Tax season is usually a blur of W-2s and 1099s. Then, out of nowhere, you check your mail and find a piece of paper labeled Form 1095-C. Most people just toss it on the "deal with this later" pile. Don't do that. Honestly, while it looks like just another boring IRS document, it’s actually the proof you need to show the government that you had health insurance through your job.

If you've ever wondered form 1095-C what is it and why it suddenly appeared in your life, you aren't alone. It exists because of the Affordable Care Act (ACA). Basically, the IRS wants to make sure large employers are actually offering the insurance they're legally required to provide. It also tracks whether you, the employee, took that insurance or decided to go another route.

👉 See also: Photography Business Name Suggestions: Why Most Photographers Pick the Wrong One

The Nitty-Gritty of What This Form Actually Does

Technically, the form is called the "Employer-Provided Health Insurance Offer and Coverage" statement. It’s sent out by "Applicable Large Employers," or ALEs. In plain English? If you work for a company with 50 or more full-time employees, they are likely required to send you one of these every year. It’s a record-keeping tool.

The IRS uses the data on this form to coordinate a few different things. First, they check if your employer is following the "employer mandate"—the rule that says big companies have to offer affordable insurance. Second, they use it to see if you’re eligible for premium tax credits. If your job offered you "affordable" coverage (according to the IRS's specific math) and you turned it down to buy a plan on the Health Insurance Marketplace, you might not be eligible for those subsidies. The 1095-C is the "snitch" that tells the IRS which side of that fence you fall on.

