If you’ve been scrolling through financial news lately, you’ve probably seen some noise about the federal income tax brackets 2026. It’s messy. Most people think taxes are a static thing that just "exist," but we are actually hurtling toward one of the biggest tax shifts in decades.

Tax law is weird. It’s basically a ticking time bomb.

Back in 2017, the Tax Cuts and Jobs Act (TCJA) changed everything. It lowered rates. It doubled the standard deduction. It made life simpler for a lot of people and way more complicated for others. But here is the kicker: those changes weren't permanent. They were "sunset" provisions. Unless Congress gets its act together and passes new legislation, the tax code is scheduled to revert back to the old, higher 2017-era rules on January 1, 2026.

Wait.

Does that mean your taxes are going up? Probably. Unless you're in a very specific niche of the economy, the 2026 shift is going to feel like a cold shower. We aren't just talking about a few bucks here and there. We are talking about the fundamental way your income is sliced and diced by the IRS.

What is actually happening to the federal income tax brackets 2026?

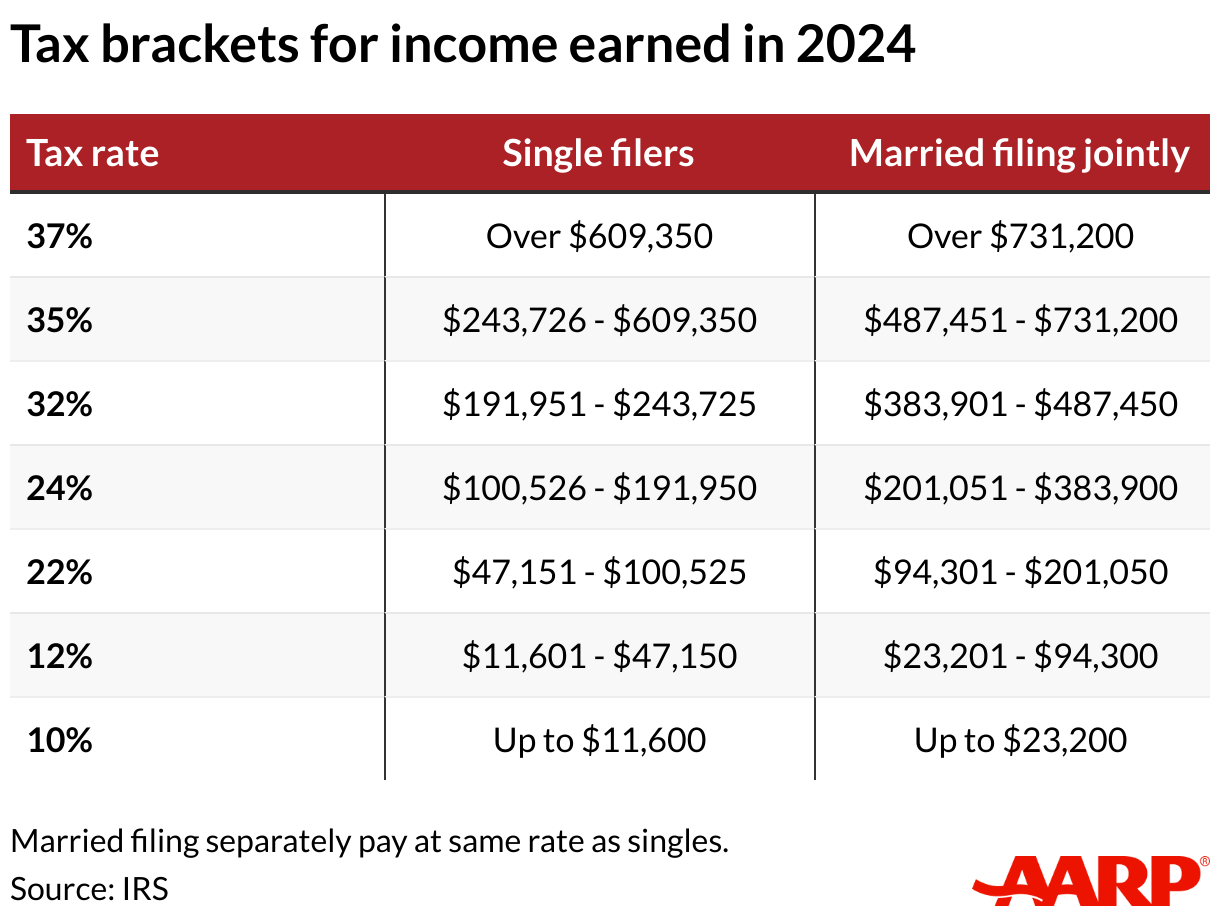

Let’s be real. The IRS doesn't just take a flat percentage of your money. It’s a ladder. You pay a little bit on the first chunk, a bit more on the second, and so on. Right now, in 2024 and 2025, those "rungs" on the ladder are relatively low. The top rate is 37%.

In 2026, that top rate is scheduled to jump back to 39.6%.

But it’s not just the rich who get hit. The 12% bracket? That likely becomes 15%. The 22% bracket? Say hello to 25%. Even the 24% bracket is looking at a jump to 28%. It’s a cascade. If you’re earning a middle-class salary, you’re looking at a 3% raise for the government that you didn't agree to.

Think about it this way. If you’re a single filer making $95,000, you’re currently sitting comfortably in the 22% bracket for your top dollars. In 2026, that same income could easily be taxed at 25%. That’s thousands of dollars vanishing from your yearly budget. Poof. Gone.

The Standard Deduction vs. Itemizing: The 2026 Flip

One of the biggest reasons people stopped complaining about taxes for a few years was the standard deduction. It got huge. For 2025, it's roughly $15,000 for singles and $30,000 for married couples. It’s easy. You just take the deduction and move on with your life.

In 2026, that deduction is set to be cut nearly in half.

