If you've ever looked at a gas pump and wondered why the price didn't drop even though the news said "oil is down," you're already touching the messy world of futures WTI crude oil. It's complicated. Honestly, it’s a bit of a circus. West Texas Intermediate, or WTI, is basically the heartbeat of the American energy market, but the way it’s traded through futures contracts is often misunderstood by anyone who isn’t sitting behind a Bloomberg terminal.

WTI isn't just "oil." It's a specific grade of light, sweet crude. "Light" because it’s low density and "sweet" because it’s low sulfur. This makes it a dream for refiners who want to turn it into gasoline. When we talk about futures, we aren't talking about buying a barrel of gunk to keep in your garage. We’re talking about a legal agreement to buy or sell 1,000 barrels of that gunk at a specific price, on a specific date, at a specific place—usually Cushing, Oklahoma.

The Cushing Connection and Why It Matters

Cushing is a tiny town in Oklahoma. You’ve probably never been there. Most people haven't. But in the world of futures WTI crude oil, it is the center of the universe. It’s the "Pipeline Crossroads of the World."

When a WTI futures contract expires on the NYMEX (New York Mercantile Exchange), physical delivery is supposed to happen in Cushing. This is where things get weird. Most traders—hedge funds, speculators, algorithms—have zero intention of ever touching a drop of oil. They just want the price movement. But because the contract is tied to a physical location with finite storage space, the price can do insane things when those tanks get full.

