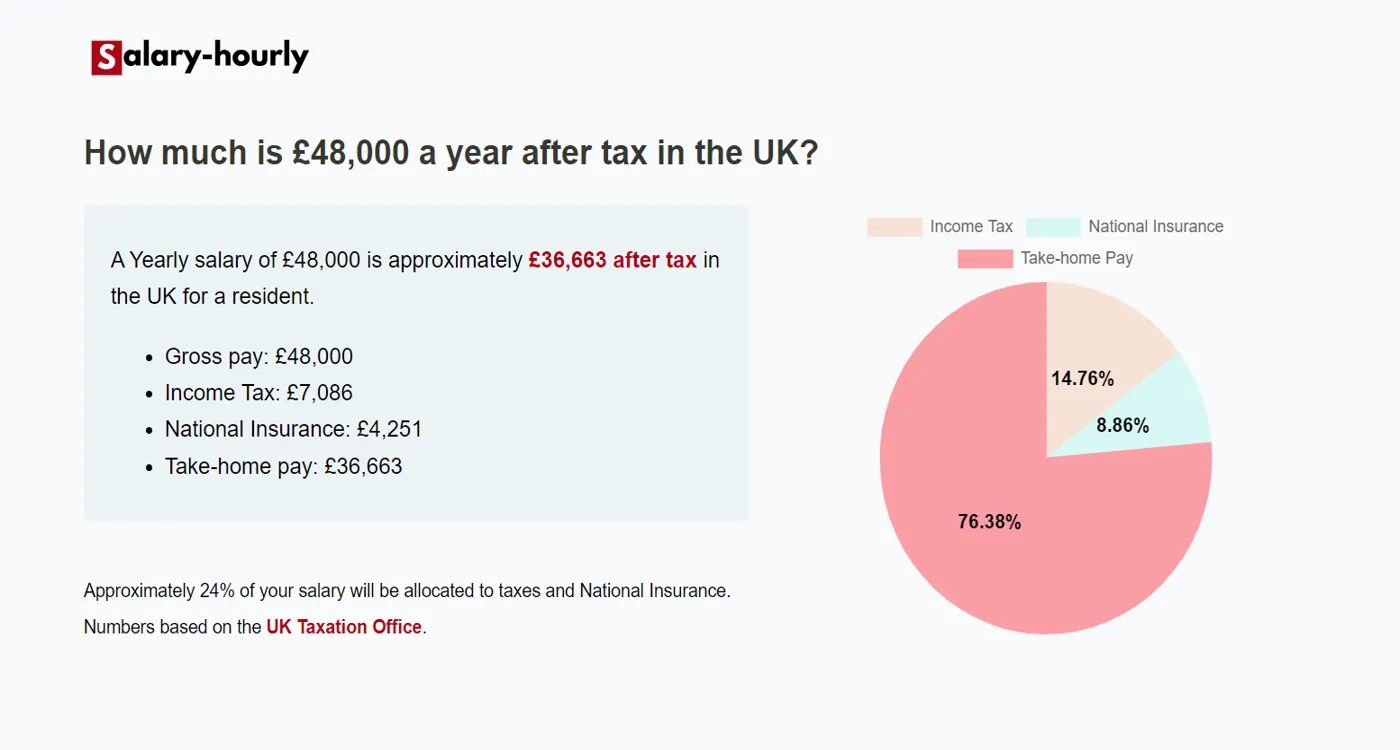

You’ve just landed a new job. The offer letter says £50,000. You’re thrilled. You start mentally spending that cash on a better flat or finally fixing the car. But wait. That £50k isn't what hits your Monzo account on the 25th. Not even close. If you don't use a salary calculator take home uk tool before signing that contract, you're essentially flying blind into a storm of National Insurance contributions and student loan repayments.

Most people think tax is simple. It isn't.

Between the Personal Allowance, various tax bands, and the ever-shifting goalposts of National Insurance (NI), your "gross" pay is just a theoretical number. It’s a starting point for a conversation with HMRC, and HMRC usually talks louder than you do. Understanding the gap between your gross salary and your net pay—the actual "take-home"—is the difference between financial peace of mind and an awkward conversation with your landlord because you miscalculated your budget by £400 a month.

Why Your Gross Pay Is a Total Lie

The UK tax system is built on layers. Think of it like a lasagna, but instead of delicious pasta, it’s made of deductions. For the 2025/2026 tax year, the standard Personal Allowance remains £12,570. This is the amount you can earn before the government takes a penny in Income Tax. But here’s the kicker: once you earn over £100,000, that allowance starts to disappear. For every £2 you earn over that threshold, you lose £1 of your allowance. This creates a "60% tax trap" that catches high earners off guard every single year.

It’s brutal.

Then there’s National Insurance. We’ve seen significant changes recently, with the main rate of Class 1 NI for employees being cut to 8% in previous budgets to ease the cost-of-living crisis. While that sounds great, it’s often offset by "fiscal drag." Because the tax thresholds are frozen while wages rise with inflation, more of your money gets pushed into higher brackets. You’re "richer" on paper, but the taxman is taking a bigger slice of the pie than he did five years ago.

