Honestly, if you’ve been watching the Domino's Pizza share price lately, you might be feeling a little bit like a delivery driver stuck in a snowstorm. Cold. Frustrated. Wondering when things will finally speed up.

As of January 16, 2026, the stock is sitting at around $400.28. Just a few days ago, it was hovering closer to $425. That’s a roughly 6% drop in two weeks. If you look at the 52-week high of **$500.55**, it’s clear the "dough" isn't rising quite as fast as investors hoped. But before you write off DPZ as a cold slice of yesterday’s dinner, there is a lot of nuance under the surface that the headlines are missing.

Wall Street is currently having a bit of an argument about this one. Some analysts, like the folks at Evercore ISI, recently trimmed their price targets from $510 down to $490. On the flip side, you have big-name firms like Argus Research still pinning their hopes on a $600 price point. That is a massive gap. It basically tells you that nobody is 100% sure if Domino's is a tech company that happens to sell pizza, or just another fast-food joint fighting for scraps in a crowded market.

Why the Market is Acting So Weird

The "Hungry for MORE" strategy—which is basically CEO Russell Weiner’s master plan—has been doing some heavy lifting. In late 2025, they posted a 5.2% jump in U.S. same-store sales. That’s actually huge. It was their best performance in six quarters. People are obsessed with the Parmesan Stuffed Crust, and the "Best Deal Ever" promotion actually lived up to its name by driving a ton of foot traffic.

But here is the kicker.

While the sales are up, the Domino's Pizza share price hasn't exactly gone parabolic. Why? Because the cost of doing business is getting expensive. We are talking about "food basket" prices rising over 3%. Flour, cheese, cardboard—it all adds up. Then you have wage inflation. It’s harder and more expensive to keep drivers on the road, especially when they’re competing with every other gig-economy app out there.

🔗 Read more: The Gary I Knew: Why the Gary Vaynerchuk You See Online Isn't the Whole Story

The Delivery Dilemma

For years, Domino's refused to play ball with third-party apps. They were the lone wolves of delivery. Now? They’ve fully embraced DoorDash.

- The Good: It opens them up to a massive pool of customers who only shop via apps.

- The Bad: It eats into those precious margins.

- The Reality: CFO Sandeep Reddy has noted that while DoorDash is a "meaningful contributor," it’s a balancing act.

Investors are worried that by joining the aggregators, Domino's is losing its secret sauce—the efficiency of its own closed-loop delivery system. If everyone is on DoorDash, does Domino's still have an edge?

By the Numbers: What’s Actually Happening?

If you like hard data, the trailing P/E ratio is sitting around 23.37. For a company that’s consistently growing its earnings per share (EPS is currently about $17.13), that’s not necessarily "expensive," but it’s not "cheap" either.

Check out how the last few weeks have looked for the Domino's Pizza share price:

On January 2nd, the stock opened the year at $425.28. By January 12th, it had dipped to $415.95. Today, we’re looking at that $400 mark. It’s a downward trend, but it’s occurring while the broader restaurant industry is facing a bit of a "macroeconomic chill," as some analysts like to call it. People are tightening their belts. Maybe they aren't ordering the extra side of Cinna Stix this month.

International growth is still the wild card. They added over 180 net stores internationally in just one quarter last year. Places like India and China are massive growth engines for them, but currency fluctuations can make the balance sheet look like a mess even when the business is actually doing great.

Is the Dividend Enough to Keep You?

One thing people forget is that Domino's is a pretty reliable dividend payer. The yield is currently around 1.74%. It’s not going to make you rich overnight, but for a "Hold" rated stock (which is the consensus among 13 out of 29 analysts right now), it’s a nice little consolation prize while you wait for the price to recover.