Suddenly, everyone is going to be digging through their shoeboxes for old receipts again. Remember the "SALT" deduction? The State and Local Tax deduction? It’s currently capped at $10,000. That cap is also supposed to disappear in 2026. If you live in a high-tax state like California, New York, or New Jersey, this is actually the one "bright spot" in a sea of bad news. You might finally be able to deduct your full property taxes and state income taxes again.

But for the average person in a low-tax state? You lose a massive chunk of your standard deduction and get nothing in return. It’s a net loss.

Honestly, it feels like a step backward into a more bureaucratic era of American life.

Mortgage Interest and the $750k Limit

If you bought a house recently, you know about the $750,000 limit on mortgage interest deductions. That was a TCJA rule. If we revert to the old ways in 2026, that limit actually goes up to $1 million.

It’s a weird irony. While the federal income tax brackets 2026 are getting tighter, certain deductions for homeowners with massive mortgages might actually get more generous. It’s the kind of nuance that makes tax planning such a headache. You’re paying more in base rates but potentially saving more on your mansion. Not exactly a win for the little guy.

📖 Related: Cómo está el dólar a México: Lo que nadie te explica sobre el superpeso este 2026

Why "Bracket Creep" is Your Silent Enemy

Inflation is a beast. We’ve all felt it at the grocery store. But inflation also messes with your taxes through something called "bracket creep."

Usually, the IRS adjusts the brackets for inflation so you don't get pushed into a higher bracket just because your boss gave you a 3% cost-of-living raise. However, when the underlying rates change—like they are scheduled to do in 2026—the inflation adjustments can't save you. You are being pushed into a higher percentage bracket regardless of whether your "real" purchasing power has increased.

It's a double whammy.

You're paying more for eggs, and you're paying a higher percentage of your paycheck to the federal government.

The Politics of the 2026 Cliff

Let’s be clear: this isn't set in stone because of some law of nature. It’s a political choice. Congress could vote tomorrow to extend the current rates. They could even lower them. But we live in a world of gridlock.

Budget hawks are worried about the national deficit.

Social advocates want more revenue for programs.

The result? A stalemate that leads us right off the cliff.

