You’d think in a country that basically runs on credit cards and complicated tax codes, we’d be better at this. But we aren't. Most people look at their 401(k) statements like they’re trying to decipher ancient Sanskrit. Honestly, financial illiteracy in America isn't just a "personal problem" or a lack of willpower; it’s a systemic quiet crisis that’s costing the average household thousands of dollars every single year.

It’s expensive to be confused.

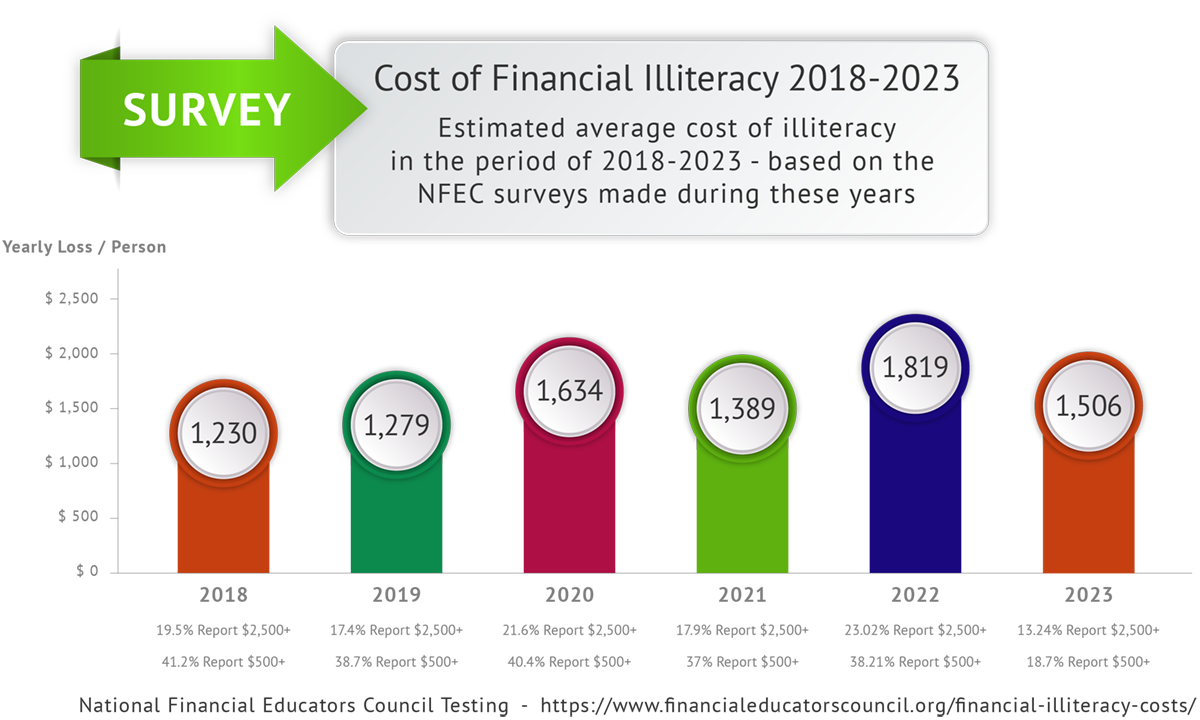

Think about the last time you sat down to really look at your debt. Not just the "total balance" on the app, but the actual math. If you don’t understand how compounding interest works against you on a 24% APR credit card, you aren't just "bad with money." You’re being drained. The TIAA Institute and the Global Financial Literacy Excellence Center (GFLEC) at George Washington University have been tracking this for years through their P-Fin Index. Their data is pretty grim. Only about half of U.S. adults can correctly answer basic questions about risk, inflation, and interest.

It gets worse.

We live in a world where you can buy a fractional share of an AI company with a thumbprint but don’t know how a Roth IRA differs from a Traditional one. That gap—between high-tech access and low-level understanding—is where the real danger lives.

The Brutal Reality of Financial Illiteracy in America

We have to stop pretending this is just about "budgeting." It's deeper. The 2023 P-Fin Index showed that financial literacy has actually remained stagnant or even dipped in some demographics over the last seven years.

Why? Because the system got more complex while our brains stayed the same.

Take the "Big Three" questions developed by economists Annamaria Lusardi and Olivia Mitchell. They test your grasp of interest rates, inflation, and risk diversification. If you can’t answer those, you’re statistically more likely to carry high-cost debt and less likely to have an emergency fund. It’s not just a "poor person" problem, either. High-income earners often suffer from financial illiteracy in America because they outsource their thinking to advisors they don't know how to vet. They pay 1.5% in assets under management (AUM) fees without realizing that over 30 years, that single percentage point could eat a third of their total nest egg.

That’s a house. They are literally paying a house in fees because they didn't do the math.

The Inflation Trap

Most people understand that prices go up. They see the eggs costing $5 and get it. But they don't understand the "purchasing power" side of the equation. If your "high-yield" savings account is giving you 4% but inflation is sitting at 5%, you are losing money. You’re becoming poorer while your balance goes up. It’s a psychological trick that keeps people stuck in "safe" investments that actually erode their wealth over decades.

Why Our Schools Are Failing the Money Test

You probably spent three months learning about the mitochondria being the powerhouse of the cell. Cool. But did anyone explain how a credit score is calculated? Probably not.

Only about 25 states currently require a personal finance course for high school graduation. That’s better than it was ten years ago, sure, but it’s still half the country. We are tossing 18-year-olds into the world with $50,000 in student loan debt before they even understand the difference between a subsidized and unsubsidized loan. It’s predatory.

