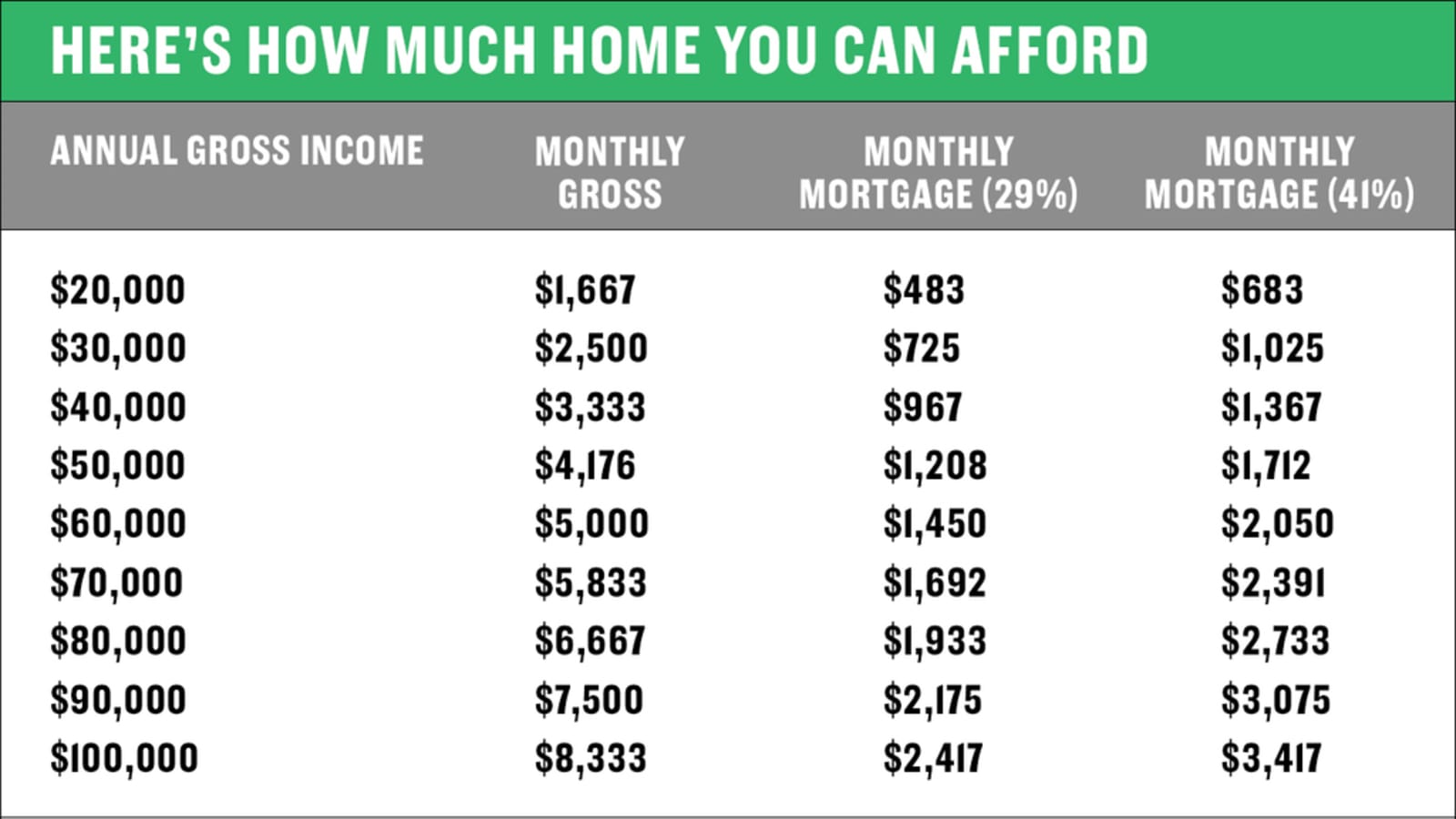

Banks are surprisingly rigid. Most lenders still lean heavily on the 28/36 rule, which is a fancy way of saying they don't want your house payment to exceed 28% of your gross monthly income. Your total debt—including that car note and the lingering student loans—shouldn't top 36%.

Let’s look at a real-world scenario. To afford a median-priced home in the U.S., which sits around $412,000 as of early 2026, you generally need an annual household income of roughly $110,000 to $120,000. That assumes a 10% down payment. If you're looking in San Jose or Boston? You’re easily looking at $250,000 plus. If you’re in an affordable pocket of the Midwest, maybe $65,000 gets you in the door. It’s all incredibly local.

You have to account for "the extras." Everyone forgets the extras.

Escrow is a silent killer. When you ask how much income to buy a house, you aren't just asking about the mortgage. You're asking about the $4,000 annual tax bill and the $1,800 homeowners insurance policy that just jumped 20% because of climate risks. In states like Florida or California, insurance alone can swing your "required income" by ten or fifteen thousand dollars a year.

Why Your Credit Score Changes the Income Math

A 640 credit score and a 760 credit score live in two different financial universes.

👉 See also: Sands Casino Long Island: What Actually Happens Next at the Old Coliseum Site

If you have a lower score, the bank sees more risk. They charge a higher interest rate. A 1% difference in your rate can add $250 to your monthly payment on a standard loan. To cover that extra $250 while staying under the 28% debt-to-income (DTI) cap, you actually need to earn about $10,000 more per year in gross salary. Basically, a good credit score acts like a virtual raise.

