You’ve probably heard your parents or grandparents brag about it at Thanksgiving. They lean back, sip their coffee, and tell you how they bought their first house in 1981 while staring down an 18% interest rate. It sounds like a horror story. Honestly, it kind of was. But when you look at the historical interest rates mortgage timeline, you realize that the number on the paper is only half the story.

Context is everything.

In the early 1980s, the median home price in the U.S. was roughly $70,000. Today, we’re looking at figures that make that look like a down payment. If you're trying to figure out why your 7% rate feels heavier than their 18% rate, you aren't crazy. It’s a mix of math, inflation, and a very specific guy named Paul Volcker who decided to break the back of the American economy to save it.

The Great Inflation and the 18% Peak

The late 1970s were a mess. We had the energy crisis, gas lines that stretched around city blocks, and "Stagflation"—that nasty cocktail of stagnant economic growth and high inflation. By the time 1981 rolled around, the Federal Reserve was desperate. Paul Volcker, the Fed Chair at the time, pushed the federal funds rate to nearly 20%.

Mortgage rates followed.

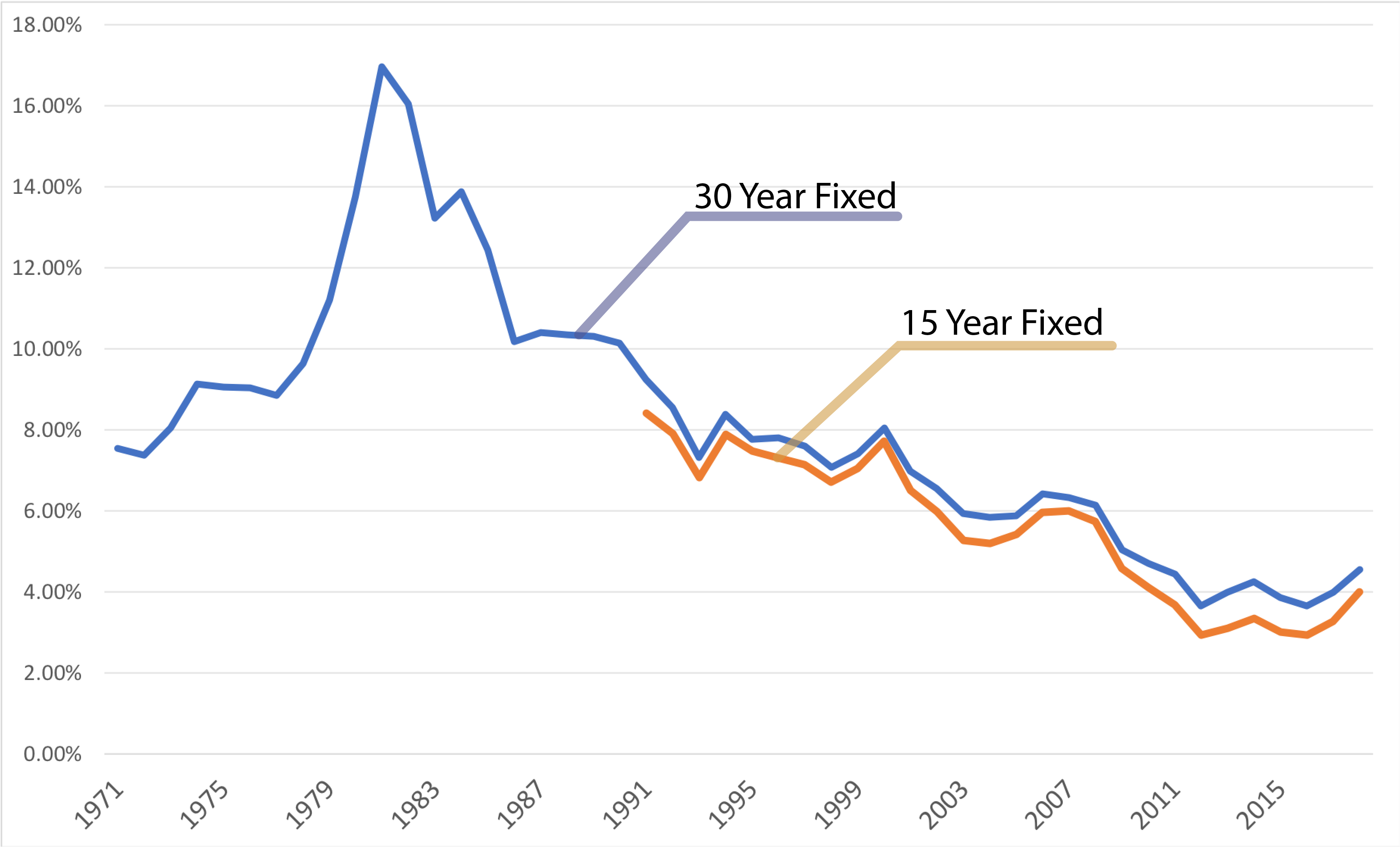

In October 1981, the average 30-year fixed mortgage hit 18.63%. Think about that. On a $100,000 loan, you were paying more than $1,500 a month just in interest, and that was back when $1,500 could buy you a fleet of used cars. People weren't exactly lining up to buy. Builders were sending wooden 2x4s to the Fed with "Help" written on them. It was a brutal era for housing, but it set the stage for a 40-year decline that we all eventually got addicted to.

