You've found the house. It has that weirdly perfect sunroom and a kitchen that doesn't look like it belongs in 1974. Now, you just need the bank to say "yes." Most people think the house loan approval process is a straight line from application to closing. Honestly? It’s more like a maze where the walls keep moving because your debt-to-income ratio shifted by 1% or a lender found a forgotten $200 credit card balance from college.

Lenders aren't just looking at your bank balance. They're looking at your life through a magnifying glass.

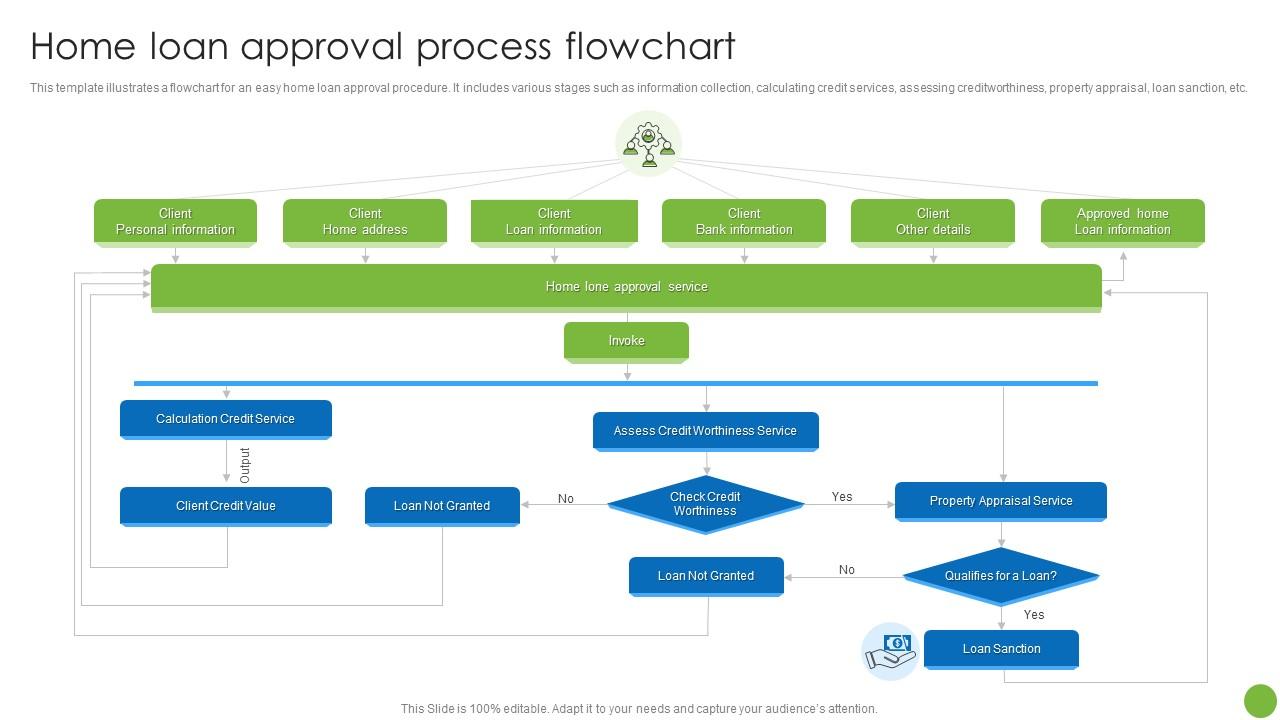

The reality is that mortgage companies are terrified of risk. Since the 2008 financial crisis, and more recently with the market volatility of the mid-2020s, the "rules" have tightened. Getting a "Pre-Approval" letter is basically just the warm-up. The real heavy lifting happens in underwriting, where a human—yes, an actual person—pokes holes in your financial history to make sure you aren't a walking liability.

Why Your Credit Score Isn't the Only Thing That Matters

Everyone obsesses over the 700 or 800 club. Sure, a high FICO score helps you snag a lower interest rate, but it won't save you if your "depth of credit" is shallow. A 780 score based on one credit card you’ve had for six months is worth way less to a bank than a 720 score backed by ten years of diverse history.

Lenders use a specific version of your score. Usually, it's FICO Score 2, 4, or 5. These are different from the "VantageScore" you see on free apps. They care about your Debt-to-Income (DTI) ratio more than almost anything else. If you earn $6,000 a month but your car payment, student loans, and new mortgage total $3,000, your DTI is 50%. Most conventional lenders start sweating once you cross 43%.

