Investing in mid-caps is usually a wild ride. You expect high adrenaline, sharp turns, and maybe a bit of motion sickness. But then you look at the HDFC Mid Cap Opportunities Fund, a behemoth in the Indian mutual fund space, and things feel... different. It's like finding a heavy-duty SUV that somehow maneuvers like a sports car.

Honestly, the sheer size of this fund should be a problem. Usually, when an equity fund hits nearly ₹93,000 crore in assets under management (AUM), it starts getting sluggish. It becomes hard for the manager to buy enough of a good stock without driving the price up himself. Yet, as of early 2026, this fund continues to be a staple in many long-term portfolios. It basically defies the "size is the enemy of performance" rule that most experts preach.

The Chirag Setalvad Factor

You can't talk about this fund without mentioning Chirag Setalvad. He’s been at the helm for what feels like forever—since 2007, actually. In an industry where fund managers jump ship every few years for a better paycheck, that kind of continuity is rare. It’s comforting. You know exactly how the fund will react when the market loses its mind.

Setalvad isn't a "momentum chaser." He’s not going to buy the latest "hot" stock just because everyone on social media is screaming about it. His style is more about "Growth at a Reasonable Price" (GARP). He looks for companies with solid balance sheets and actual cash flow. If a company is just a "cool idea" without a real business model, it probably won't find a home here.

This patience shows in the portfolio turnover ratio, which sits around 18% to 19%. Think about that. Most of the stocks in the fund have been there for years. He isn't trading; he’s owning.

What's Actually Inside the Portfolio?

If you peek under the hood as of January 2026, you'll see a heavy leaning towards Financial Services and Healthcare. These aren't exactly "get rich quick" sectors, but they are the backbone of the economy.

- Max Financial Services Ltd: A long-term favorite in the portfolio.

- The Federal Bank Ltd: Shows the fund's preference for stable, mid-sized private lenders.

- Balkrishna Industries: A play on the global agricultural and industrial tire market.

- Apollo Tyres: Another classic manufacturing bet.

The fund typically holds between 60 to 80 stocks. That might sound like a lot, but for a fund this big, it's necessary for liquidity. The top 10 holdings usually make up about 30% to 35% of the total assets. It's diversified enough to protect you if one company craters, but concentrated enough that the "winners" actually move the needle on your returns.

👉 See also: Bank of America Stock: What Most People Get Wrong About the 2026 Outlook