The Student Loan Stealth Tax

If you went to university, you’re likely paying an extra "tax" that isn't called a tax. Depending on when you started your studies, you could be on Plan 1, Plan 2, Plan 5, or a Postgraduate loan. Plan 2 graduates—those who started between 2012 and 2023—pay 9% on everything earned over £27,295.

💡 You might also like: Class A Berkshire Hathaway Stock Price: Why $740,000 Is Only Half the Story

Combined with the 20% basic rate tax and 8% NI, a mid-career professional is effectively facing a 37% marginal tax rate.

That’s over a third of every extra pound you earn gone before you even see it. A salary calculator take home uk helps you visualize this. It’s one thing to know the percentage; it’s another to see £210 stripped from your monthly paycheck specifically for a degree you finished a decade ago. It changes how you view a £2,000 pay rise. Suddenly, it’s only an extra £100 a month in your pocket.

Is the extra stress worth it? Maybe. But you should know the number first.

Pension Contributions: The Good Kind of Deduction

Not all deductions are "thefts" from your paycheck. Most UK employees are now auto-enrolled into a workplace pension. Usually, you put in 5% and your employer puts in 3%. This is "free money," but it does lower your immediate take-home pay.

The beauty of pension contributions is tax relief. If you're a basic rate taxpayer, a £100 contribution only costs you £80 because the government adds the tax you would have paid back into your pot. If you’re a higher rate taxpayer (earning over £50,270), the deal is even better. You get 40% relief.

However, when you're looking at a salary calculator take home uk result, seeing that "Net Pay" figure drop because of a pension contribution can be scary. You have to weigh the long-term gain of a comfortable retirement against the short-term need for grocery money.

📖 Related: Getting a music business degree online: What most people get wrong about the industry

The Mystery of the Tax Code

Ever looked at your payslip and seen "1257L"? That’s the standard code. It tells your employer you get the full Personal Allowance. But sometimes, things go weird. If you have a company car, medical insurance through work, or you owe unpaid tax from a previous year, HMRC will change your code.

If your code is "K", it means your untaxed income is higher than your allowance. Essentially, your employer has to take more tax out because you’re already "in debt" to the system from other benefits. People often forget to factor these "Benefits in Kind" (BiK) into their take-home calculations. A "free" company BMW might end up costing you £300 a month in extra tax.

Real World Example: The £40k vs £50k Jump

Let’s look at a quick illustrative example.

Person A earns £40,000.

Person B earns £50,000.

On paper, Person B is £10,000 a year richer. That’s £833 a month.

But after Income Tax, National Insurance, and a standard 5% pension contribution?

Person A takes home roughly £2,580.

Person B takes home roughly £3,100.

👉 See also: We Are Legal Revolution: Why the Status Quo is Finally Breaking

The gap isn't £833. It’s about £520. If Person B also has a Plan 2 student loan, that gap narrows even further. This is why negotiating a salary based on the gross figure is often misleading. You aren't negotiating for £10,000; you're negotiating for an extra five hundred quid a month. When you realize that, your leverage in a meeting changes. You might realize you'd rather have an extra five days of holiday or a four-day work week instead of a marginal pay increase that gets eaten by the system.

Regional Variations: The Scottish Factor

If you live in Glasgow or Edinburgh, your salary calculator take home uk search is going to give you different results than if you live in London or Cardiff. Scotland has its own tax bands.

They have a "Starter Rate" of 19%, but they also have an "Intermediate Rate" of 21% and a "Higher Rate" of 42% (compared to 40% in the rest of the UK). Plus, the threshold for that 42% rate is lower than the 40% threshold in England. If you’re a high earner in Scotland, you are objectively paying more in tax. It’s a significant factor if you’re considering a cross-border move for work.

How to Optimize Your Take-Home Pay

You can't really "hack" the tax system, but you can be smart.

Salary sacrifice is the gold standard here. By asking your employer to take money out of your gross pay for things like electric cars, cycle-to-work schemes, or additional pension contributions, you lower your taxable income.

If you earn £52,000, you are just barely a higher rate taxpayer. By sacrificing £2,000 into your pension, you drop back into the basic rate band. You’re saving that 40% tax and keeping your full child benefit if you have kids (the High Income Child Benefit Charge starts to bite at £60,000 now, thanks to recent threshold increases).

Actionable Steps for Your Next Paycheck

Don't just wait for payday to see what happens. Take control of the numbers now.

- Check your current tax code: Login to your Personal Tax Account on the GOV.UK website. Ensure it reflects your actual situation. If it’s wrong, you’re either underpaying (and will get a scary bill later) or overpaying (and giving the government an interest-free loan).

- Run the numbers on any prospective pay rise: Before accepting a promotion, use a salary calculator take home uk tool to see the net impact. Factor in your specific student loan plan and pension percentage.

- Review your "Benefits in Kind": If your workplace offers a gym membership or private health insurance, check how much it's actually costing you in tax. Sometimes the "perk" is more expensive than buying it yourself with post-tax cash.

- Adjust your pension: If you can afford it, increasing your contribution by even 1% can have a massive impact on your tax efficiency, especially if you’re near a threshold like £50,000 or £100,000.

Understanding your take-home pay is the foundation of every other financial decision you make. Whether you're saving for a mortgage or just trying to survive the month, the gross number on your contract is just vanity. The net number in your bank account is the reality. Use the tools available to make sure you know exactly what that reality looks like before the month begins.