Some FHA loans allow for higher ratios, sometimes up to 56 or 57% in specific cases, but you'll pay for it in mortgage insurance. It's a trade-off. You get the house, but the monthly cost is steeper.

The Underwriting Black Box in the House Loan Approval Process

Underwriting is where dreams go to wait. Or die. This is the stage of the house loan approval process where a specialist verifies every single claim you made on your application. They will call your employer. They will look at two years of W-2s. They will scrutinize that $1,500 Venmo transfer from your aunt and ask why it's there.

If you can’t prove where a large deposit came from, they can’t use it toward your down payment. It’s called "sourcing and seasoning." Money has to sit in your account for at least 60 days to be considered "seasoned."

The Self-Employed Struggle

If you’re a freelancer or a small business owner, brace yourself. You are the "problem child" of the mortgage world. Lenders look at net income—what’s left after you’ve written off your home office, your car, and your "business" dinners. If you’re too good at taxes and bring your taxable income down to $30,000, the bank thinks you only make $30,000. It doesn't matter if your gross revenue was $150,000.

You’ll likely need two full years of tax returns. Some lenders offer "Bank Statement Loans" for the self-employed, where they look at your cash flow instead of tax returns, but these usually come with a higher interest rate. It's the price of flexibility.

The Appraisal Gap: The Great Deal Killer

You and the seller agreed on $450,000. Great. But the bank’s appraiser says the house is only worth $425,000.

This is the appraisal gap. The bank will only lend you a percentage of the appraised value, not the sale price. You now have three choices. One, the seller drops the price (rare in a hot market). Two, you walk away. Three, you come up with the $25,000 difference in cash.

💡 You might also like: Amazon Fulfillment Center Orlando FL: What Really Happens Inside the MCO1 and MCO5 Hubs

This is why "waiving appraisal contingencies" is such a dangerous game. It’s a gamble that the house is worth what you think it is. If you're wrong, your pockets better be deep.

Don't Buy a Fridge Yet

This is the most common mistake. You’re under contract. You’re excited. You go to a big-box store and buy $5,000 worth of appliances on a 0% interest credit line.

Stop.

Lenders pull your credit one last time right before closing. That new debt changes your DTI ratio. It can—and frequently does—get loans denied 24 hours before the keys were supposed to be handed over. Keep your credit "frozen" in time from the moment you apply until the moment you sign the final deed. No new cars. No new furniture. No new credit cards. Not even for a "10% off your first purchase" deal at a hardware store.

Real Steps to Get to the Finish Line

The house loan approval process doesn't have to be a nightmare if you treat it like a military operation. Documentation is your ammunition.

Gather the "Big Four": You need the last 30 days of pay stubs, the last 60 days of bank statements (every single page, even the blank ones), the last two years of W-2s, and the last two years of federal tax returns. If you have these ready in a digital folder before you even talk to a loan officer, you're already ahead of 80% of applicants.

The Paper Trail: If someone is gifting you money for a down payment, get a signed "gift letter" early. The donor will also have to show their bank statement proving they had the money to give. Some people find this intrusive. It is. But it’s required.

Letter of Explanation (LOE): If there’s a gap in your employment or a weird dip in your income from 2024, write a proactive letter. Explain it clearly. "I was transitioning between roles" or "I took time off for family medical leave." Underwriters are human; they just need a paper trail to justify the "risk" to their bosses.

Check Your Own Credit (The Right Way): Go to AnnualCreditReport.com. It’s the only site authorized by Federal law to give you a free report from all three bureaus. Look for errors. A "late payment" that was actually the bank's fault can take months to fix, so do this today.

Calculate Your "Cash to Close": It's not just the down payment. You have closing costs—usually 2% to 5% of the home's price. On a $400,000 house, that's an extra $8,000 to $20,000. If you don't have that sitting in a liquid savings account, the loan won't clear.

The process is tedious. It's invasive. But it’s the only way to secure what is likely the biggest investment of your life. Keep your finances boring, your paperwork organized, and your credit cards in your drawer.

Actionable Next Steps:

Start by calculating your DTI manually: divide all monthly debt payments by your gross monthly income. If you're over 40%, spend the next three months aggressively paying down small balances like credit cards or personal loans before applying. This "cleans up" your profile and can significantly lower the interest rate you're offered, saving you tens of thousands of dollars over the life of the loan.