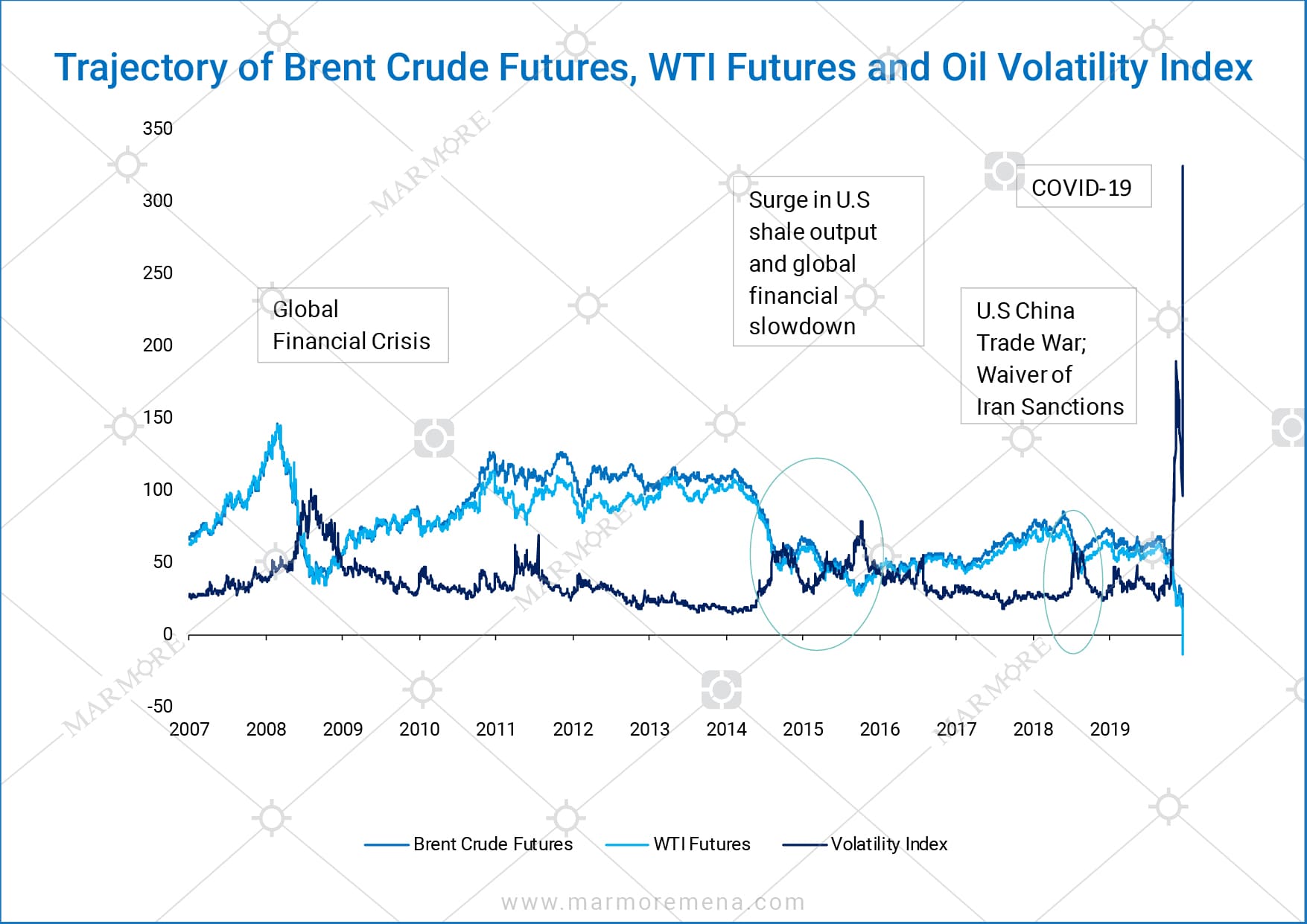

Remember April 2020? Prices went negative. Literally -$37 a barrel. That happened because the world ran out of places to put the oil in Cushing, and traders were basically paying people to take the contracts off their hands so they wouldn't have to show up in Oklahoma with 1,000 barrels they couldn't store. It was a localized storage crisis disguised as a global market collapse.

How the Futures Curve Actually Works (No, It’s Not Linear)

Most people assume if oil is $70 today, the futures contract for six months from now should also be $70, or maybe a little higher. Wrong.

🔗 Read more: ONEOK Stock Price Today: Why This Energy Giant Is Finally Turning a Corner

The market lives in two states: Contango and Backwardation.

In Contango, the future price is higher than the current (spot) price. This is normal-ish. It reflects the cost of "carry"—insurance, storage, and interest. If you buy oil now to sell later, you have to pay to keep it somewhere. But if the Contango gets too wide, savvy players buy physical oil, shove it in a tank, sell a future against it, and lock in a guaranteed profit. This is called a cash-and-carry trade.

Backwardation is the opposite. It’s when the price for immediate delivery is higher than the price for the future. This happens when there’s a shortage right now. Maybe a pipeline in Libya blew up, or there’s a hurricane in the Gulf of Mexico. Refiners are desperate for oil today, so they pay a premium. In this scenario, the market is basically telling you: "Don't store it. Sell it now."

The Invisible Hands: Speculators vs. Hedgers

There’s this common myth that "speculators" are the villains driving up gas prices. It's a bit more nuanced than that.

The market for futures WTI crude oil needs speculators. Without them, the market would be "illiquid," meaning you couldn't buy or sell quickly without moving the price too much.

- The Hedgers: These are the "real" players. Think ExxonMobil or Delta Air Lines. Delta needs to know what they’ll pay for jet fuel in six months so they can price their tickets. They buy futures to lock in costs. If oil goes to $150, they don't care; they’ve already locked in $80.

- The Speculators: These are the folks looking for a profit. They provide the "other side" of the trade for the hedgers.

If a driller wants to sell their future production to protect against a price drop, they need someone to buy it. If every other driller is also trying to sell, who buys? The speculator. They take the risk the driller doesn't want.

Why the US Dollar is Oil's Best Friend (and Worst Enemy)

Oil is priced in U.S. Dollars globally. This is a massive deal.

If the Dollar gets stronger, oil usually gets cheaper for Americans but more expensive for everyone else. If you're a refiner in Japan buying oil in Yen, and the Dollar goes up 10%, your oil just got 10% more expensive even if the "price" on the screen didn't move. This creates a natural "inverse correlation." When the DXY (Dollar Index) spikes, WTI usually feels the gravity.

But don't treat this as a perfect rule. In 2022, we saw both the Dollar and oil rocket upward at the same time because of the war in Ukraine. Geopolitics almost always trumps currency trends.

Reading the "Tealeaves" of the COT Report

If you want to know what’s actually happening in futures WTI crude oil, you have to look at the Commitments of Traders (COT) report. The CFTC releases this every Friday.

It breaks down who owns what. Are the "Managed Money" (hedge funds) heavily long? If they are all piled into one side of the trade, the market is "overcrowded." When everyone is already long, there’s no one left to buy. That’s usually when a sharp correction happens.

