Tax season never really ends for employers. If you've got people on the payroll, you're basically an unpaid tax collector for the IRS. It sounds harsh, but that’s the reality of the Employer’s Quarterly Federal Tax Return. You're responsible for reporting the income taxes, Social Security tax, and Medicare tax withheld from your employees' paychecks, along with your own share of those payroll taxes. Honestly, it’s one of those tasks that feels like it should be simpler than it actually is.

Most people dread filling out Form 941 because the math has to be perfect. One decimal point out of place and you're looking at a notice from the IRS that might take six months to resolve. It’s not just about the money; it’s about the documentation.

Why Does the IRS Care So Much About This Form?

The IRS uses Form 941 to bridge the gap between what you told them you’d pay and what you actually deposited. Think of it as a quarterly reconciliation. If you’re a small business owner, this is your pulse check. If your numbers don't match your Form W-2s at the end of the year, you’re in for a world of pain during an audit.

Generally, you have to file this every three months. Even if you didn't have any employees for a specific quarter, if you're a registered employer, you usually still have to file a "zero" return unless you’re a seasonal employer or you've filed a final return.

📖 Related: 200 West Street: What Most People Get Wrong About the Goldman Sachs Building NYC

The First Hurdle: Getting Your Basics Right

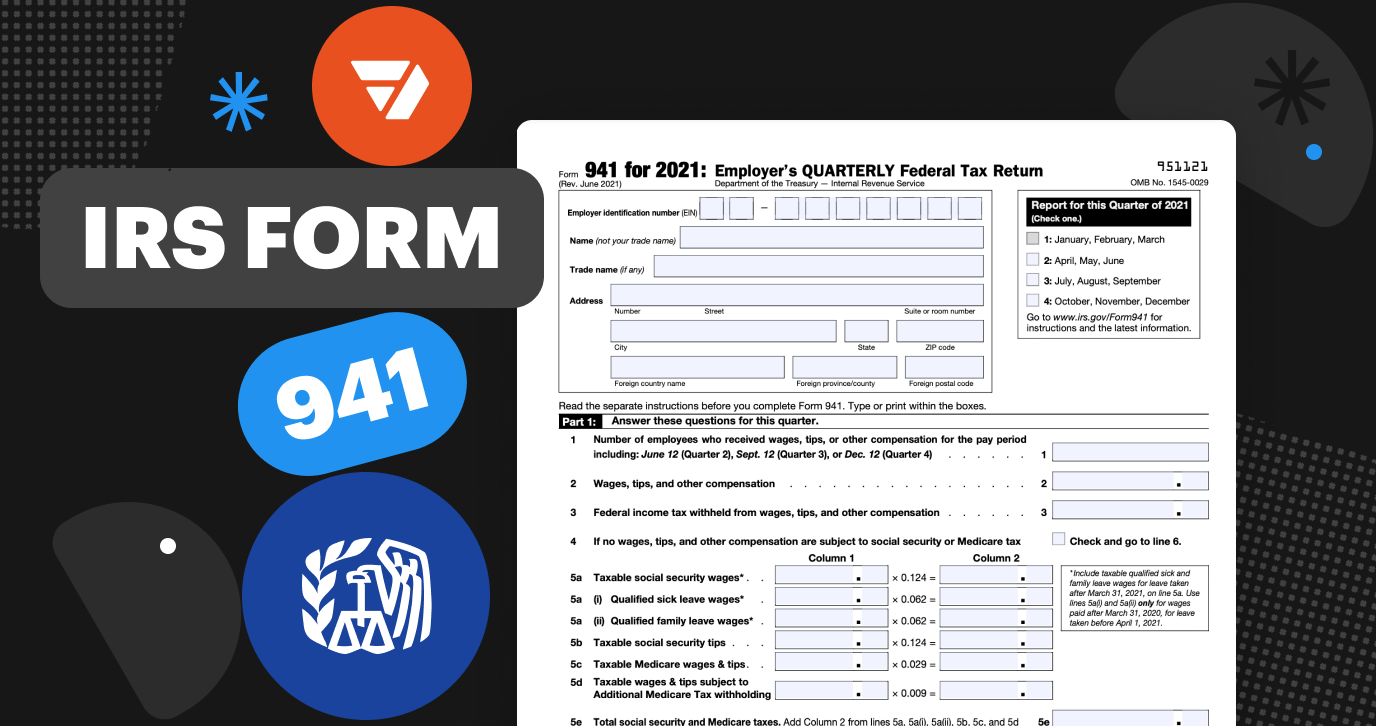

Before you even touch the lines, you need your Employer Identification Number (EIN). Don't use your Social Security number. If you don't have an EIN yet, you shouldn't be running payroll. You also need to make sure you’re using the correct form for the correct year. The IRS updates these forms more often than you’d think, often changing line numbers or adding "credit" sections that relate to temporary legislation like the defunct Employee Retention Credit (ERC).

Line 1: The Number of Employees

This is simpler than it looks. You count the number of employees who received pay during the pay period that includes March 12, June 12, September 12, or December 12. If you hired someone on the 15th and they didn't work the 12th, they don't count for this specific line. It’s a snapshot.