The "Experience" Fallacy

There’s this weird idea that we learn about money by "doing." But money isn't like riding a bike. If you fall off a bike, you get a scraped knee. If you mess up your credit in your 20s, you might not be able to buy a home until your 40s. The stakes are too high for "trial and error."

I’ve talked to people who thought they were "investing" by putting money into a savings account. They didn't realize that the bank was taking their money, lending it out at 12%, and giving them back a measly 0.5%. They were the product, not the customer. This lack of fundamental knowledge creates a massive wealth gap. It’s not just about what you earn; it’s about what you keep and how that money works while you’re asleep.

The Psychological Toll of Not Knowing

Money is the leading cause of stress for American adults. It beats out work, health, and relationships. When you don't understand your finances, every bill feels like an attack. Every unexpected car repair feels like a catastrophe.

- Anxiety: The constant "checkbook math" running in the back of your head.

- Avoidance: Not opening the envelopes because you're scared of what’s inside.

- Relationship Strain: Arguments about spending that are actually about a lack of a shared plan.

When you're financially illiterate, you feel like a passenger in your own life. You’re waiting for the next paycheck, waiting for the tax refund, waiting for a miracle. Knowledge flips that. It turns you into the pilot. Even if the news is bad—like finding out you’re $80,000 in debt—knowing the exact number and the interest rate gives you a map.

The Industry That Profits From Your Confusion

Let’s be real: A lot of people make a lot of money because you’re confused.

💡 You might also like: What Is The US Dollar To The Canadian Dollar: What Most People Get Wrong

Payday lenders, "buy now, pay later" apps, and even some big-name banks rely on you not reading the fine print. They love financial illiteracy in America. If everyone understood the math behind "zero percent interest for 12 months" (and the deferred interest trap that triggers if you're one day late), these companies would lose billions.

Complexity is a feature, not a bug.

Look at the 401(k) options at a typical mid-sized company. You’re often presented with a "menu" of 30 different mutual funds with names like "Aggressive Growth Fund Class Z." Unless you know how to look for the "expense ratio," you’re just guessing. You might pick the one that did well last year, not realizing it has a 2% fee that will gut your returns over time.

The Crypto and "FinTok" Mirage

Then there's the new wave of misinformation. Social media is filled with "gurus" telling you to buy the latest memecoin or use "infinite banking" strategies. These are often just sophisticated ways to separate you from your cash. Without a solid foundation, it’s impossible to tell the difference between a legitimate investment and a Ponzi scheme wrapped in a TikTok filter.

How to Actually Fix Your Financial Literacy

You don't need an MBA. You really don't. You just need to master about five or six core concepts. Once you get those, the rest is just noise.

First, understand Opportunity Cost. Every dollar you spend on a $7 latte today isn't just $7. If that money were invested in a low-cost index fund for 30 years, it could be $50 or $60. Is the latte worth $60? Sometimes, yes. But you should make that choice consciously.

Second, learn the Rule of 72. It’s a simple way to see how long it takes for your money to double. Divide 72 by your expected annual rate of return. If you're getting 7% in the stock market, your money doubles every 10 years. If you’re paying 24% on a credit card, your debt doubles in three years. That should terrify you.

Move Away from "Manual" Finance

The smartest thing most people can do is automate their intelligence. If you have to "decide" to save every month, you’ll eventually fail. Willpower is a finite resource. Set up an automatic transfer to your brokerage account or your 401(k). Treat your savings like a bill you have to pay.

Actionable Steps to Bridge the Gap

If you feel like you’re behind, stop beating yourself up. Most of us weren't taught this. But you have to start moving.

Calculate Your True Net Worth

This isn't just for rich people. List every single asset (cash, car value, 401k) and every single debt (student loans, credit cards, mortgage). Subtract the debt from the assets. If the number is negative, that’s your starting line. You can’t win the game if you don't know the score.

Audit Your Fees

Log into your retirement account today. Look for the "Expense Ratio." If it’s over 0.50% for a basic fund, you’re likely being overcharged. Look for low-cost "Index Funds" or "Target Date Funds" that usually have fees closer to 0.05% or 0.10%. This 10-minute check can literally save you six figures over your lifetime.

The "High-Interest" Rule

Never, ever carry a balance on a card with an interest rate over 10% if you can help it. If you have high-interest debt, that is a financial emergency. Forget "saving" for a house or "investing" in the S&P 500 until that high-interest debt is gone. The 20% interest you're paying is a "guaranteed" loss that no investment can reliably beat.

Read One Classic Book

Don't follow "hustle culture" influencers. Read The Simple Path to Wealth by JL Collins or I Will Teach You To Be Rich by Ramit Sethi. These aren't about get-rich-quick schemes; they’re about understanding the plumbing of the financial system.

Question Everything "Free"

If a financial product is free—like a trading app or a "no-fee" checking account—find out how they make money. Usually, it’s by selling your data, "payment for order flow," or hitting you with massive fees when you make a mistake.

Financial illiteracy in America is a heavy burden, but it’s one you can put down. It starts with admitting you don't know what you don't know. Once you start asking the right questions, the math stops being scary and starts being a tool. You don't need to be a genius; you just need to be slightly more informed than the person the bank is trying to exploit. That’s enough to change your entire life.

To take the next step, look at your last three bank statements. Don't judge the spending, just categorize it. See exactly where the leaks are. Then, call one of your high-interest credit card companies and ask for a lower rate. You'd be surprised how often they say yes just because you asked. From there, pick one financial term you don't understand—like "Escrow" or "Tax-Loss Harvesting"—and spend five minutes reading about it. Small wins build momentum. Over time, those wins turn into a secure future.