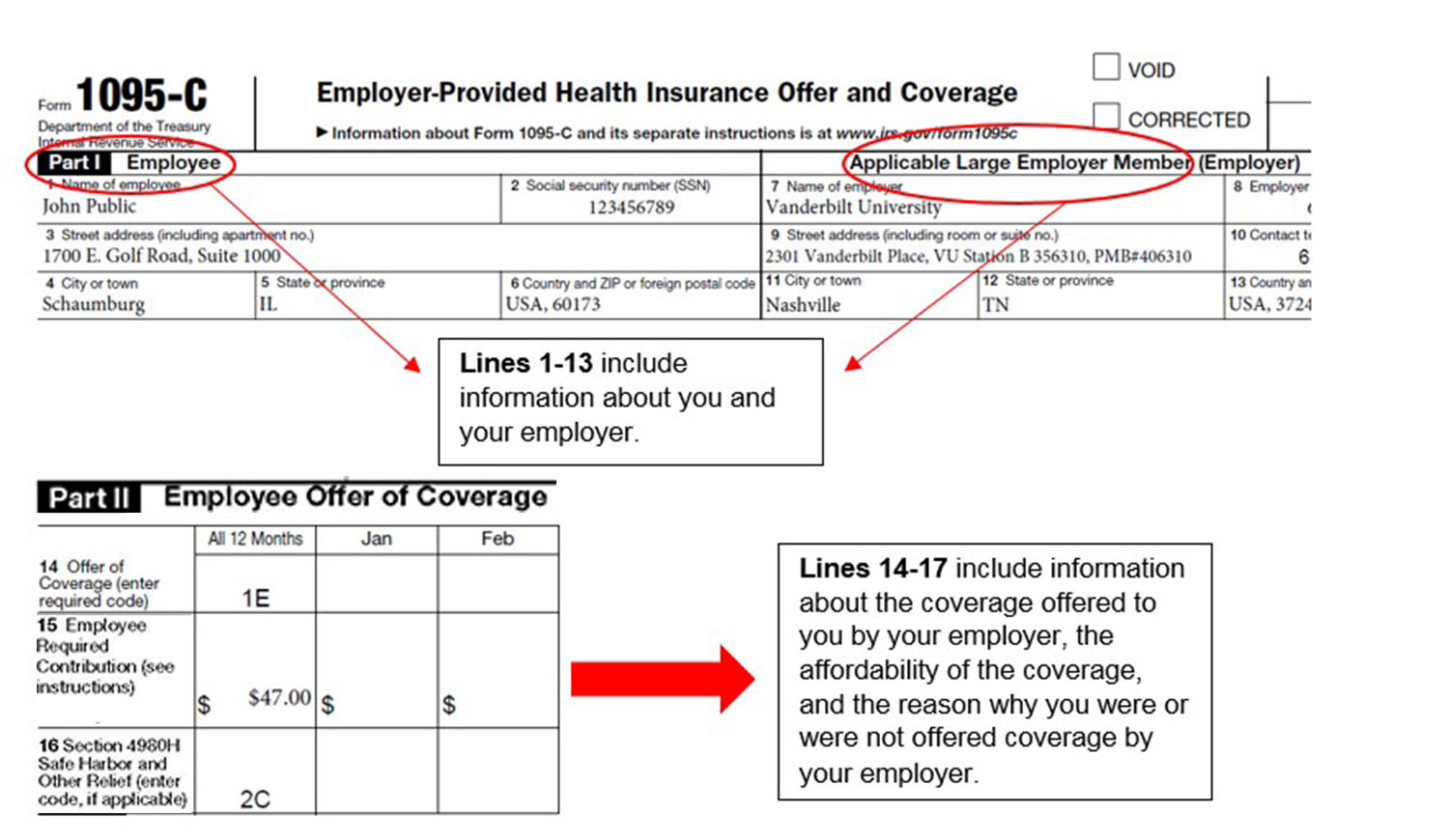

It’s a three-part document. Part I is just the basics—your name, address, and your employer's info. Part II is where things get weird. This section uses a series of cryptic codes (like 1A, 1E, or 2G) to describe exactly what kind of coverage you were offered, how much the cheapest plan cost you, and why the employer thinks they aren't liable for a penalty. Part III is only filled out if your employer "self-insures," meaning they pay the medical claims themselves rather than paying an insurance company like Blue Cross or Aetna to do it.

Do You Actually Need It to File Your Taxes?

Here is the part that confuses everyone: You usually don’t need to wait for your 1095-C to file your tax return.

Unlike a W-2, which you absolutely must have to input your income, the information on a 1095-C is mostly for your records. Most tax software will ask you a simple "Yes/No" question about whether you had health insurance for the year. You can answer that based on your own knowledge. You don't have to attach the 1095-C to your return.

However—and this is a big "however"—if you received a premium tax credit because you bought insurance through the Marketplace (Healthcare.gov), you'll need the info from your 1095-A, which is a totally different form. The 1095-C just serves as the backup proof in case the IRS ever audits you and asks, "Hey, did your job offer you better insurance than what you got on the exchange?"

If you see an error on the form, like the wrong months checked off or a misspelled name, get it fixed. Call your HR department. While it might not stop your filing today, a mismatch in IRS records can trigger a "Letter 12C" or other automated inquiries months down the road. Nobody wants that.

👉 See also: Why the Social Security Area Number Map Doesn't Actually Work the Way You Think

Deciphering the Codes: A Quick Translation

If you look at Part II, Line 14 and Line 16, you'll see those alphanumeric codes mentioned earlier. They look like gibberish.

Code 1A is the gold standard. It means your employer offered "Qualifying Health Coverage" that met the federal poverty line safe harbor. If you see 1H, it means no offer of coverage was made—maybe you weren't full-time yet, or you were in a waiting period.

The dollar amount on Line 15 is often the most misunderstood part of the whole thing. It isn't what you actually paid for insurance. It is the cost of the lowest-cost monthly premium for self-only coverage that your employer offered you. Even if you chose the "Platinum Family Plan" that costs you $800 a month, Line 15 might only show $105. That’s because the IRS only cares about the cheapest "minimum value" option available to you. They use this to determine "affordability." For 2024 and 2025, the affordability threshold has hovered around 8.39% to 9.02% of your household income.

Common Misconceptions and Why They Matter

A lot of people think the 1095-C is a bill. It isn't. You don't owe money when you get this.

Another common myth is that if you didn't get one, your company is breaking the law. Not necessarily. If you worked for a small business with 30 employees, they aren't required to send this. You might get a 1095-B instead, or nothing at all. Also, if you were a part-time worker or an independent contractor, you won't get a 1095-C because you aren't considered a "full-time equivalent" under the ACA guidelines.

Real World Example: The "New Hire" Gap

Imagine you started a job in September. Your insurance didn't kick in until October 1st. When you get your 1095-C, you’ll see "No Offer" codes for January through September. This is totally normal. If you had insurance through a previous job or a COBRA plan during those months, those providers would be responsible for their own reporting. The 1095-C is a snapshot of your relationship with that specific employer only.

Actionable Steps for Tax Season

If you just received this form, don't panic. Here is what you should actually do with it:

- Verify your Social Security Number. If the SSN on the form is wrong, the IRS won't be able to match the coverage to your tax account. This is the #1 reason for "please explain your insurance" letters from the IRS.

- Check the months covered. Ensure the "All 12 Months" box (or the individual month boxes) accurately reflects when you were eligible for benefits.

- Keep it with your tax records for three years. This is the standard window for IRS audits. Scan it, save it as a PDF, or stick it in the folder with your W-2s.

- File your taxes anyway. If you know you had insurance, you don't need to wait for this form to arrive in the mail to hit "submit" on your tax software. Most employers have until early March to mail these out, which is well after many people file.

- Consult Form 8962 if needed. If you did take a tax credit for Marketplace insurance, use the 1095-C to confirm you weren't actually eligible for "affordable" employer coverage during those months. If you were, you might have to pay back some of that tax credit.

Understanding form 1095-C what is it basically boils down to having a receipt for your health insurance. It’s the paper trail that keeps you—and your employer—in the clear with the IRS regarding the complex rules of the Affordable Care Act. Keep it safe, check the numbers, and move on with your life.