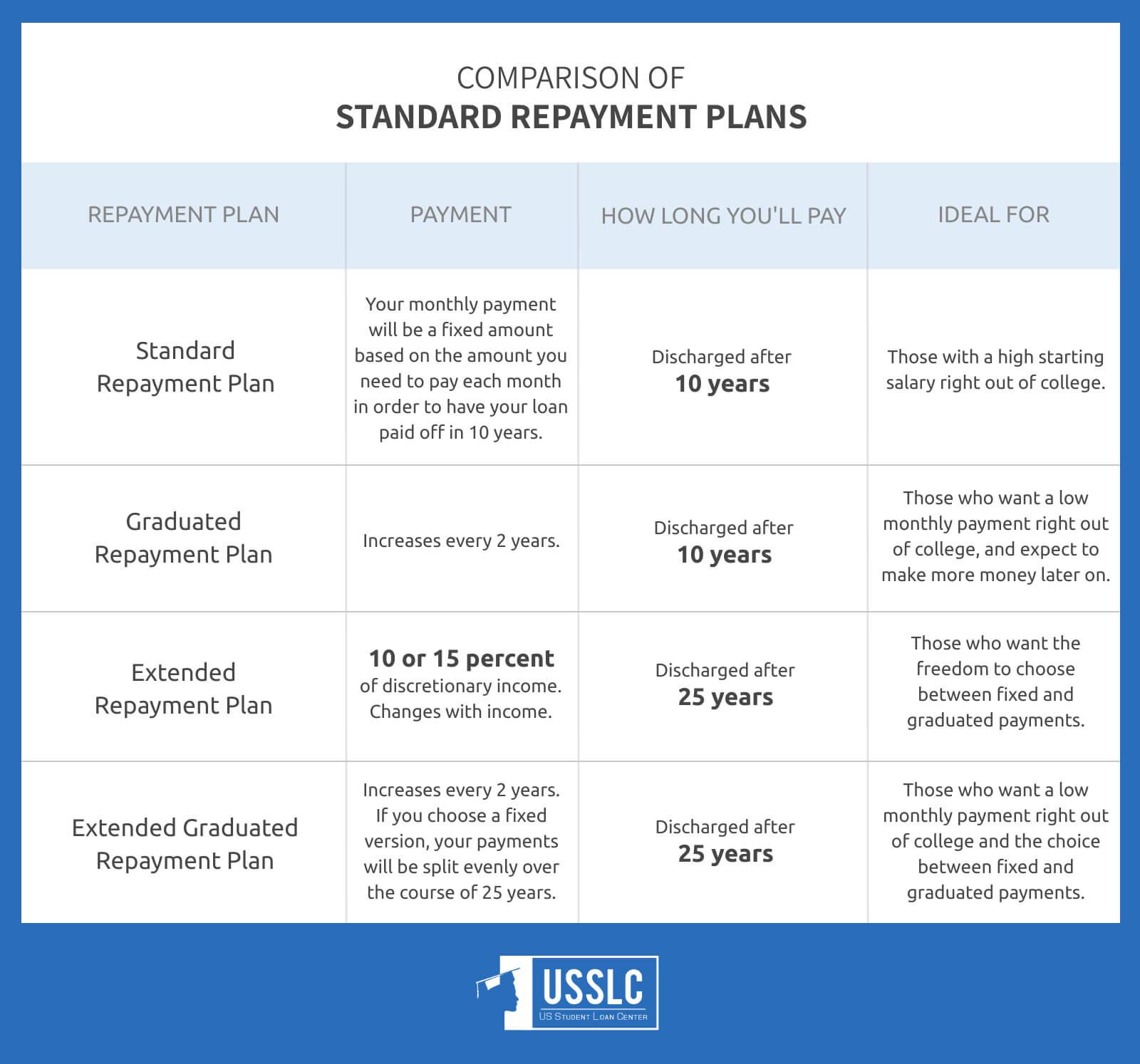

You sign the papers, grab the keys, and suddenly you're staring at a thirty-year sentence. It's daunting. Most people just assume they’ll be writing that monthly check until their hair turns gray and the kids have kids of their own. But the real answer to how long will it take to pay off home loan is rarely as simple as the date printed on your closing disclosure.

