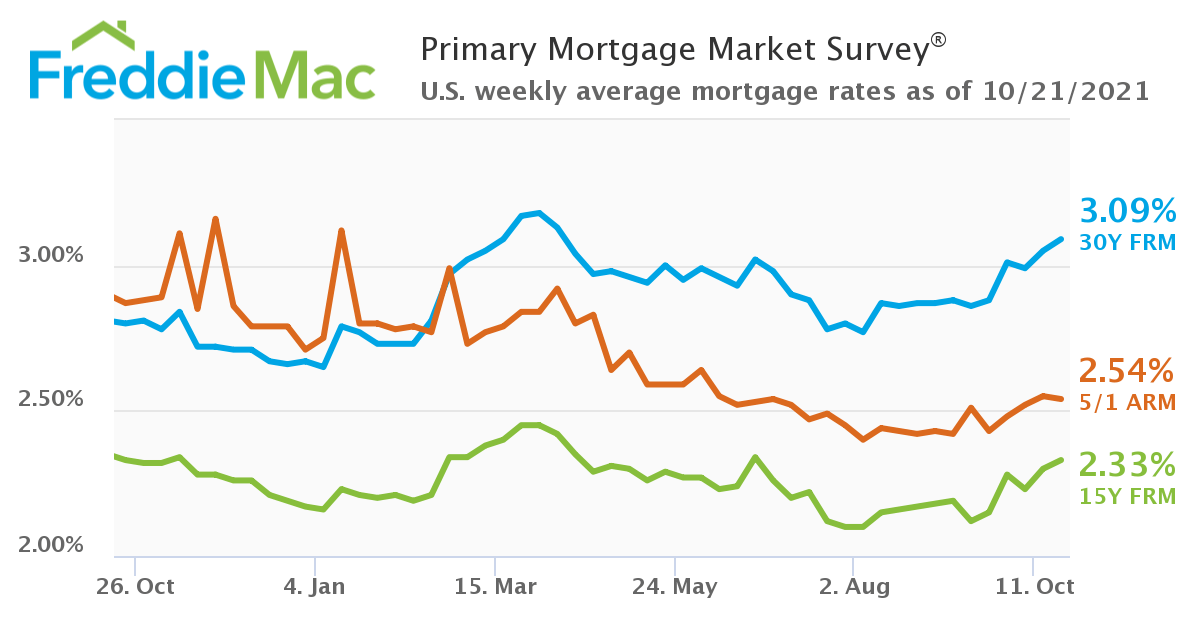

Honestly, walking into a bank today feels a lot different than it did even six months ago. If you’ve been glued to the news, you probably saw the latest headlines about Freddie Mac mortgage rates hitting their lowest levels in over three years. As of January 15, 2026, the 30-year fixed-rate mortgage averaged 6.06%.

That’s a big deal.

It’s down from 6.16% just a week ago and looks like a total bargain compared to the 7.04% we were seeing this time last year. But there is a lot of noise out there. People are calling it a "plunge," while others are still waiting for that mythical 3% to return. Spoiler: it’s not coming back anytime soon.

The market is reacting to some pretty massive moves. Just recently, the federal government announced a $200 billion mortgage-backed securities (MBS) buyback plan. Basically, the goal is to force affordability back into a market that has been frozen solid for years. When the government starts buying bonds like that, it pushes prices up and yields down.

And mortgage rates usually follow those yields like a shadow.

The Reality Behind the Freddie Mac Mortgage Rates Survey

When Sam Khater, Freddie Mac’s Chief Economist, talks about "improving momentum," he isn't just blowing smoke. We are actually seeing it in the data. Purchase applications are jumping. Refinance activity is finally waking up from a long nap.

📖 Related: Understanding Mass State Tax: Why Your Paycheck Looks the Way It Does

But you have to understand what the Freddie Mac Primary Mortgage Market Survey (PMMS) actually represents. It’s a barometer. It’s an average of what lenders are offering to "prime" borrowers—people with 20% down and credit scores that would make a banker weep with joy.

If your credit is a bit messy or you're only putting 3.5% down on an FHA loan, your personal rate might not look exactly like that 6.06% headline.

Why 6% is the magic number right now

Psychology plays a huge role in real estate. For the last couple of years, the "lock-in effect" has been the industry's biggest nightmare. About 68% of people with a mortgage right now have a rate under 5%. If you're sitting on a 3% rate, why would you move and take on a 7.5% rate? You wouldn't. You'd stay put.

But at 6%? The math starts to change.