What Most People Get Wrong

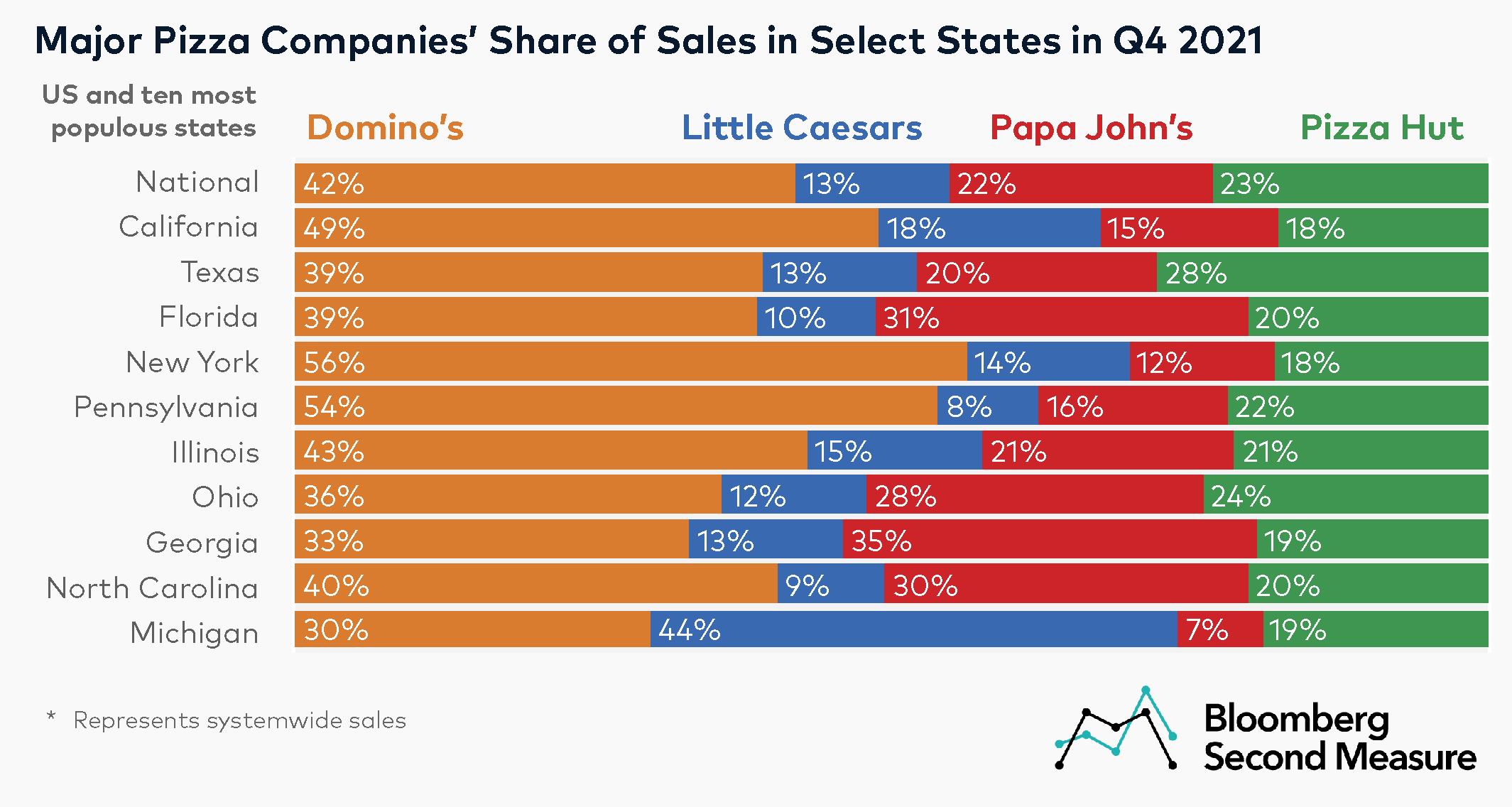

Most retail investors think Domino's is just competing with Pizza Hut or Papa John's. They aren't. They are competing with the "share of stomach."

🔗 Read more: Norwegian Cruise Lines Stock: What Most People Get Wrong

In 2026, the competition is everything from the frozen pizza aisle at the grocery store to the local taco truck that now has a slick mobile app. The reason the Domino's Pizza share price stays resilient is their tech. Their app is basically a fintech product at this point. They know exactly when you’re hungry, what you want, and how to get you to click "Reorder" in under 10 seconds.

That digital dominance is why 12 analysts still have a "Buy" rating on the stock despite the recent dip. They see the long game. They see a company that is successfully navigating the transition from a pure delivery play to a "carryout powerhouse." Carryout sales were up 8.7% recently. That’s pure profit because they don't have to pay a driver or a third-party fee.

Actionable Insights for Your Portfolio

If you’re looking at the Domino's Pizza share price and trying to decide your next move, consider these three factors:

👉 See also: Bitcoin Fear and Greed Index: What Most People Get Wrong

- Watch the $392 Level: This is the 52-week low. If it breaks below this, we might see some panic selling. If it holds, it could be a classic "buy the dip" opportunity.

- The Earnings Catalyst: Keep an eye on the Q1 2026 report. Analysts are expecting an EPS of around $4.44. If they beat that, expect the stock to snap back toward the $450 range quickly.

- Inflation Trends: If cheese and wheat prices start to stabilize, Domino's margins will expand rapidly. Their scale allows them to buy in bulk better than almost anyone else.

The smart money isn't looking at the 6% drop this month. They are looking at the 21.35% average upside that Wall Street analysts are predicting for the next 12 months. Whether they hit that $485 target depends entirely on if they can keep those "Hungry for MORE" customers coming back without spending every penny on advertising.

Check your brokerage app for the latest real-time quote, as the $400.28 price point is a moving target. Set a price alert for $395 if you're looking for an entry point, or $415 if you want to see a confirmation of a trend reversal before jumping in.