You just closed a trade. Maybe it was that Nvidia run-up you timed perfectly, or perhaps you finally unloaded that crypto bag after a volatile week. You’re looking at a $5,000 profit. It feels great until you realize the IRS is basically sitting at your dinner table waiting for their cut. Honestly, most people focus way too much on the "gain" and not nearly enough on the "tax" part of the equation. If you held that asset for 365 days or less, you aren’t paying the "cool" investor rate. You’re paying the same rate you pay on your 9-to-5 paycheck.

Federal short term capital gains tax is one of those things that catches people off guard every April. It’s not a separate, special tax bracket. It’s just your ordinary income tax rate. If you’re in the 24% bracket because of your salary, your short-term flip is taxed at 24%. Simple. Brutal. But simple.

The One-Year Line in the Sand

The IRS is obsessed with calendars. Specifically, they care about the "holding period." If you buy a stock on January 1st and sell it on January 1st of the following year, you’ve held it for exactly one year. Is that long-term? Nope. You need to hold it for more than a year—at least one year and one day—to qualify for the lower long-term rates.

Short-term gains apply to almost anything you sell for a profit: stocks, bonds, precious metals, real estate (that isn't your primary residence), and even that digital art piece you bought on a whim. The tax isn't triggered when the value goes up; it’s triggered the moment you "realize" the gain. Selling is the trigger. Trading one cryptocurrency for another is also a trigger, which is a mistake that haunts people during tax season.

Why the Rates Feel So High

Most investors dream of the 0%, 15%, or 20% long-term rates. But for federal short term capital gains tax, you’re looking at the standard seven-tier progressive tax system. For the 2025 and 2026 tax years, those brackets range from 10% all the way up to 37%.

Think about it this way. If you’re a high-earner in California or New York, you aren’t just paying that 37% federal top rate. You’re also potentially hitting the 3.8% Net Investment Income Tax (NIIT) if your income is high enough, plus whatever your state wants. Suddenly, your "quick win" is being taxed at over 50%. It’s enough to make you want to put your money under a mattress. But don't do that. Inflation will eat it anyway.

📖 Related: GA 30084 from Georgia Ports Authority: The Truth Behind the Zip Code

The Math Behind the Madness

Let's look at a quick, illustrative example. Imagine Sarah. Sarah is a software engineer making $170,000 a year. She’s single. In 2025, that puts her firmly in the 24% tax bracket. She decides to try her hand at day trading. Over three months, she nets $10,000 in profit.

When tax time rolls around, that $10,000 isn't treated as special "investment income." The IRS just adds it to her $170,000. Now, her taxable income is $180,000. She owes $2,400 on those gains. If she had just waited 366 days to sell, and assuming her income stayed the same, she would likely have paid 15% ($1,500). That’s a $900 difference just for being patient.

Does Everything Count as a Short-Term Gain?

Not quite. There are weird exceptions. Collectibles, like that vintage comic book or a rare coin, are taxed at a maximum of 28% if held long-term, but they still follow ordinary rates if held short-term. Then there’s Section 1256 contracts—things like regulated futures contracts. These get a "60/40" split. 60% is taxed at long-term rates and 40% at short-term rates, regardless of how long you held them. It’s a loophole big enough to drive a truck through, which is why professional traders love futures.

The Secret Weapon: Tax-Loss Harvesting

If you’re staring at a massive bill for your federal short term capital gains tax, you need to look at your losers. Seriously. This is where "Tax-Loss Harvesting" comes in.

The IRS allows you to use your capital losses to offset your capital gains. If you made $10,000 on Stock A but lost $8,000 on Stock B, you only owe taxes on the $2,000 difference. It’s a net game. If your losses actually exceed your gains, you can use up to $3,000 of that excess loss to offset your "ordinary" income—like your salary. Anything beyond that $3,000 gets "carried forward" to future years. It’s like a tax-saving gift to your future self.

👉 See also: Jerry Jones 19.2 Billion Net Worth: Why Everyone is Getting the Math Wrong

But watch out for the Wash Sale Rule. If you sell a stock at a loss just to take the tax break, but then buy it back within 30 days, the IRS says "nice try." They’ll disallow the loss. You have to stay out of the position for at least 31 days to make it stick.

How to Actually Plan for This

You shouldn't let the tax "tail" wag the investment "dog." If a stock is crashing and you need to get out, get out. Don't wait for the one-year mark just to save on taxes while your principal evaporates. That’s bad math.

However, if you’re sitting on a gain and you’re at month 11, it pays to be disciplined. Check your brokerage statements. Most platforms like Fidelity, Schwab, or Vanguard have a "Cost Basis" tab. It will literally tell you which shares are "short-term" and which are "long-term."

The NIIT Factor

If your Modified Adjusted Gross Income (MAGI) is over $200,000 (single) or $250,000 (married filing jointly), you get hit with an extra 3.8% tax on your investment income. This is the Net Investment Income Tax, born from the Affordable Care Act. It applies to your federal short term capital gains tax too.

Basically, the more you make, the more the government wants to "help" you spend it. Being aware of these thresholds is vital. If you’re right on the edge of the NIIT threshold, maybe you don't sell that asset until January 1st of next year. Timing is everything in tax planning.

✨ Don't miss: Missouri Paycheck Tax Calculator: What Most People Get Wrong

What People Often Get Wrong

A common myth is that you can't use long-term losses to offset short-term gains. You can. The IRS has a specific "ordering rule."

- Short-term losses offset short-term gains.

- Long-term losses offset long-term gains.

- If you have leftover losses in one category, they can offset gains in the other.