The gap between a 4.5% "old" rate and a 6% "new" rate is a lot easier to stomach than the gap we saw in 2024. It's roughly a $350 difference on a $400,000 home. That is still a chunk of change, but for a family that needs an extra bedroom or a shorter commute, it's finally a manageable trade-off.

Breaking Down the 2026 Rate Landscape

The downward trend isn't just hitting the 30-year loans. The 15-year fixed-rate mortgage is currently sitting at 5.38%.

A year ago, that was way up at 6.27%. This specific drop is fueling a surge in "tactical" refinances. These are homeowners who bought in late 2023 or early 2024 when rates were flirting with 8%. For them, dropping to 5.3% or even 6% is a massive win that saves hundreds of dollars every single month.

✨ Don't miss: Price of Weight Watchers Stock: What Most People Get Wrong

- 30-Year Fixed: 6.06% (Current) vs. 7.04% (Last Year)

- 15-Year Fixed: 5.38% (Current) vs. 6.27% (Last Year)

- Spread Compression: The gap between the 10-year Treasury and mortgage rates is finally narrowing, sitting around 1.89 percentage points.

What’s interesting is that while Freddie Mac shows 6.06%, some daily trackers like Mortgage News Daily actually dipped briefly to 5.99% in early January. It was the first time we saw a "5" at the front of that number in years. Even if it was just for a moment, it changed the vibe of the whole spring home-buying season.

The "Trump Buyback" and Market Volatility

We can't talk about these rates without mentioning the $200 billion MBS buyback. The administration is essentially trying to "grease the wheels" of the housing market ahead of the midterms. It’s a bold move, and it has definitely worked in the short term to pull rates down.

However, there’s a catch.

Expanding Treasury yields and solid economic growth can actually put upward pressure on rates. It’s a tug-of-war. The government is pulling one way to lower costs, but a strong economy naturally pushes rates higher because it signals that the Fed doesn't need to be in a rush to cut.

What Most People Get Wrong About Freddie Mac Data

People tend to treat the weekly survey like it’s a quote they can take to the bank. It's not. It’s a trailing indicator. By the time the survey is released on Thursday morning, the market may have already moved.

Also, the survey doesn't account for "points." If a lender offers you 5.75% but charges you $6,000 in upfront fees to get it, is that really a better deal than 6.06% with no fees? Probably not. You have to look at the APR, not just the flashy headline number.

The impact of "historically soft" inventory

Even with Freddie Mac mortgage rates moving in the right direction, we have a supply problem. We are still short about 3.7 million housing units in the U.S. Lower rates make it cheaper to buy, but they also mean more competition. If rates drop to 5.5% by the summer, don't be surprised if you see bidding wars coming back with a vengeance.

Lowering the cost of borrowing is great, but if it just drives home prices up by 10% because everyone is suddenly out shopping again, the "affordability" gain is basically a wash. It's a frustrating cycle.

Actionable Steps for Borrowers in 2026

If you're looking at these numbers and wondering if you should jump in or wait, here is the honest truth: you can't time the bottom. Nobody can. But you can be prepared.

Check your "Rate Gap"

If you currently have a mortgage at 7.5% or higher, the current average of 6.06% is likely enough to justify a refinance. Generally, if you can drop your rate by 0.75% to 1%, and you plan to stay in the house for at least three more years, the math usually works out in your favor.

Don't ignore the 15-year option

If you’re looking to refinance and can handle a higher monthly payment, that 5.38% rate is incredibly attractive. You’ll save a fortune in interest over the life of the loan.

Get a "Live" Quote

The Freddie Mac survey is a great "weather report," but you need a specific quote for your "house." Call a couple of lenders. See what they are actually offering today, not what they were offering last Tuesday when the survey data was being collected.

Watch the 10-Year Treasury

If you want to know where rates are going tomorrow, watch the 10-year Treasury yield today. If it’s climbing, mortgage rates will likely follow. If it’s sliding, you might want to hold off on locking your rate for 24 hours to see if you can snag a better deal.

🔗 Read more: Free guest list template: Why simple tools beat expensive event software every time

Think about the "Lock-In" release

If you are a buyer, keep an eye on new listings. As rates stay near 6%, more homeowners who were "locked in" will finally decide to sell. This could mean more inventory for you to choose from, even if the competition is a bit stiffer.

The reality of the 2026 market is that we are finally moving away from the "crisis" rates of the post-pandemic era. We aren't back to the ultra-cheap money of 2021, but we are entering a period of "normalcy" that we haven't seen in a long time. 6% isn't perfect, but compared to where we've been, it's a massive breath of fresh air for the American homeowner.