You’re sitting there, staring at your bank account, wondering if that "extra" money is actually coming. We’ve all done it. You start mental-mathing your way through the last twelve months of paychecks, trying to figure out if Uncle Sam owes you a trip to Mexico or if you’re about to owe him the cost of a used Honda Civic. This is exactly where a free income tax estimator enters the chat.

Tax season is honestly a psychological rollercoaster. One minute you’re feeling rich because of a bonus, and the next, you’re sweating because you forgot to adjust your withholdings after getting married or starting that side hustle on Etsy. Most people treat tax forecasting like a game of blackjack. They hope for the best but have no idea what’s actually in the deck.

But here’s the thing.

A tax estimator isn't a crystal ball. It’s a calculator. And like any calculator, if you feed it garbage data, it’s going to spit out a garbage result. If you’re using one of these tools and just "winging" the numbers, you are setting yourself up for a very rude awakening come April.

The Math Behind the Curtain

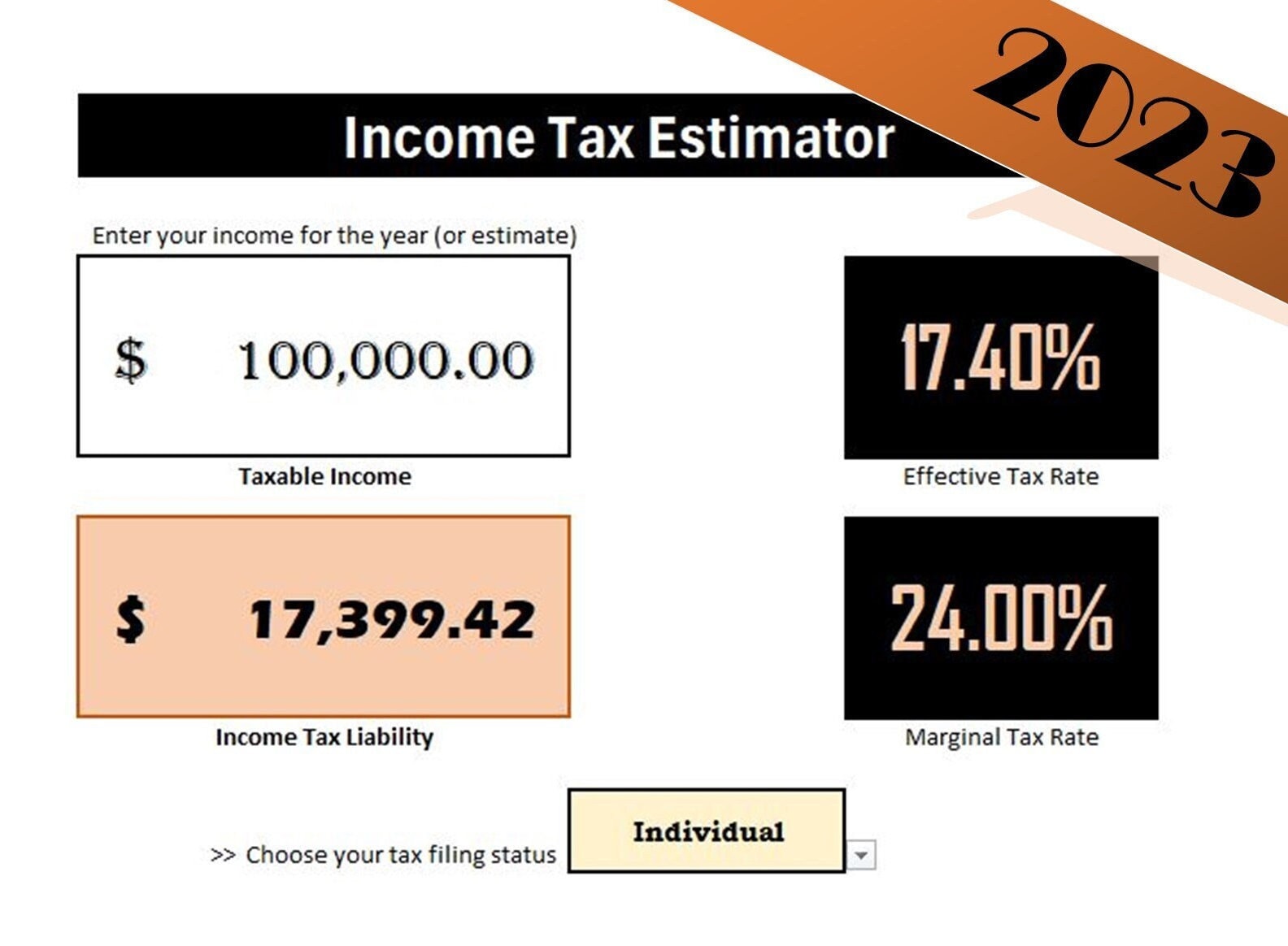

Most people think taxes are a flat percentage. It’s not that simple. The U.S. uses a progressive tax system, which basically means your income is chopped up into buckets. The first bucket is taxed at 10%, the next at 12%, and so on. When you use a free income tax estimator, the software is essentially trying to map your estimated annual earnings across these brackets while accounting for the Standard Deduction—which, for the 2025 tax year (filing in 2026), has adjusted again for inflation.

📖 Related: Fresh Mozzarella Cheese Costco: Why This $10 Kirkland Tub Is Actually a Big Deal

For single filers, that standard deduction is now $15,000. For married couples filing jointly, it’s $30,000.

If you make $60,000, you aren't taxed on $60,000. You’re taxed on $45,000 (if you’re single). That’s a massive distinction that many "quick" calculators accidentally gloss over if you don't input your filing status correctly.

Why Your "Quick Check" Is Usually A Lie

I’ve seen people pull up a free income tax estimator on their phone, type in two numbers, and then start shopping for a new TV. Stop. Just stop.

