You've probably heard the rumors that the "golden age" of high-interest savings is dead. Honestly? That's just not true. While the Federal Reserve spent the tail end of 2025 trimming back the benchmark rate, the hunt for the highest rates on CDs in 2026 has actually become more interesting, albeit a bit more competitive.

If you're sitting on a pile of cash in a "big bank" savings account earning 0.01%, you’re basically letting inflation eat your lunch. I'm looking at you, Chase and Wells Fargo.

👉 See also: What Happens If You Don't Pay Affirm: The Reality of Skipping Your Payments

Right now, as of mid-January 2026, the landscape is shifting. The Fed recently nudged rates down to a range of $3.5%$-$3.75%$, and most analysts—including the folks over at Goldman Sachs—expect a bit of a "wait and see" approach for the next few months. This creates a weird, beautiful window for savers. Banks are still hungry for your deposits to fund their loan books, but they know they can't keep those 5% rates forever.

The Heavy Hitters: Where the Rates are Hiding

You won't find the best deals at the branch down the street with the free lollipops. You’ve gotta look toward credit unions and digital-first banks. For instance, Connexus Credit Union is currently leading the pack with a 7-month special hitting 4.50% APY.

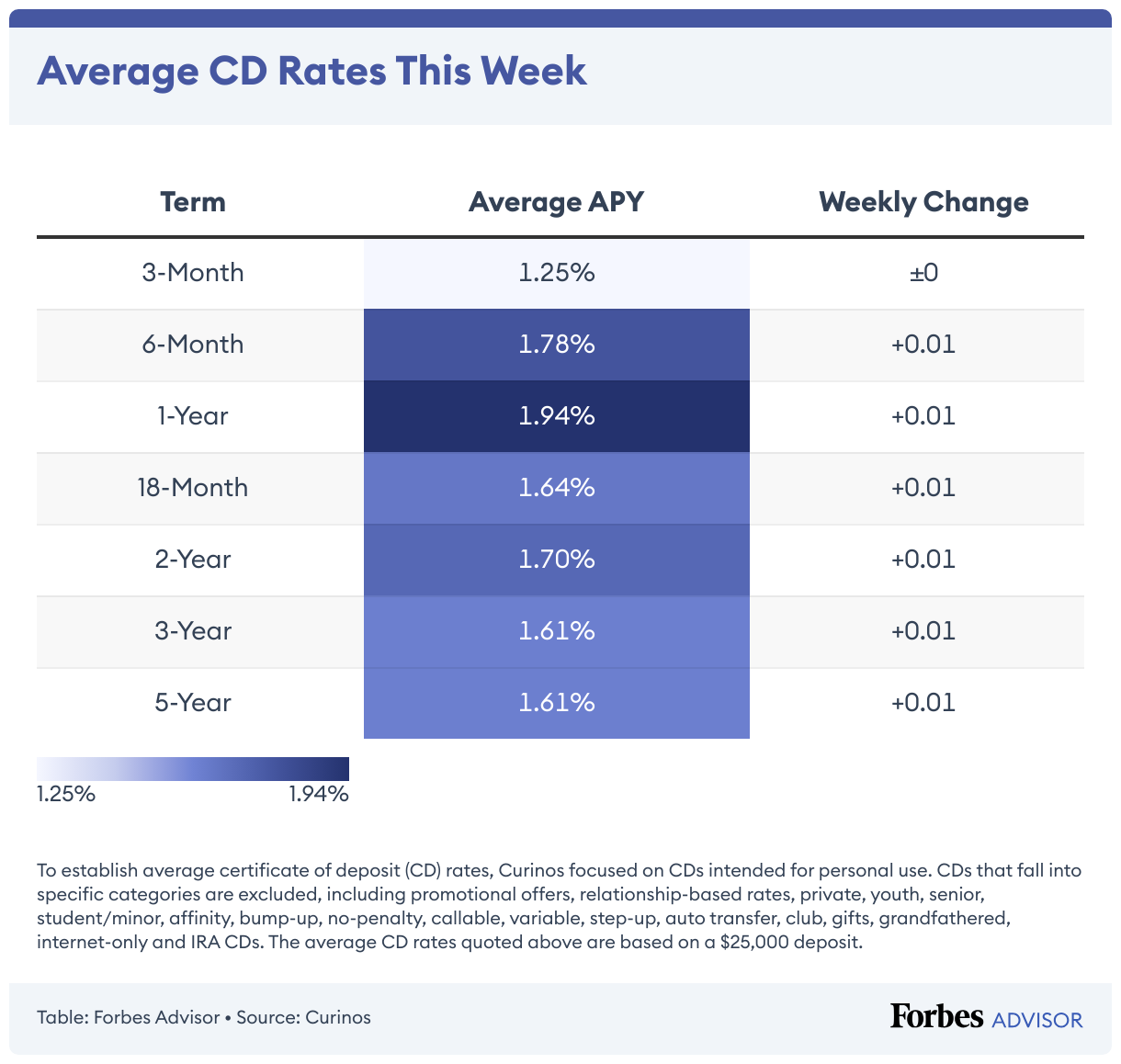

That is significantly higher than the national average, which is currently languishing around 1.63% for a standard 12-month term.

