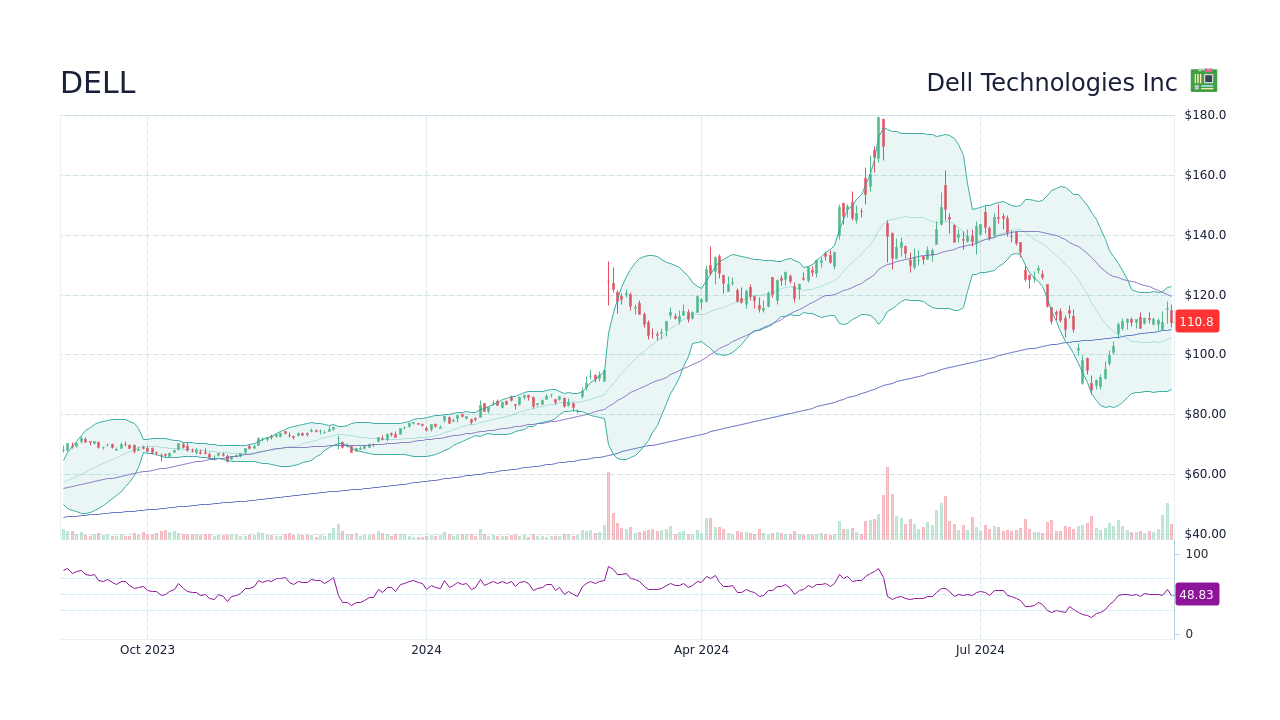

Money moves fast. One day you're looking at a dell computer stock quote and thinking about boring office laptops, and the next, you're staring at a chart that looks like a literal mountain range. It's wild. Most people still associate Michael Dell’s brainchild with those gray towers under desks, but Wall Street has pivoted. It's all about the servers now. Specifically, the massive, heat-generating racks that power artificial intelligence.

If you've checked the ticker recently, you know the volatility is real.

The AI Server Gold Rush

Last year, everyone went nuts for Nvidia. This year? The focus shifted to the "plumbing" of AI. Dell found itself in the right place at the right time with its PowerEdge servers. When Elon Musk or Tier 2 cloud providers need serious horsepower to train LLMs, they don't just buy chips; they buy the whole integrated system. That’s where the money is.

Honestly, the dell computer stock quote started acting like a tech startup rather than a legacy hardware company. We saw the price double in a ridiculously short window because the backlog for AI-optimized servers exploded. But here's the kicker: margins are thin. Hardware is a tough business. You can sell a billion dollars' worth of servers, but if the components (like those pricey H100s) cost you nearly as much, the "bottom line" doesn't always look as pretty as the "top line."

Investors often miss this. They see the revenue growth and hit 'buy,' forgetting that Dell is basically middle-manning the most expensive silicon on the planet.

Understanding the Dell Computer Stock Quote Beyond the Number

When you look up the price today, you’re seeing a reflection of three very different businesses smashed together.

First, there’s the Client Solutions Group. That’s your laptop. It’s steady, it’s reliable, and it’s kinda boring. When companies refresh their fleets every three or four years, Dell wins. Second, you have the Infrastructure Solutions Group. This is the sexy part. This is the AI part. It's the reason the stock broke out of its decade-long slumber. Third, there’s the dividend and buyback play. Dell is a cash cow. They give a lot of that money back to shareholders, which keeps the "value investors" happy even when the "growth investors" are screaming about quarterly margins.