Mortgages are math problems designed to favor the lender. If you stick to the script, you’re looking at 360 months of payments. That is a long time. However, very few people actually stay in a loan for the full term. Life happens. People move, they refinance, or they get fed up with the interest and start throwing extra cash at the principal.

Honestly, the "standard" timeline is a myth.

The average American homeowner keeps a mortgage for only about seven to ten years before selling or refinancing. So, technically, the "loan" ends then, but the debt often just transforms into a new one. If we're talking about becoming truly debt-free, that’s a different beast entirely. You have to look at the amortization schedule—that depressing table where, for the first decade, almost every cent you pay goes toward interest rather than the house itself.

The brutal reality of the 30-year schedule

Most folks go for the 30-year fixed-rate mortgage because the monthly payment doesn't break the bank. It’s manageable. But here is the catch: you pay for that "affordability" with time.

If you have a $400,000 loan at a 6.5% interest rate, your monthly principal and interest payment is about $2,528. In the first month, $2,166 of that goes straight to the bank as interest. You only actually "own" $362 more of your house than you did the day before. It feels like running in sand.

How long will it take to pay off home loan if you just do the bare minimum? Exactly 30 years. Not a day less.

But wait. What if you chose a 15-year mortgage instead? The payment jumps up—in this example, to about $3,485—but you aren't just cutting the time in half. You’re slashing the total interest paid by hundreds of thousands of dollars. You're out of debt in 180 months. That sounds better, right? It is, but it also leaves you with less "wiggle room" if you lose your job or the water heater explodes.

Why the first five years feel like nothing is happening

Amortization is front-loaded. This isn't a conspiracy; it's just how the math of declining balances works. Because your balance is highest at the start, the interest (which is calculated as a percentage of that balance) is also at its peak.

As the years grind on, the balance drops, the interest portion shrinks, and the principal portion grows. It’s a snowball that takes forever to start rolling. If you’re asking how long will it take to pay off home loan, you have to realize that the "halfway point" of your loan—in terms of when you’ve paid off half the principal—doesn't happen at year 15 on a 30-year mortgage. It usually happens around year 22 or 23.

That is a tough pill to swallow.

📖 Related: Adani Ports SEZ Share Price: Why the Market is kida Obsessed Right Now

Hacks that actually move the needle

You don't have to be a victim of the schedule. There are ways to cheat the system that don't involve winning the lottery.

One of the most effective, albeit boring, methods is the bi-weekly payment strategy. Instead of paying once a month, you pay half your mortgage every two weeks. Because there are 52 weeks in a year, you end up making 26 half-payments. That equals 13 full payments instead of 12.

That one extra payment a year can shave about five to seven years off a 30-year mortgage.

Think about that. Just by changing the timing of your money, you can potentially stop paying your mortgage in year 24 instead of year 30. No lifestyle change required. Just a bit of administrative setup with your servicer.

Rounding up the "spare change"

If bi-weekly feels too complicated, just round up.

If your payment is $1,840, pay $2,000. That extra $160 goes directly to the principal. It doesn't seem like much, but on a $300,000 loan, that extra bit can kill the debt years earlier. It’s about reducing the base upon which interest is calculated. Every dollar you pay today is a dollar that can’t be charged interest for the next twenty years.

The "Recast" vs. Refinance debate

Sometimes people find themselves with a chunk of cash—a bonus, an inheritance, or a lucky day at the track. They want to know how long will it take to pay off home loan if they dump that cash into the mortgage.

You have two main options here:

- Refinancing: You get a brand new loan with a new term and a new rate. If rates have dropped since you bought, this is great. If rates have gone up, it's a disaster.

- Recasting: This is the hidden gem of the banking world. You give the bank a lump sum (usually $5,000 or more), and they "re-amortize" your existing loan. Your interest rate stays the same, and your end date stays the same, but your monthly payment drops significantly.

Wait, if the end date stays the same, how does this help?

If you recast to lower your payment, but continue paying the old, higher amount, you will absolutely demolish your mortgage timeline. You're effectively forcing the loan into a fast-forward mode.