Line 2: Wages, Tips, and Other Compensation

Total it up. Every dime you paid in taxable wages goes here. This should match your internal payroll reports exactly. If you use software like Gusto or Quickbooks, they usually spit this number out for you, but it’s worth double-checking manually. Why? Because software glitches happen.

The Math Part: Social Security and Medicare

This is where things get "kinda" hairy. You’re dealing with different tax rates and wage bases.

For 2025 and 2026, the Social Security wage base typically climbs. You only tax the first $176,100 (or whatever the current inflation-adjusted cap is) of an employee's earnings. Once they hit that ceiling, you stop withholding the 6.2%.

- Line 5a: Taxable Social Security Wages. Multiply the total by 0.124. That’s 6.2% from the employee and 6.2% from you.

- Line 5c: Taxable Medicare Wages and Tips. There is no cap here. You multiply by 0.029.

- Line 5d: Additional Medicare Tax Withholding. If an employee earns more than $200,000, you have to withhold an extra 0.9%. Only the employee pays this, not you.

If you’re filling out Form 941 and your math on Line 5 doesn't match your actual withholdings, don't panic. Fractions of a cent matter. The IRS actually provides Line 7 for "Fractions of Cents" adjustments. It’s there because rounding differences between individual paychecks and the quarterly total are inevitable. Use it.

The Deposit Schedule Nightmare

Are you a monthly depositor or a semi-weekly depositor? This is the question that trips up everyone. Your status isn't something you choose; it’s determined by your total tax liability during a "lookback period."

If you reported $50,000 or less in taxes during the lookback period, you’re monthly. More than that? You’re semi-weekly.

If you’re a semi-weekly depositor, you must fill out Schedule B. This form breaks down your tax liability by the day. If you leave this out, the IRS will send the form back, or worse, hit you with a failure-to-deposit penalty even if you paid the money on time. They want to see when you became liable for the tax to ensure you deposited it within the required three business days.

💡 You might also like: Finding the Rite Aid Basin Rd: Why Local Pharmacy Access is Changing So Fast

Common Mistakes That Trigger Audits

Mistakes happen. But some mistakes look like fraud to a computer.

One big one is forgetting to report tips. If your employees receive more than $20 in tips a month, they have to report them to you. You have to report those on Line 5b. If you’re a restaurant owner and your Line 2 wages don't seem to align with the industry average for tips, that’s a red flag.

Another issue is the "Total Deposits" line. This is Line 13. You need to list the total amount you actually paid through EFTPS (Electronic Federal Tax Payment System). If you write down what you should have paid instead of what you did pay, you're going to get a bill for the balance plus interest.

Handling the Credits

While the pandemic-era credits are mostly phased out, there are still small business credits for things like paid family leave or certain R&D credits that can be applied against payroll taxes. If you’re claiming these, you usually need Form 8974. Filling out Form 941 while juggling these credits requires a high level of precision. Honestly, if you're at this stage, having a CPA look over it is the smartest $500 you'll ever spend.

Signing the Document

It sounds silly, but people forget to sign. Or they have the wrong person sign. Only an authorized person—like the president, vice president, or a fiduciary—can sign for a corporation. If you’re a sole proprietor, you sign it yourself.

If you use a third-party payer or a reporting agent, they can sign, but the legal responsibility for the taxes always sits with you, the business owner. If they mess up, the IRS is coming for your bank account, not theirs.

What to Do If You Miss the Deadline

The deadlines are firm: April 30, July 31, October 31, and January 31.

🔗 Read more: How Much is an Ounce of Gold Worth Today: Why the Market is Hitting Records

If you miss it, file anyway. The "Failure to File" penalty is 5% of the tax due for each month or part of a month the return is late, up to 25%. However, the "Failure to Pay" penalty is much smaller (0.5% per month). Basically, it’s always better to file a return you can’t pay than to not file at all.

Your Immediate Checklist for Success

Don't wait until the 30th of the month to start this.

- Verify your payroll records against your bank statements. Every single withdrawal for taxes should have a corresponding entry in your ledger.

- Log into EFTPS and download your payment history for the quarter. Don't guess. Look at the actual dates and amounts.

- Check for rounding errors. If your Line 6 (total taxes before adjustments) is $4,000.02 and your actual deposits were $4,000.00, put that negative $0.02 on Line 7.

- Review Schedule B. If you're a semi-weekly depositor, ensure the total on Schedule B matches Line 12 on Form 941 exactly. If they are off by one dollar, the IRS computer will flag it.

- Keep copies of everything. The IRS has three years to audit these forms, but in some cases, they can go back much further. Store digital copies and physical backups.

Filling out the paperwork is just the final step of a three-month process. If your bookkeeping is clean, the form is just a summary. If your bookkeeping is a mess, Form 941 will reveal every single crack in your system. Take it slow, use a calculator, and remember that the IRS prefers a corrected return (Form 941-X) over a fraudulent one. If you find a mistake later, fix it immediately.