Expert traders look for "divergence." If prices are hitting new highs but the "Commercials" (the people who actually handle the oil) are selling aggressively, something is wrong. The smart money is usually the physical players, not the guys in suits in Greenwich, Connecticut.

Environmental Shifts and the "Peak Demand" Myth

For years, people talked about "Peak Oil"—the idea that we’d run out of the stuff. Now, the conversation has shifted to "Peak Demand."

The logic is that electric vehicles (EVs) and renewables will kill the need for WTI. Kinda makes sense on paper. But in reality, crude oil is used for way more than just cars. Petrochemicals, plastics, asphalt, and shipping grade fuel keep the floor under the price.

Investors have pulled back from funding new oil projects because of ESG (Environmental, Social, and Governance) pressures. This has created a weird situation where supply might actually drop faster than demand. If you stop drilling for new oil but people are still flying planes and buying plastic toys, the price of futures WTI crude oil could stay higher for longer than the "green transition" narrative suggests.

Geopolitical Risk: The "Fear Premium"

The Middle East, Russia, and even Venezuela. These places dictate the "fear premium."

👉 See also: Thrift Savings Plan 401k: Why You’re Probably Leaving Free Money on the Table

When things are calm, WTI trades based on fundamentals—how much is in the tanks at Cushing. But when a tanker gets seized in the Strait of Hormuz, the market adds a $5 or $10 premium instantly. This isn't because supply has actually stopped; it’s because of the risk that it might.

WTI is slightly more insulated from this than Brent (the North Sea benchmark used in Europe) because the U.S. is now a massive producer. We don't rely on the Middle East like we used to. However, because oil is a fungible global commodity, a shock anywhere is a shock everywhere. If Brent goes up, WTI follows it like a shadow.

Practical Steps for Tracking the Market

Don't just watch the headlines. Headlines are lagging indicators. By the time you read "Oil surges on supply fears," the move is probably over.

Instead, track the crack spread. This is the difference between the price of crude oil and the products made from it (gasoline and heating oil). If the crack spread is high, refiners are making a ton of money. They will buy more crude to take advantage of those margins, which pushes WTI prices up. If the crack spread collapses, refiners slow down, and crude prices usually follow them down into the basement.

Keep an eye on the weekly EIA (Energy Information Administration) inventory reports. They come out every Wednesday. These are the "truth" of the market. They tell you exactly how many barrels were added to or taken out of storage. A "draw" (decrease) is bullish. A "build" (increase) is bearish.

Actionable Insights for the Informed Observer

If you're looking to actually engage with or understand this market, stop thinking about it as a single number.

🔗 Read more: Eicher Motors Ltd Stock Price: Why Most People Are Getting It Wrong

- Watch the Spreads: Look at the difference between the current month and the next month. This "calendar spread" tells you more about the health of the market than the flat price does.

- Monitor the Dollar: If you see the U.S. Dollar starting a major bull run, be very cautious about being "long" oil.

- Check Cushing Levels: If storage at Cushing drops below 20 million barrels, things get "tight," and price spikes become much more violent.

- Differentiate between WTI and Brent: WTI is your U.S. economic barometer; Brent is your geopolitical barometer. They usually trade within a few dollars of each other, but if that "spread" widens to $10 or $15, there is a major structural problem in global shipping or refining.

The market for futures WTI crude oil is a beast. It’s a mix of math, geology, politics, and human greed. It doesn't care about your "opinion" on the economy. It only cares about how much oil is sitting in a pipe in Oklahoma and how much it costs to keep it there.

Focus on the physical reality. That's where the real money is made. Ignore the noise of the 24-hour news cycle and look at the inventories. The tanks don't lie.

Key Takeaways for Navigating WTI Markets

- Analyze the "Term Structure": Check if the market is in Contango or Backwardation to understand if there is a current surplus or shortage.

- Follow the Crack Spread: The profitability of refiners is the primary driver of crude oil demand.

- Use the COT Report: Identify when speculative positions are "overextended" to predict potential reversals.

- Watch Cushing Inventory: Treat the storage levels at the Oklahoma hub as the primary indicator of North American supply-demand balance.

- Currency Correlation: Always overlay a chart of the U.S. Dollar Index (DXY) when making long-term price predictions for crude.

By focusing on these structural elements rather than reactive news, you gain a clearer picture of the energy landscape and the forces driving the world's most vital commodity.