Money is weird. We talk about it constantly, yet almost nobody seems to agree on what a "normal" amount of it actually is. If you're scrolling through social media, you’d think everyone is either a billionaire or completely broke. Real life, though? It lives in the messy middle.

Household income in the United States isn't just a single number you can find on a chart and call it a day. It’s a moving target influenced by where you live, who you live with, and—honestly—how much the price of eggs has gone up this week.

The Number Everyone Quotes (But Rarely Understands)

According to the latest 2025 Census Bureau data reflecting 2024 earnings, the real median household income in the U.S. sat at $83,730.

That sounds specific. It feels official. But "median" is just the middle point. It means half the country is making more than that, and the other half is making less. It doesn't tell you that a family of four in San Francisco is struggling on $100,000 while a single person in Jackson, Mississippi, might be living like royalty on $70,000.

What's actually interesting is that while the "sticker price" of our paychecks went up, our actual purchasing power stayed pretty flat. Between 2023 and 2024, the median income didn't statistically budge once you adjusted for inflation. We’re essentially running on a treadmill—moving fast, but staying in the same place.

The Race and Ethnicity Gap

You can’t talk about American income without looking at the divides. It’s just the reality of the data.

- Asian households continue to lead the pack with a median income of roughly $112,800.

- Hispanic households saw one of the biggest jumps recently, climbing to $70,950.

- Black households actually saw a slight dip, landing around $56,490.

These aren't just dry stats. They represent different access to high-growth industries, varying levels of generational wealth, and the simple fact that some communities are getting hit harder by the "K-shaped" recovery we keep hearing about in 2026.

🔗 Read more: Philippine Peso to USD Explained: Why the Exchange Rate is Acting So Weird Lately

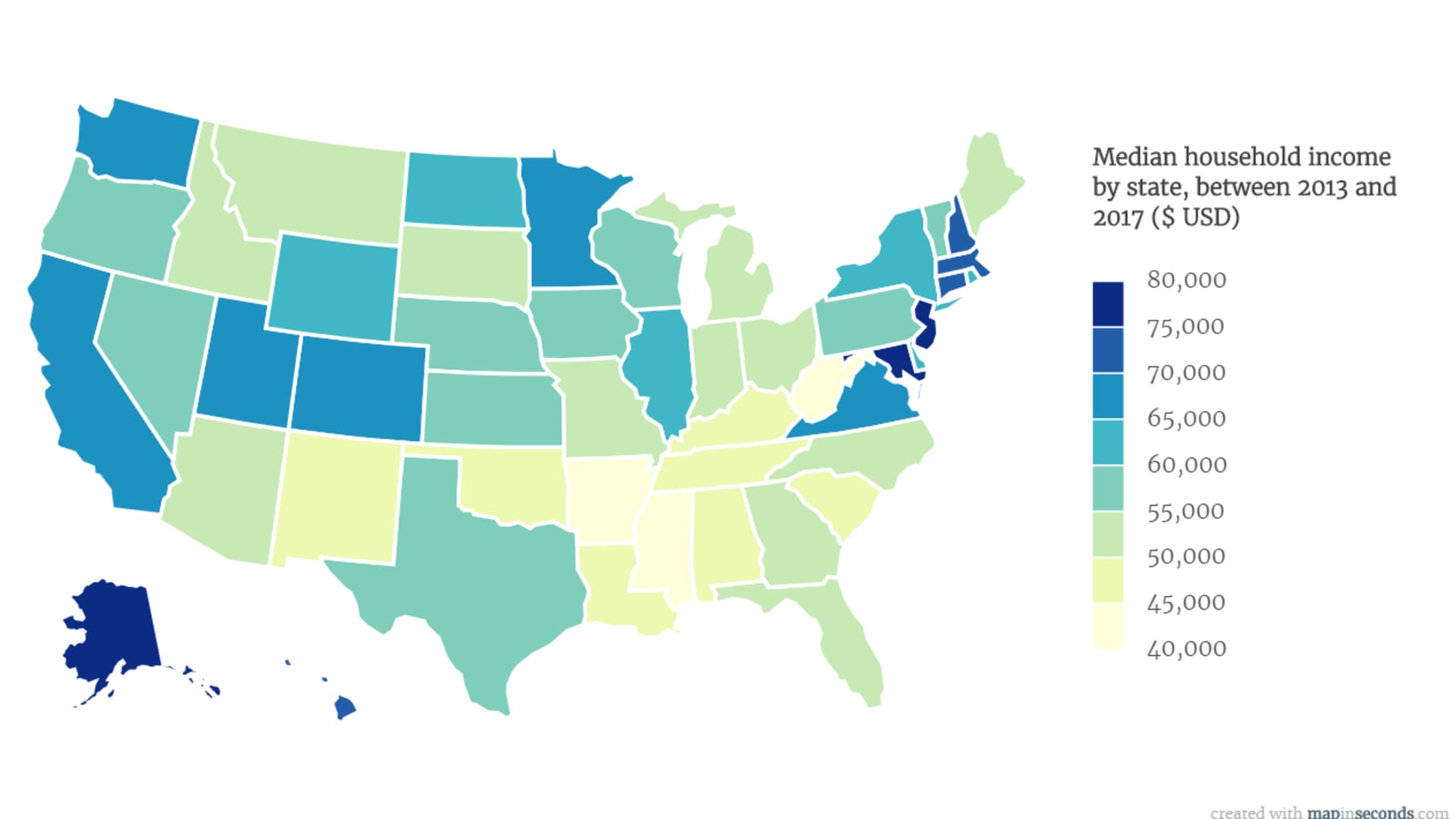

Where You Live is Your Financial Destiny

Honestly, your zip code might matter more than your degree. The geography of wealth in the U.S. is wild. If you look at the 2026 state rankings, the District of Columbia is in a league of its own with a median income of $150,381.