So, if you have a massive long-term loss from a housing deal that went south years ago, you can use that to wipe out the federal short term capital gains tax on your current stock flips.

Another misconception is that tax brackets are "all or nothing." If you move into a higher bracket, only the money in that bracket is taxed at the higher rate. Your first $11,000-ish is still taxed at 10%, even if you’re a millionaire.

Real World Nuance: The "Specific Identification" Method

When you sell shares, most brokers defaults to "FIFO"—First In, First Out. This means they assume you’re selling the oldest shares you own. But what if your oldest shares are the ones with the massive gains? You can actually choose "Specific Identification." You tell the broker, "Hey, sell the shares I bought on June 12th for $50, not the ones I bought three years ago for $10." This gives you incredible control over your tax liability.

Moving Forward With Your Portfolio

Managing your tax burden isn't about being shady; it’s about being efficient. The tax code is a set of rules. If you play by them, you keep more of your money.

- Audit your holding periods. Before you click "sell," check if you’re at day 360 or day 366. That one week could save you thousands.

- Review your losers. Before December 31st, look for underperforming assets you want to exit anyway. Use those losses to neutralize your gains.

- Consider your accounts. Capital gains tax doesn't exist inside a 401(k) or a Roth IRA. If you’re a frequent trader, do the heavy lifting in those tax-advantaged accounts.

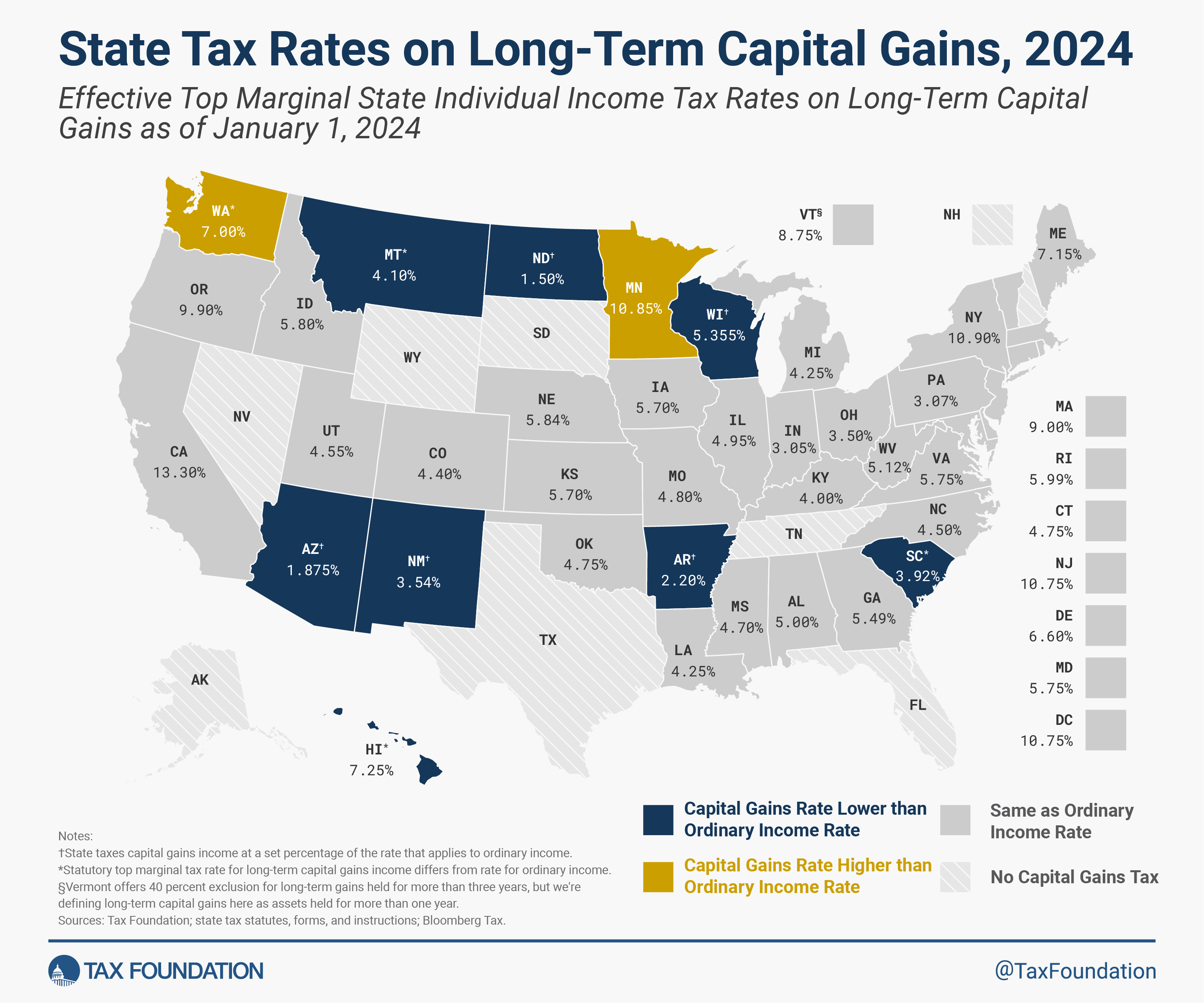

- Track your state rules. Remember, states like Florida and Texas have no income tax, so you only worry about the federal level. If you’re in California, prepare for another double-digit hit.

- Talk to a pro. If your gains are in the six-figure range, a CPA isn't an expense; they’re an investment. They can spot things like the "Section 1202" exclusion for small business stock that could potentially wipe out your tax bill entirely.

The goal isn't to avoid taxes—it's to avoid overpaying. Stay liquid, stay informed, and keep a close eye on that 366-day mark.