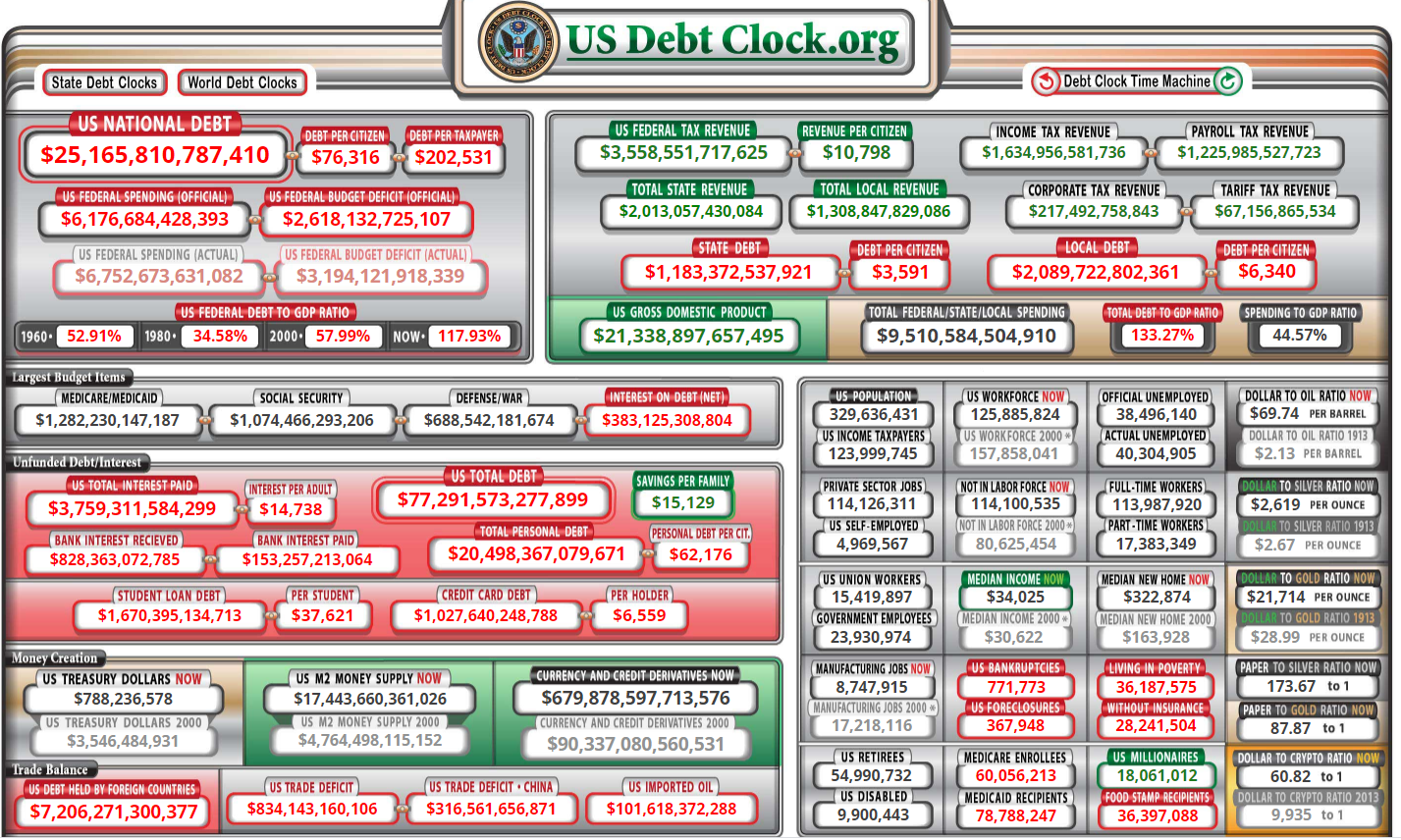

You’ve seen the big numbers. They’re everywhere. The flickering red digits of the debt clock in Midtown Manhattan or the frantic headlines about "fiscal cliffs." But honestly, the current US national debt 2025 is no longer just a "big number" problem. It's a "math doesn't work anymore" problem.

