You’ve probably seen those glossy brochures from review providers promising that their example CPA exam questions are the exact replicas of what you’ll face on test day. Honestly? They’re close, but they often miss the "vibe" of the actual Prometric experience. It’s one thing to calculate a depreciation schedule in the quiet of your bedroom; it’s a whole different animal when you’re four hours deep into a testing center session, the person next to you is coughing, and the simulation window won’t resize properly.

The CPA exam isn't just a test of what you know. It’s a test of how much misery you can tolerate while still remembering how to account for a non-monetary exchange with commercial substance.

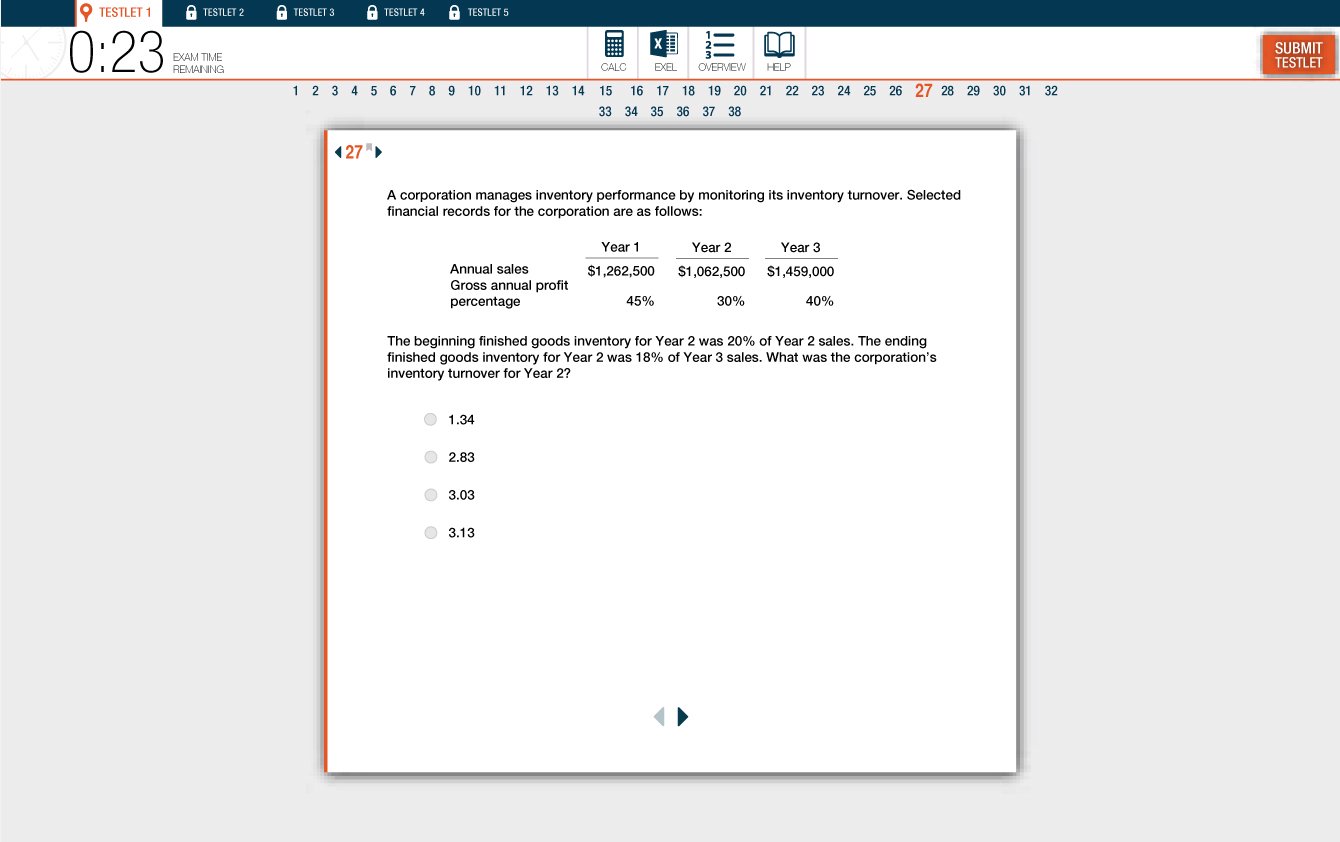

Why Real Example CPA Exam Questions Feel Different

If you look at released questions from the AICPA, you’ll notice they’re surprisingly brief. Most prep courses—Becker, UWorld, Surgent—actually make their practice questions harder and more wordy than the actual exam to over-prepare you. It’s a classic "train hard, fight easy" mentality. But the real exam has a specific brand of trickery. It’s not always about the math. Sometimes, it’s about one single word like "except" or "not" buried in a three-paragraph prompt.