The "Hidden" Costs That Inflate Your Required Salary

Most online calculators are liars. They give you a "Principal and Interest" number that looks great, but it’s a fantasy.

You need to factor in:

- PMI (Private Mortgage Insurance): If you put down less than 20%, you're paying this. It's usually $50 to $150 a month.

- Maintenance: A roof doesn't care about your DTI ratio. If it leaks, it's $15,000. Experts like Elizabeth Renter from NerdWallet often suggest the 1% rule—set aside 1% of the home's value every year for repairs.

- HOA Fees: Some condos have fees that rival the mortgage itself.

If you’re looking at a $300,000 house, the 1% rule means you need $3,000 a year just for the "oops" moments. If your income is stretched to the absolute limit just to make the monthly payment, one broken HVAC unit becomes a life-altering financial disaster.

Debt-to-Income (DTI) Ratios: The Lender's Secret Sauce

Lenders look at your "Gross" income, which is your pay before taxes. This is a bit dangerous for you, the borrower. You don't live on gross income; you live on net income. If you live in a high-tax state like New Jersey, your take-home pay is significantly lower than someone in Texas making the same gross salary.

Banks might let you go up to a 43% or even 50% DTI for certain FHA loans. Just because they will lend it to you doesn't mean you should take it. Being "house poor" means you own a beautiful building but can't afford to buy a pizza or go to the movies. It’s a stressful way to live.

Location Is the Ultimate Variable

The answer to how much income to buy a house depends entirely on your zip code.

✨ Don't miss: Is The Housing Market About To Crash? What Most People Get Wrong

Take a look at the disparity:

In Cleveland, Ohio, you can often find solid homes for $200,000. With a decent down payment, an income of $55,000 to $60,000 might actually be enough to live comfortably.

Contrast that with Austin, Texas. Even with the recent market cooling, you likely need a household income hovering around $130,000 to $150,000 to shop in desirable neighborhoods without feeling the squeeze.

And then there's the "Secondary Market" effect. People are fleeing the most expensive cities and moving to "medium-cost" cities. This has pushed the required income up in places like Boise, Tampa, and Charlotte faster than local wages have grown. You’re competing with remote workers who brought their Silicon Valley or NYC salaries with them. It’s not a fair fight, but it’s the reality of the 2026 market.

Is the 20% Down Payment Still a Thing?

Not really. The average first-time homebuyer puts down about 6% to 8%.

This is a double-edged sword. Putting less money down means you keep your cash for emergencies, which is smart. But it also means your monthly payment is higher, which in turn means the income to buy a house needs to be higher to qualify. If you can scrape together a larger down payment, you lower the "income bar" you have to clear for the bank.

Real Income Strategies for the Modern Buyer

If the math isn't working, you have a few levers to pull. You can't magically make the Federal Reserve drop interest rates tomorrow.

First, look at the "Co-Borrower" option. We’re seeing a massive spike in "unmarried co-buying"—friends or siblings teaming up to combine their incomes. It’s risky legally, but from a pure math perspective, it's often the only way for Gen Z or Millennials to hit that $120,000 income threshold.

Second, the "House Hack." If you buy a duplex or a home with an ADU (Accessory Dwelling Unit) and rent it out, some lenders will actually count a portion of that potential rental income toward your qualifying income. It’s a loophole that can help you afford more than your salary alone would allow.

🔗 Read more: Neiman Marcus in Manhattan New York: What Really Happened to the Hudson Yards Giant

Third, the "Buy Down." You can use "points" to lower your interest rate. You pay a bit more upfront at closing to get a lower rate for the life of the loan. If you're $200 over your DTI limit, buying down the rate might be the thing that gets your application approved.

Don't Trust the Pre-Approval Letter Blindly

A bank might tell you that you're pre-approved for $500,000.

That is not a suggestion. It is a limit.

They don't know that you like to travel, or that you have a child who needs expensive daycare, or that you’re planning to buy a new car in two years. You have to do your own "lifestyle audit." Subtract all your expenses from your take-home pay. Whatever is left over—minus a cushion for savings—is your actual mortgage budget.

Actionable Steps to Determine Your Number

Stop guessing. If you want to know exactly how much income to buy a house in your specific situation, follow these steps:

- Calculate your "Real" DTI: Add up your car payment, minimum credit card payments, and student loans. Subtract this from 36% of your monthly gross income. Whatever is left is the absolute maximum the bank wants to see for a house payment.

- Get a localized quote: Call a local mortgage broker, not just a big national website. Ask for a "Total Monthly Payment" estimate on a specific house address. This includes the taxes and insurance for that specific neighborhood.

- Stress test the "What Ifs": If you lost your job or your spouse took a pay cut, could you still pay the mortgage for six months? If the answer is no, you might need a higher income—or a cheaper house—before pulling the trigger.

- Audit your "Debt Load": If you can pay off a $300/month car loan, you effectively "increase" your qualifying income by about $10,000 in the eyes of most lenders. Sometimes the best way to afford a house isn't making more money, it's owing less elsewhere.

- Check for Down Payment Assistance (DPA): Many states have programs for people making under a certain income (often up to 120% of the area's median income). These programs can provide $10,000 or more in grants, which lowers your loan amount and the income needed to support it.

The market is tough, sure. But it’s not impossible. It just requires a level of mathematical honesty that most people avoid. Know your numbers, ignore the "dream home" marketing, and buy the house that your actual paycheck—not your "future" paycheck—can afford.