The biggest mistake is ignoring the "above-the-line" adjustments. Are you contributing to a 401(k)? That lowers your taxable income. Did you pay student loan interest? That changes the math. What about health savings accounts (HSAs)? If you aren't accounting for these, your estimate is basically a work of fiction.

Let’s talk about the "Side Hustle Trap." In 2026, the IRS is more vigilant than ever about 1099-K forms. If you made over $600 selling vintage clothes or driving for a ride-share app, that platform is sending a form to the IRS. If you use a tax estimator but forget to include that $4,000 you made on the side, your "refund" might actually turn into a "payment due" notice.

Self-employment tax is a whole different beast. It’s 15.3%. That’s on top of your regular income tax. Most basic estimators won't automatically calculate that unless you specifically tell it you have self-employment income.

Real Tools vs. Ad-Heavy Junk

Not all estimators are created equal. Honestly, some of them are just lead-generation funnels designed to get your email address so they can spam you with loan offers. You want tools that actually mirror the IRS worksheets.

- The IRS Tax Withholding Estimator: It’s clunky. It looks like it was designed in 2005. But it is the most accurate tool available because it comes directly from the source. It asks for your most recent paystub details and actually factors in the federal tax already withheld.

- TurboTax & H&R Block Calculators: These are much prettier. They have better user interfaces and are great for "what-if" scenarios. "What if I contribute $2,000 more to my IRA?" These tools excel at showing that immediate impact.

- SmartAsset: This one is great for a high-level view of how state taxes affect your take-home pay. Since state tax laws vary wildly—from Florida’s 0% to California’s high brackets—this is crucial for anyone who moved during the year.

The Secret Language of Tax Credits

There is a huge difference between a "deduction" and a "credit." A deduction lowers the amount of income you’re taxed on. A credit is a dollar-for-dollar reduction of the tax you actually owe.

The Child Tax Credit (CTC) is a classic example. If a free income tax estimator tells you that you owe $3,000 in taxes, but you qualify for a $2,000 CTC, your bill drops to $1,000. Some of these credits are "refundable," meaning if the credit is bigger than the tax you owe, the government actually sends you the difference.