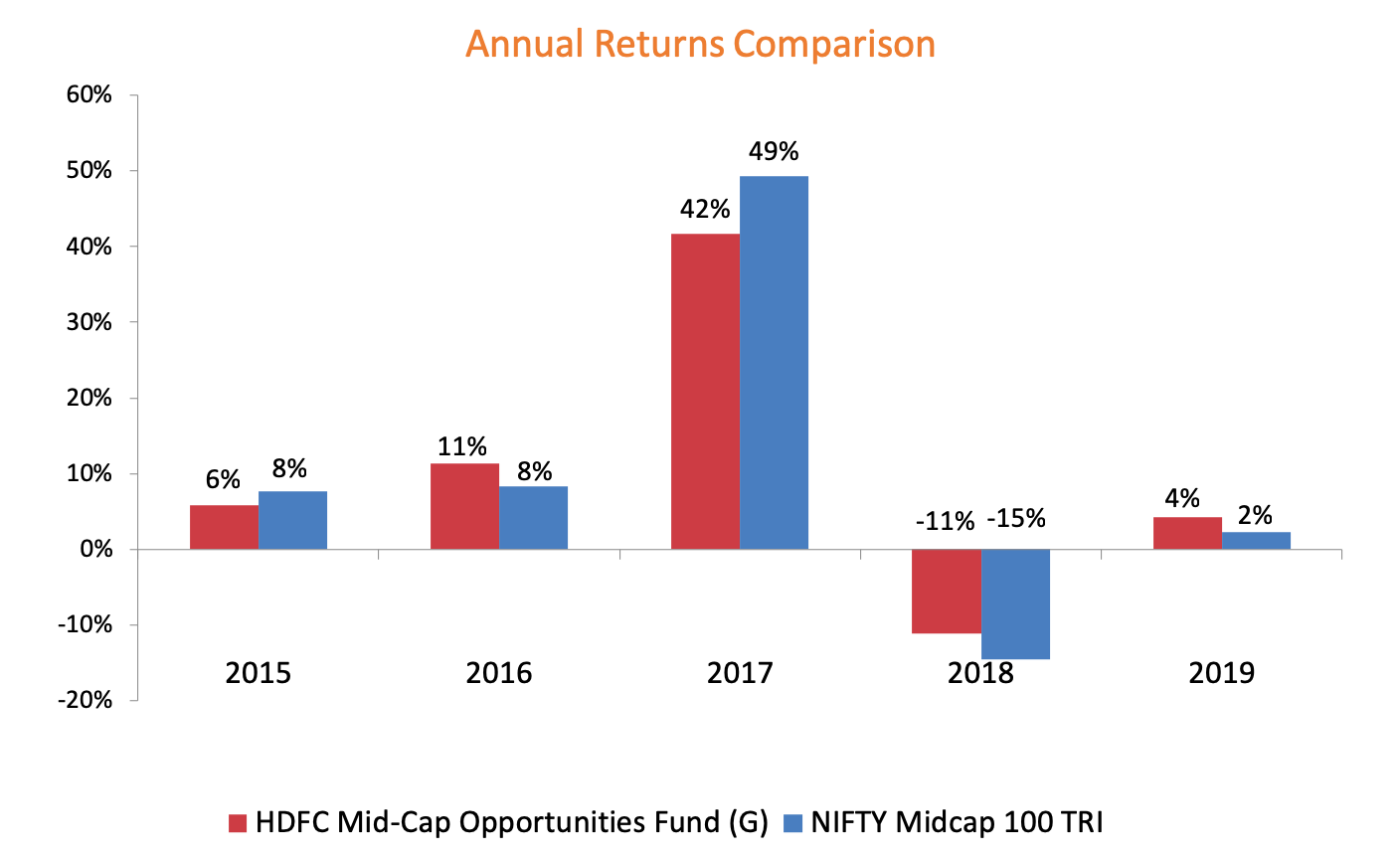

Does the Performance Justify the Hype?

Let’s look at the numbers, because at the end of the day, that’s why we’re here. The 3-year annualized returns for the Direct Plan are hovering around 25% to 26%. The 5-year returns are equally impressive, sitting near 24.5% to 25%.

Wait.

Compare that to the NIFTY Midcap 150 TRI benchmark. Historically, this fund has a knack for beating its benchmark over 10-year periods. In the short term—like a single year—it might trail some "aggressive" or "quant-based" funds. That’s the trade-off. You’re trading the potential for a 60% "lucky year" for the high probability of a steady 18-20% over a decade.

The Reality of Risks in 2026

No investment is perfect. The "Very High" risk label on the riskometer isn't just a suggestion—it's a warning. Mid-cap stocks can drop 30% in a month if the global economy hiccups.

Liquidity is the elephant in the room. Because the HDFC Mid Cap Opportunities Fund is so massive, it can't exit small positions quickly. If there’s a massive market crash and everyone wants their money back at once, the fund might have to sell its best, most liquid stocks first to pay out investors. It hasn't happened yet, but it’s a structural reality you should acknowledge.

Also, keep an eye on the expense ratio. The direct plan is relatively cheap at around 0.72% to 0.74%, but the regular plan (if you're going through a broker) is significantly higher. Over 20 years, that 1% difference in fees can eat up lakhs of rupees. Seriously. Use the direct plan if you can manage it yourself.

Who Should Actually Buy This?

This isn't for the person who needs their money for a wedding next year. It’s just not.

This fund is for:

- The 10-Year Planner: Someone who is building a retirement nest egg.

- The SIP Devotee: The fund is tailor-made for Systematic Investment Plans. Since it's less volatile than its peers (it has a lower Beta of around 0.86), your monthly investments don't feel like a gamble.

- The "Core" Investor: Use this as the "mid-cap" slice of your portfolio, and pair it with a solid Large Cap or Index fund.

Actionable Next Steps

If you're thinking about jumping in, don't dump a massive lump sum in all at once. Even with "reasonable" valuations, mid-caps are pricey right now.

- Start a SIP: Even ₹500 or ₹1,000 a month is enough to get skin in the game.

- Check Your Asset Allocation: If you already have 50% of your money in mid and small caps, adding more here might make your portfolio too "top-heavy" with risk.

- Choose the Direct Growth Plan: Avoid the IDCW (Income Distribution cum Capital Withdrawal) option unless you absolutely need the cash flow. The Growth option lets your money compound, which is where the real magic happens.

- Commit for 7+ Years: If you can't see yourself holding this through 2033, look at a Large Cap fund instead. Mid-caps need time to breathe and recover from the inevitable market dips.

The HDFC Mid Cap Opportunities Fund isn't the flashiest fund on the block anymore. It’s the "old reliable." In a world of "get rich quick" schemes and volatile new-age tech funds, there’s something to be said for a fund that simply does what it says on the tin. Just don't expect it to double your money overnight. Expect it to build wealth slowly, boringly, and consistently.