Why did anyone buy a house then?

Well, many didn't. But those who did often used "seller financing" or "assumable mortgages." These are relics of the past that are starting to make a comeback now. Basically, a buyer would take over the seller's old 6% or 8% loan because the bank's new 18% rate was effectively a death sentence for a deal.

📖 Related: Target Town Hall Live: What Really Happens Behind the Scenes

The historical interest rates mortgage data shows that while rates were high, house prices stayed relatively flat because nobody could afford the payments. It was a standoff between the Fed and the American consumer. The Fed won. Inflation cooled. And then, the long slide down began.

The Long Slide: 1990 to 2010

By the time the 90s hit, we were seeing rates in the 10% to 7% range. This was the "sweet spot" for a long time. If you got a 7.5% mortgage in 1994, you felt like a genius. It was a period of relative stability. The economy was humming, the tech bubble was inflating, and the housing market was growing at a pace that felt sustainable.

Then 2008 happened.

The Great Recession wasn't caused by high rates—it was caused by bad loans and a "house of cards" financial system. To save the world from a total collapse, the Fed dropped rates to basically zero. This ushered in the era of the "3% mortgage."

The "Free Money" Trap

For over a decade, we lived in an artificial reality. Between 2010 and 2021, if you saw a mortgage rate above 5%, you thought it was high. In early 2021, the 30-year fixed rate hit an all-time low of 2.65%.

That is effectively free money.

👉 See also: Les Wexner Net Worth: What the Billions Really Look Like in 2026

When you account for inflation, the bank was practically paying you to take the loan. This created a massive distortion in the historical interest rates mortgage narrative. People began to view 3% as "normal" when, historically, it is a complete anomaly. According to Freddie Mac's primary mortgage market survey data, the long-term average for a 30-year fixed-rate mortgage since 1971 is actually closer to 7.7%.

We aren't in a high-rate environment right now. We are in a normal rate environment. It just feels high because we’re all suffering from a collective "low-rate hangover."

The Psychology of the "Lock-In" Effect

One thing the history books will talk about regarding the 2020s is the "Golden Handcuffs." Millions of homeowners are currently sitting on 2.5% or 3% rates. They want to move. They need a bigger backyard or a shorter commute. But they look at today's 7% rates and realize their monthly payment would double for the exact same house.

This has frozen the market.

Historically, when rates go up, prices go down. That isn't happening this time because nobody is selling. There is no inventory. We are in a weird stalemate where the past is preventing the future from happening.

Comparing Apples to (Very Expensive) Oranges

To really understand the historical interest rates mortgage landscape, you have to look at the Debt-to-Income ratio.

✨ Don't miss: Left House LLC Austin: Why This Design-Forward Firm Keeps Popping Up

- 1981: Mortgage rate was 18%. Median home price was about 3.5x the median household income.

- 2024: Mortgage rate is 7%. Median home price is about 6x or 7x the median household income.

This is why the "my parents did it, so can you" argument falls apart. Even though their interest rate was three times higher, the "entry fee" (the principal) was significantly lower relative to what they earned. Today, we have "moderate" rates on top of "extreme" prices. It’s a double-ended candle that’s burning the middle class.

What about the 5/1 ARM?

Adjustable Rate Mortgages (ARMs) have a spotty history. In the lead-up to 2008, they were the villain. People took "teaser rates" that exploded after two years, leading to mass foreclosures. But back in the 80s and 90s, they were just a tool.

If you think rates will go down in the next few years, an ARM might actually make sense. You're betting against the house. It's risky. But history shows that rates move in cycles. Nothing stays high forever, and nothing stays low forever.

How to Handle Today’s Market Using Lessons from the Past

Looking at the historical interest rates mortgage data isn't just a nostalgia trip; it gives us a blueprint for what to do next. If you are waiting for 3% to come back, you might be waiting for a very long time—maybe forever. That was a "once in a century" event triggered by a global pandemic and a financial meltdown.

Instead of waiting for the "perfect" rate, smart buyers are looking at the "Buy the house, marry the rate" strategy. It's a bit of a cliché, but there's truth in it. If you buy now at 7% and rates drop to 5% in two years, you refinance. If rates go to 9%, you look like a genius for locking in at 7%.

Actionable Steps for the Current Climate

- Check for Assumable Mortgages: Some FHA and VA loans are "assumable." This means you can literally take over the seller's 3% interest rate. It’s rare, and the paperwork is a nightmare, but it is the closest thing to a "time machine" in real estate.

- Focus on the Principal, Not the Rate: You can always change your interest rate later through refinancing. You can never change the price you paid for the house. If you can negotiate a lower price because high rates have scared off other buyers, do it.

- The 2/1 Buydown: This is a trick from the 1980s. The seller pays a lump sum to "buy down" your interest rate for the first two years. It gives you a breathing room while you wait for the market to settle.

- Ignore the Headlines: The media loves to scream about "record high rates." They aren't record high. They are average. If the payment fits your budget today, the "historical" context doesn't really matter for your personal checkbook.

The reality of the historical interest rates mortgage cycle is that it’s a pendulum. It swung too far toward 18% in the 80s, it swung too far toward 2% in 2021, and now it’s trying to find the middle again. The middle is uncomfortable, but it's where things are actually stable. Stop comparing your journey to a 1981 outlier or a 2021 fluke. Buy when you're ready, and keep an eye on the refi window. That's how the game is actually played.