👉 See also: 40 Quid to Dollars: Why You Always Get Less Than the Google Rate

When paying it off slowly is actually smarter

I know, I know. Being debt-free is the dream.

But sometimes, rushing to pay off a home loan is a bad financial move. We have to talk about "opportunity cost."

If your mortgage interest rate is 3% (shout out to the 2020-2021 buyers), and the stock market is averaging 7-10% over the long haul, every extra dollar you put into your mortgage is technically "losing" you 4-7% in potential gains. Plus, mortgage interest is often tax-deductible if you itemize.

Inflation also helps the borrower. If you have a fixed payment of $2,000 in 2024, that $2,000 will feel like a lot less money in 2044 because of inflation. You're paying back the bank with "cheaper" dollars.

So, if you ask a math nerd "how long will it take to pay off home loan," they might answer: "As long as humanly possible, because my money works harder elsewhere."

It depends on your stomach for risk. Some people sleep better knowing the bank doesn't own their roof. That peace of mind has a value that doesn't show up on a spreadsheet.

Real-world variables you can't ignore

Life isn't a calculator.

- Escrow changes: Your property taxes and insurance will go up. Your total monthly payment will rise even if your principal and interest stay the same.

- The "Move-Up" Trap: Most people pay off their loan by selling the house. Then they take the equity and buy a bigger house with a bigger loan. The clock resets to 30 years. This is why many people in their 50s still have 25 years left on a mortgage.

- PMI (Private Mortgage Insurance): If you put down less than 20%, you’re paying insurance that protects the bank, not you. Getting rid of this early doesn't necessarily shorten the loan, but it frees up cash you can then pivot toward the principal.

Calculating your specific exit date

To get a real answer, you need to use an amortization calculator with "extra payments" functionality.

Let's look at a $350,000 loan at 7%.

- Standard: 30 years. Total interest: $488,000 (yes, you pay for the house twice).

- Add $200 a month: You pay it off in 23 years and 10 months. You save $131,000 in interest.

- Add $500 a month: You pay it off in 18 years and 4 months. You save $248,000 in interest.

The difference is staggering.

✨ Don't miss: 25 Pounds in USD: What You’re Actually Paying After the Hidden Fees

Small, consistent additions are more powerful than occasional big chunks because they stop the interest from compounding earlier in the process. Time is your enemy here, so the sooner you start "overpaying," the more effective each dollar is.

The psychology of the "Burn the Mortgage" party

There is a movement—think Dave Ramsey or the FIRE (Financial Independence, Retire Early) community—that treats the mortgage like a house on fire. They suggest living on rice and beans to kill the debt in 5 to 7 years.

Is it possible? For a high-income earner with low expenses, absolutely.

But for most of us, the answer to how long will it take to pay off home loan is usually found in the middle ground. It’s the 15-to-22-year window. That’s the "sweet spot" where you still have a life, you still contribute to your 401k, but you aren't a slave to the bank for three decades.

Actionable steps to shorten your timeline

If you're tired of seeing that massive balance on your banking app, do these things in this order:

Check for prepayment penalties. Most modern residential loans don't have them, but you’ve got to be sure. Read your note. If there is a penalty for paying early, the math changes.

Automate an extra amount. Don't "wait and see what's left at the end of the month." There’s never anything left. Add $50 or $100 to your autopay specifically designated for "Principal Only."

Use "found money." Tax refunds. Work bonuses. That $50 your grandma sent for your birthday. If you aren't hurting for essentials, throw half of every windfall at the house.

Watch the rates. If rates drop significantly below your current rate, refinancing into a shorter term (like moving from a 30-year to a 15-year) can force you into a faster payoff while keeping the interest costs low.

Audit your escrow. Sometimes banks over-collect for taxes. If you get an escrow refund check in the mail, don't buy a new TV. Send it right back to the bank as a principal payment.

Ultimately, the clock is in your hands. The bank gives you a 30-year map, but you’re the one driving the car. You can take the scenic route and pay the full price, or you can take the shortcuts and keep more of your hard-earned money in your own pocket.

The best time to start was the day you closed. The second best time is today. Pay an extra $20 this month just to prove to the bank that you're the one in charge of the calendar. It feels surprisingly good.