👉 See also: How Much Do Chick fil A Operators Make: What Most People Get Wrong

Why the PC Refresh Cycle is the Secret Weapon

Everyone is talking about AI. I get it. It’s flashy. But don't sleep on the "boring" PC business.

Windows 10 is hitting its end-of-life phase soon. That means millions of enterprise laptops are about to become paperweights. Companies have to upgrade. This creates a massive, predictable wave of demand that usually props up the dell computer stock quote when the server side of the house gets too volatile. It's a safety net.

- Institutional investors love this predictability.

- The AI-PC trend is actually starting to take off, even if consumers don't quite get it yet.

- Higher-end machines mean better margins than the cheap Chromebooks competitors sell.

If you're watching the stock, you've gotta watch the "Core PC" shipment numbers just as closely as the "AI Server" backlog. If one slips, the other has to carry the weight. It's a balancing act that Michael Dell has mastered over forty years.

The Margin Compression Trap

Here is what most people get wrong about Dell. They think "More AI = More Profit." Not always.

In recent earnings calls, the leadership has been very honest about the fact that AI servers are currently lower-margin than their traditional storage products. Why? Because the competition is fierce. Super Micro and HP Enterprise are breathing down their necks. To win the big contracts from companies like Meta or CoreWeave, Dell sometimes has to sharpen the pencil on pricing.

The stock often drops after a "beat and raise" because the gross margins came in a tiny bit lower than some analyst in a suit expected. It's a weird paradox. You're growing faster than ever, but the market punishes you because that growth is "expensive."

✨ Don't miss: ROST Stock Price History: What Most People Get Wrong

The Storage Factor

Storage is the hidden gem.

When you have massive amounts of data for AI, you need somewhere to put it. Dell’s storage business—built largely on the massive EMC acquisition years ago—is high-margin. When a customer buys a rack of AI servers, Dell tries to pull them into their storage ecosystem. That’s where the real profit hides. If you see the storage numbers ticking up in the quarterly report, that’s usually a better sign for the long-term health of the dell computer stock quote than a one-time spike in server sales.

Debt and the Balance Sheet

Dell has a lot of debt. It’s a fact.

They took on a mountain of it to go private and then come back public, and then again to buy EMC. They’ve been aggressively paying it down, which is great. But in a high-interest-rate environment, that debt is a weight. If interest rates stay higher for longer, it eats into the cash they could be using for dividends.

Most retail traders just look at the P/E ratio. That’s a mistake. You have to look at the Free Cash Flow (FCF). Dell is an FCF machine. They are very good at squeezing every penny out of their supply chain. They basically invented the "just-in-time" manufacturing model, and they still use those efficiencies to stay ahead of the pack.

What to Watch for in 2026

We're in a weird spot. The initial "AI hype" has cooled into "AI execution."

🔗 Read more: 53 Scott Ave Brooklyn NY: What It Actually Costs to Build a Creative Empire in East Williamsburg

- Watch the backlog: If the backlog for AI servers starts to shrink, the stock will get hammered.

- Watch the dividend: They’ve been raising it. If that stops, the income investors will flee.

- Watch Michael Dell: He still owns a massive chunk of the company. When he sells, it’s usually for estate planning, but the market still freaks out every time.

Actionable Insights for Investors

If you are tracking the dell computer stock quote with the intention of jumping in, don't just buy the peak of a news cycle. This stock moves in cycles.

Stop looking at the daily price fluctuations and start looking at the 90-day moving average. Dell tends to overextend on good news and over-correct on bad news. It's a "trader's stock" disguised as a "grandpa stock."

Check the "Book-to-Bill" ratio in their earnings reports. If they are booking more orders than they are billing, growth is accelerating. If that ratio slips below 1.0, it’s time to be cautious. Also, keep an eye on Nvidia’s supply chain. If Nvidia can’t ship chips, Dell can’t ship servers. It’s that simple.

Monitor the enterprise spend surveys from firms like Gartner or IDC. If IT budgets are tightening, Dell is the first to feel it. But if companies are shifting "Legacy IT" budget into "AI IT" budget, Dell is perfectly positioned to capture that flow.

The smartest move is usually to wait for the "post-earnings dip." Dell has a historical habit of dropping 5-10% right after reporting, even if the news is good, simply because the "whisper numbers" on margins are so hard to hit. That’s usually the entry point people look for.

Keep your eye on the total debt-to-equity ratio as well. As that number drops, the company becomes much more attractive to conservative institutional funds that were previously scared off by the leveraged balance sheet. Dell is transforming from a high-debt hardware play into a lean, AI-infrastructure powerhouse. It’s a messy transition, but the numbers don't lie.

Focus on the cash flow, ignore the flashy headlines about "AI PCs" until they actually show up in the revenue column, and remember that hardware is a game of scale. Nobody has more scale than Dell.