Compare that to Mississippi, where the median is hovering around $70,821.

That’s a $80,000 gap.

High-Income Strongholds vs. The Rest

If you want the big bucks, you head to the coasts. Massachusetts, New Jersey, and Maryland are all comfortably crossing the $120,000 threshold. But here’s the kicker: the cost of living in those places eats that "extra" money for breakfast.

I’ve met people in Boston making six figures who feel "house poor" because their mortgage is $4,500 a month. Meanwhile, someone in a "lower income" state like Arkansas or West Virginia might have a $900 mortgage and a boat in the driveway. The household income in the United States data looks great on paper for Jersey, but the vibe on the ground is different.

The 2026 "K-Shaped" Reality

We’re currently seeing a massive divergence. Economists call it a K-shaped economy. Basically, the top 20% of earners are doing great—their assets like stocks and homes are worth more than ever. They’re driving more than half of all consumer spending.

💡 You might also like: Average Uber Driver Income: What People Get Wrong About the Numbers

But then you look at the bottom 20%. They’re taking home only about 3.1% of the total national income. Many of these folks are living paycheck to paycheck, increasingly relying on credit cards and auto loans to get by. Delinquency rates are creeping up in 2026, which is a red flag that the "middle" is getting squeezed.

The AI Wildcard

Let’s be real: artificial intelligence is starting to mess with these numbers. We’re seeing "labor hoarding" in some sectors where companies are scared to let people go, but hiring has slowed way down. If you're in a job that AI can do, your income growth has likely stalled. If you're the one managing the AI, you're probably seeing a nice bump. This is creating a new kind of "digital divide" in our tax brackets.

Tax Bites and Take-Home Reality

Most people focus on the "gross" number—what’s on the offer letter. But that’s a trap.

The Census started tracking post-tax household income more closely because that’s what actually pays for groceries. In 2024, while the "gross" median was $83,730, the "post-tax" median was only **$72,330**.

That’s over $11,000 disappearing into the ether of federal, state, and payroll taxes before you even see it. And if you live in a high-tax state like New York or California? That gap is even wider.

The Gender Pay Gap: Still Stuck

It’s 2026 and we’re still talking about this. For full-time workers, the female-to-male earnings ratio actually fell recently to 80.9%.

📖 Related: Why People Search How to Leave the Union NYT and What Happens Next

It’s the second year in a row it’s gone down.

Why? It’s not just "discrimination" in a vacuum. It’s also about who is taking on caregiving roles as the cost of childcare skyrockets. When a daycare center in a mid-sized city costs $2,000 a month, many households decide it makes more "economic sense" for one parent (statistically the mother) to scale back. That shows up in the national income data as a massive lost opportunity.

Surprising Details You Might’ve Missed

- Social Security is a powerhouse: It moves nearly 29 million people out of poverty every year. Without it, the "bottom" of our income distribution would look like a total disaster.

- The Single-Person Factor: A huge reason some household incomes look low is that more Americans are living alone. A "household" of one naturally makes less than a "household" of two working professionals.

- The Education Premium: It’s still there, but it’s changing. Specialized trade skills are starting to outpace "generalist" master's degrees in terms of income growth in 2026.

Actionable Steps to Improve Your Position

You can’t control the Fed or the Census Bureau, but you can control your own "household economy."

- Check your "Real" Income: Don't look at your salary. Look at your purchasing power. If you got a 3% raise but inflation was 4%, you took a pay cut. Use an inflation calculator to see where you actually stand compared to five years ago.

- Audit Your Geography: If your job allows remote work, moving from a high-cost state to a mid-tier one can effectively give you a 20% "raise" without changing your paycheck.

- Upskill for the AI Shift: The data shows that income is concentrating in tech-adjacent roles. Even if you're in a traditional field like law or accounting, learning how to leverage automation is the only way to stay in the "top arm" of that K-shaped curve.

- Watch the "Post-Tax" Number: When considering a new job in a different state, use a take-home pay calculator. A $110,000 salary in Nashville often nets you more cash than $130,000 in Los Angeles.

The story of income in America isn't just about getting rich. It’s about not getting left behind as the landscape shifts under our feet.

To stay ahead, keep a close eye on your debt-to-income ratio, as 2026 is seeing a significant rise in credit-dependency among middle-earning households. Diversifying your income streams—whether through side hustles or investments—is no longer a luxury; it's a necessary hedge against a labor market that is becoming increasingly unpredictable. Understanding your local cost of living versus the national median will help you make more informed decisions about where to live and work in the coming years.