As of late 2025, the total gross national debt has rocketed past $38 trillion. To be precise, we hit the $38 trillion milestone in October 2025, just 71 days after crossing $37 trillion. It's moving fast.

Why the Current US National Debt 2025 Feels Different

For decades, economists told us not to worry. They said as long as the economy grew faster than the debt, we were fine. Well, the script changed. We’re now looking at a debt-to-GDP ratio that has blown past 120%. Basically, we owe significantly more than our entire economy produces in a year.

It’s kinda like having a credit card balance that is bigger than your annual salary. Most people can handle a few thousand in debt if they make $100k. But what if you make $100k and owe $125k, and the interest rate just doubled? That’s where the US government is sitting right now.

✨ Don't miss: Rivian Current Stock Price: What Most People Get Wrong

The Interest Trap

The real killer isn't the total debt; it's the cost to keep the lights on. For a long time, interest rates were essentially zero. The government could borrow for free. Not anymore.

- Net interest payments are now one of the largest line items in the federal budget.

- In 2025, the US began spending more on interest than on the entire national defense budget.

- We are currently paying roughly $2 billion to $3 billion a day just in interest.

That is money not going to schools, roads, or healthcare. It’s just vanishing into the pockets of bondholders.

The Politics of the $38 Trillion Hole

Washington is currently in a weird spot. On one hand, you have the "One Big Beautiful Bill" signed in the summer of 2025, which aimed to slash some taxes but also added trillions in long-term borrowing. On the other hand, there’s the new Department of Government Efficiency (DOGE), led by figures like Elon Musk and Vivek Ramaswamy, trying to hack away at the fat.

It’s a tug-of-war.

DOGE claimed over $110 billion in savings early on by terminating old contracts and leases. That sounds like a lot. It’s not. When you’re adding $1 trillion in debt every 100 days, $110 billion is basically a rounding error. It’s like trying to bail out the Titanic with a thimble.

Who actually owns this debt?

Most people think China owns us. That’s a myth. Honestly, the biggest owner of US debt is... the US.

- Social Security Trust Funds: The government borrows from itself.

- The Federal Reserve: They buy bonds to manage the economy.

- Private Investors: Your 401(k) probably holds Treasury bonds.

- Foreign Nations: Japan and China are big holders, but they only own a fraction of the total.

What Happens Next?

If you're looking for a silver lining, it’s tough to find one in the raw data. The Congressional Budget Office (CBO) is projecting that if we don't change course, the debt will hit 150% of GDP in the coming decades.

📖 Related: Finding Your Next Meal: Why the Fast Food Chain Map is Changing So Fast

Jamie Dimon, the CEO of JPMorgan Chase, called this the “most predictable crisis” in history. Ray Dalio has warned of an “economic heart attack” if the world loses faith in the dollar. But the US dollar is still the world's reserve currency. For now, everyone still wants our debt because there isn't a safer place to put money.

But "for now" is doing a lot of heavy lifting.

Actionable Steps for Your Money

You can't fix the national debt, but you can protect yourself from the fallout. High debt usually leads to two things: higher taxes or higher inflation (or both).

👉 See also: 0005 hk stock price: Why Everyone Is Suddenly Obsessed With HSBC Again

- Diversify away from the dollar: Consider assets that aren't tied to US government solvency, like international stocks, gold, or even a small slice of crypto if that's your vibe.

- Watch the interest rates: If the government has to pay more to borrow, your mortgage and car loan rates aren't going down anytime soon. Lock in fixed rates when you can.

- Hedge against tax hikes: With the current US national debt 2025 levels, the government will eventually need more revenue. Roth IRAs are looking better and better because you pay the tax now at today's rates, rather than whatever crazy rate they might invent in 2040.

The math is getting harder to ignore. We are living through a massive fiscal experiment, and 2025 might be the year we realize the lab is starting to smoke. Keep an eye on the Treasury's "Debt to the Penny" updates; it's the only honest scoreboard we have left.