If you’re a fan of the traditional one-year lock-in, Genisys Credit Union is dangling a 13-month certificate at 4.16% APY. It’s a bit of an odd term length, I know. Banks love these "broken" terms (7 months, 13 months, 22 months) because they help them manage their liquidity profiles more precisely than a standard calendar year.

The "Slam Dunk" and Other Weird Promos

We are seeing some truly bizarre promotional products lately. Ardent Federal Credit Union recently launched what they call a "Slam Dunk CD." It starts with a base of 3.90%, but if the Villanova Wildcats win a home game, the rate jumps to 4.25% APY.

Is it a gimmick? Sorta. But if you’re looking for the highest rates on CDs, these are the types of rock-turning exercises you have to do.

Then there’s the Lynchburg Municipal Employees Federal Credit Union. They’re celebrating an anniversary with a 78-month CD (yes, 6.5 years) paying a whopping 6.50% APY. That is an incredible rate for 2026, but you have to be comfortable locking that money away until basically the next decade.

Why the "Highest" Rate Might Be a Trap

I'm gonna be real with you: chasing the absolute top number can sometimes bite you in the backside. Every CD comes with an "Early Withdrawal Penalty" (EWP).

Let’s look at Marcus by Goldman Sachs. They’re offering a solid 4.00% APY on a 12-month term. Great, right? But their penalty is 9 months of interest. Compare that to American Bank, which offers 4.05% APY but only charges 3 months of interest if you need to bust the account open early.

📖 Related: TJ Morris Ltd Home Bargains: What Most People Get Wrong

If life happens—and let's be honest, it usually does—that lower penalty is worth way more than a 0.05% difference in the annual yield.

The CD Ladder Strategy for 2026

Since the Fed is likely to stay steady or cut slightly more this year, the "ladder" strategy is basically the only way to play this. Don't dump your whole $50,000 into one 5-year CD.

If you do that and rates somehow defy the experts and go back up (hey, it's happened before), you're stuck. Instead, you split it.

- Put some in a 6-month CD at Climate First Bank (earning roughly 4.27% APY).

- Put some in a 1-year CD at Morgan Stanley Private Bank (4.10% APY).

- Put the rest in a longer 3-year or 5-year term to "lock in" the current yields before they drop into the 2% range.

This way, you have cash becoming available every few months. It gives you "dry powder" to reinvest if a better deal pops up.

Credit Unions: The Secret Sauce

Most people think you have to be a teacher or a firefighter to join a credit union. You don't. Most of the ones offering the highest rates on CDs—like Superior Choice or HUSTL Digital—allow anyone to join if they make a tiny donation ($5 to $15) to a specific non-profit.

It's basically a "pay-to-play" entry fee that pays for itself in about two weeks of earned interest.

Brokered CDs vs. Bank CDs

If you have a Fidelity or Vanguard account, you might see "Brokered CDs" on your dashboard. These are different animals.

- Pros: You can sell them on the secondary market without a fixed bank penalty.

- Cons: If interest rates go up, the value of your CD down if you try to sell it early.

Honestly, for most people reading this, stick to the direct bank or credit union CDs. They’re simpler, FDIC/NCUA insured up to $250,000, and you don’t have to worry about market fluctuations.

Real-World Math: Is it Worth It?

Let's do some quick math. If you put $25,000 into a "big bank" savings account at 0.01%, you earn $2.50 in a year. That won't even buy you a cup of coffee in most cities anymore.

🔗 Read more: CD Rates Credit Unions: Why Your Bank Is Probably Ripping You Off

If you put that same $25,000 into the 4.50% APY offer from Connexus, you're looking at over **$1,125** in interest.

That’s a car payment. That’s a flight. That’s a significant chunk of a mortgage payment.

What to Watch Out For

Watch the "Auto-Renewal" clause like a hawk. Banks love to lure you in with a high "special" rate, say for 7 months. When that 7 months is up, they will automatically roll your money into a "standard" CD that might only pay 0.50%.

They're betting on you being lazy. Don't be lazy. Set a calendar alert for 10 days before maturity.

Actionable Next Steps

To actually snag the highest rates on CDs today, here is your playbook:

- Check your current yield. If it’s under 3.5%, you’re losing.

- Look at the "Broken Terms." Search for 7, 9, or 13-month specials. These are where the marketing budgets are spent.

- Verify the Insurance. Ensure the institution is FDIC (banks) or NCUA (credit unions) insured.

- Join the ACC. Many credit unions require membership in the American Consumer Council. It usually costs about $15 and unlocks those 4%+ rates.

- Calculate the EWP. Before you click "open," know exactly how many months of interest you lose if you withdraw early. If it's more than 6 months for a 1-year CD, keep looking.

The market isn't going to wait for you. These 4% and 5% handles are likely the highest we'll see for the next couple of years as the economy "normalizes." If you have the cash, now is the time to lock it down.