If you’re waiting for a "tax hero" to ride in and save the day before 2026, don't hold your breath. Both parties will likely use these tax brackets as leverage in a massive game of chicken. It’s going to be a loud, messy 2025 in Washington.

The Impact on Small Business Owners

If you’re a freelancer or a small business owner, you probably love the Section 199A deduction. It’s that 20% "pass-through" deduction that lets you keep more of your hard-earned cash.

Guess what? That’s on the chopping block too.

If that 20% deduction disappears alongside the shift in federal income tax brackets 2026, small business owners are looking at a massive spike in their effective tax rate. We are talking about a potential 10% or more increase in what they owe. That’s the difference between hiring a new employee or closing up shop for some folks. It’s serious.

Real World Example: The "Typical" Family

Let’s look at a hypothetical. The Miller family. They make $120,000 combined. They have two kids.

Under the 2024/2025 rules, they get a massive standard deduction and a healthy Child Tax Credit ($2,000 per kid).

📖 Related: What Really Happened When Costco Replaces Pepsi With Coca Cola Products In Food Courts

In 2026, their tax bracket jumps from 12% to 15% (for that portion of their income). Their standard deduction drops. The Child Tax Credit is scheduled to drop from $2,000 back to $1,000 per child. Oh, and it's no longer fully refundable.

The Millers aren't "rich" by any stretch of the imagination, but they are looking at a tax bill that could easily be $3,000 to $5,000 higher. That’s a used car. That’s a year of groceries. That’s a lot of pressure.

Strategies to Get Ahead of the 2026 Shift

You can't control the law, but you can control your timing. If you know rates are going up in 2026, you might want to change how you handle your money in 2025.

Accelerate your income. If you’re a business owner or have control over bonuses, it might make sense to pull that income into 2025 while the rates are still lower. Why pay 39.6% later when you can pay 37% now?

Rethink your Roth. If you’ve been on the fence about a Roth conversion, 2025 might be the last "cheap" year to do it. You pay the tax now at the current low rates so you never have to pay tax on that money again. If you wait until 2026, that conversion is going to cost you more in upfront taxes.

Watch your capital gains. While the 2026 shift mostly targets "ordinary" income, the overall tax environment is getting stickier. If you have big stock wins, locking them in before the dust settles might be a smart play.

The Alternative Minimum Tax (AMT)

Remember the AMT? It was that "ghost tax" that used to haunt the middle class. The TCJA basically killed it for most people by raising the exemption levels.

In 2026, the AMT is coming back from the dead.

✨ Don't miss: Cómo se escribe mil dólares en inglés sin cometer errores de principiante

If you have a lot of deductions or specific types of income, you might find yourself caught in this parallel tax system again. It’s another layer of complexity that’s been missing for a few years, and honestly, nobody missed it.

Don't Panic, But Do Plan

The 2026 tax landscape looks daunting, but it’s mostly about preparation. The worst thing you can do is pretend it isn't happening. Ignorance is definitely not bliss when the IRS is involved.

- Audit your current withholding. Check your paystubs. Are you barely breaking even now? If so, you're going to owe a lot more in 2026.

- Talk to a pro. A good CPA is worth their weight in gold right now. They can run "what-if" scenarios for your specific 2026 situation.

- Max out those pre-tax accounts. If your tax rate is going up, your 401(k) and HSA contributions become even more valuable because they lower your taxable income.

- Keep an eye on the news. This is a moving target. If Congress passes a "Tax Extension Act," all of this could change overnight.

The federal income tax brackets 2026 represent a major pivot point in American finance. Whether you're a high-earner or just trying to get by, the rules of the game are changing. The era of "easy" tax filing and historically low rates is closing. It’s time to tighten the belt and look at the numbers.

Start looking at your 2025 year-end planning as a bridge to 2026. If you can shift expenses into 2026 and income into 2025, you are already winning. It’s about being proactive rather than reactive. Don't let the 2026 tax cliff catch you by surprise. Your bank account will thank you.