Take a standard Financial Accounting and Reporting (FAR) question. You might get a wall of text about a company's year-end adjustments. It looks intimidating. You see numbers for unearned revenue, prepaid insurance, and accrued liabilities. But then you read the actual call of the question: "What is the total effect on current assets?" Suddenly, half that data is garbage. You don't need the liability info. The exam loves to give you "noise" to see if you can filter it out.

The Auditing (AUD) Mindset Trap

In AUD, the questions aren't math-heavy. They’re linguistic puzzles. You’ll see four answers that all look "correct." You’re not looking for the right answer; you’re looking for the best answer according to GAAS (Generally Accepted Auditing Standards).

Example: "Which of the following procedures would an auditor most likely perform to identify unusual transactions?"

- Scanning the general ledger.

- Inquiring of the janitorial staff.

- Checking the CEO’s Twitter.

- Vouching a sample of invoices.

Now, obviously, 2 and 3 are nonsense. But between 1 and 4? Both are valid. However, the AICPA loves the word "scanning" when it comes to "identifying" things. It’s that subtle distinction that makes practice questions so vital. You start to learn the "AICPA-speak."

Breaking Down Task-Based Simulations (TBS)

TBS are where dreams go to die. Or at least where the most points are lost. These aren't just example CPA exam questions; they are mini-work projects. You might have to open six different PDF "exhibits"—an invoice, a memo, an email from a CFO, a bank statement—and reconcile them all.

A common simulation involves adjusting a trial balance. You’ll be given a list of accounts and then five "findings" from an audit. You have to decide if an adjustment is needed and, if so, by how much. Most students fail here because they lose track of time. You have to be ruthless. If a simulation is taking more than 20 minutes, you’re in the danger zone.

The Evolution of the Exam in 2024 and Beyond

The "CPA Evolution" model changed things. We now have the Core (FAR, AUD, REG) and the Disciplines (ISC, TCP, BAR).

- BAR (Business Analysis and Reporting): Basically FAR on steroids. Lots of technical stuff.

- ISC (Information Systems and Controls): Heavy on IT audit and data.

- TCP (Tax Compliance and Planning): For the people who actually enjoy reading the Internal Revenue Code.

If you’re looking at older example CPA exam questions, be careful. The BEC (Business Environment and Concepts) section is gone. If your practice material is asking you to write a memo about corporate governance in the BEC format, you’re studying for a ghost exam.

The Strategy of Guessing

Here is a secret: the CPA exam is curved, sort of. It’s actually graded using Item Response Theory (IRT). This means not all questions are worth the same amount of points. Harder questions carry more weight. Also, there are "pretest" questions in every section—these don't count for your score at all. They’re just the AICPA testing out new material.

You’ll never know which ones they are.

So, if you hit a question that looks like it was written in ancient Greek, don't panic. It might be a pretest. Pick "C" and move on. Don't let one weird question ruin your mental state for the next fifty.

Real-World Example: A Regulation (REG) Scenario

Let’s look at a typical REG question involving Gift Tax.

Scenario: "In 2024, Sarah gives her brother $20,000 in cash. She also pays $15,000 directly to a university for her niece's tuition. How much of these gifts are taxable?"

A lot of people start doing math. They subtract the annual exclusion ($18,000 for 2024). They think, "Okay, $20k - $18k = $2k taxable." But they forget the rule: payments made directly to an educational institution for tuition are 100% exempt.

The answer is $2,000.

This is how the exam works. It tests the rule (exclusion limit) and the exception (direct tuition payments) simultaneously.

Why You Should Use Multiple Sources

No single test bank is perfect. Becker is the gold standard, but it's pricey. Ninja CPA is great for "sparring" with extra questions. If you find yourself memorizing the answers to your practice questions rather than understanding the concepts, you're in trouble. Switch banks. Get a fresh set of eyes on the material.

The Mental Game of the Four-Hour Window

You get a 15-minute break that doesn't stop the clock between testlets three and four. Take it. Seriously. Go eat a protein bar. Splash water on your face. The "Example CPA exam questions" you see in your textbooks don't simulate the physical fatigue of sitting in a sterile room for 240 minutes.

📖 Related: Holly O'Neill Bank of America: Why Her Retail Strategy Actually Works

How to Evaluate Your Practice Scores

Don’t aim for 100% on practice exams. If you’re scoring in the 65-75% range on "random" sets of questions, you’re likely ready for the real thing. This is known in the community as the "Becker Bump." People often score 10-15 points higher on the actual exam than they do on their mock exams because the practice software is designed to be more punishing.

Immediate Next Steps for Your Studies

Stop scrolling through forums and start a "targeted" session. Pick the one topic you absolutely hate—maybe it’s Leases, maybe it’s Consolidation—and do 20 multiple-choice questions right now.

- Identify your "weakest link" by looking at your software's performance dashboard.

- Ignore the "Overall Score" and look at your "Trending Score" over the last 100 questions.

- Practice with a basic calculator and a digital whiteboard, as that's all you get at the Prometric center.

- Download the AICPA sample test directly from their website. It’s the only place to see the actual software interface you’ll be using on the big day.