🔗 Read more: Modern Japanese House Design: Why It Is Actually Hard to Live In

If you’re a student or paying for daycare, you need to make sure the estimator you're using asks about the American Opportunity Tax Credit (AOTC) or the Child and Dependent Care Credit. If it doesn't, you’re leaving money on the table in your projection.

Capital Gains: The Great Estimator Killer

Did you sell some crypto this year? Maybe you offloaded some Nvidia stock after it spiked?

This is where the free income tax estimator usually breaks. Short-term capital gains (assets held for less than a year) are taxed at your ordinary income rate. Long-term gains (held for over a year) are taxed at 0%, 15%, or 20% depending on your total income.

If you just lump your stock gains in with your salary, you might be overestimating your tax bill. Conversely, if you forget to include them, you’re in for a shock. And don't get me started on "Wash Sales." If you sold a stock at a loss but bought it back within 30 days, you can't claim that loss to offset your gains. Most simple calculators can't handle that level of nuance.

When Should You Use One?

Timing is everything.

Using an estimator in April is pointless. By then, the damage is done. The best time to use a free income tax estimator is actually in September or October.

Why? Because you still have time to pivot.

If the estimator shows you’re going to owe $2,000, you can increase your withholdings at work for the last few months of the year. Or you can dump more money into your 401(k) to lower your taxable income. You have agency. Once December 31st passes, most of your "levers" are locked in place.

The Nuance of "Filing Status"

It sounds boring, but your filing status is the foundation of the whole house. "Head of Household" is a status many people overlook. If you’re unmarried but pay more than half the cost of keeping up a home for a qualifying person, you get a much larger standard deduction than a "Single" filer.

I once talked to a guy who used a free income tax estimator and thought he was getting a $4,000 refund. He’d selected "Married Filing Jointly" even though he was technically separated and his spouse was filing a separate return. He ended up owing money. Small dropdown menus have big consequences.

Actionable Steps for a Better Estimate

Don't just guess. If you want a number that actually reflects reality, you need to do a little bit of homework.

- Grab your last three paystubs. Look at the "Year to Date" (YTD) federal tax withheld. This is the most important number.

- Estimate your "Above-the-Line" deductions. Total up your student loan interest (up to $2,500) and any HSA contributions you made outside of your employer.

- Account for interest and dividends. Look at your 1099-INT forms from last year as a baseline. Banks are finally paying interest again, and that $500 you made in a high-yield savings account is taxable income.

- Run the numbers through at least two different tools. If the IRS estimator and the NerdWallet one give you wildly different results, look at the "Taxable Income" line on both. Find out where the discrepancy is.

Beyond the Calculator

At the end of the day, a free income tax estimator is just a tool for awareness. It helps you avoid "Tax Surprise Syndrome."

If your life is simple—one W-2, no kids, no house, no investments—the estimator will be nearly perfect. But most lives aren't simple. We have side gigs, we get married, we buy homes, we invest in weird things.

Real tax planning involves looking at these numbers and realizing that "refunds" aren't actually gifts from the government. A refund is just an interest-free loan you gave to the IRS. If your estimator shows a $5,000 refund, you might want to adjust your W-4 so you get more of that money in your weekly paycheck instead of waiting until next year.

👉 See also: Mid Top Skateboard Shoes: Why Most Skaters Are Actually Missing Out

Stop treating your taxes like a mystery that only gets solved in April. Take fifteen minutes, get your documents together, and run a proper estimate. You'll sleep better knowing whether you're getting a check or writing one.

Next Steps to Secure Your Finances

To get the most out of your tax planning, your next move should be to gather your most recent paystubs and visit the official IRS Tax Withholding Estimator. Use the "Adjust Results" feature to see how increasing your retirement contributions today could lower your tax liability for the entire year. Once you have a baseline, cross-reference that result with a secondary calculator like SmartAsset to ensure your state-level tax obligations are also being met, especially if you live in a state with local or city-specific income taxes.