Honestly, the way people talk about the federal budget feels a lot like how families argue over a credit card bill at the kitchen table. But there is a massive, trillion-dollar difference. When you or I overspend, the bank eventually cuts us off. When the U.S. government does it, they just print more "checks" or issue more bonds.

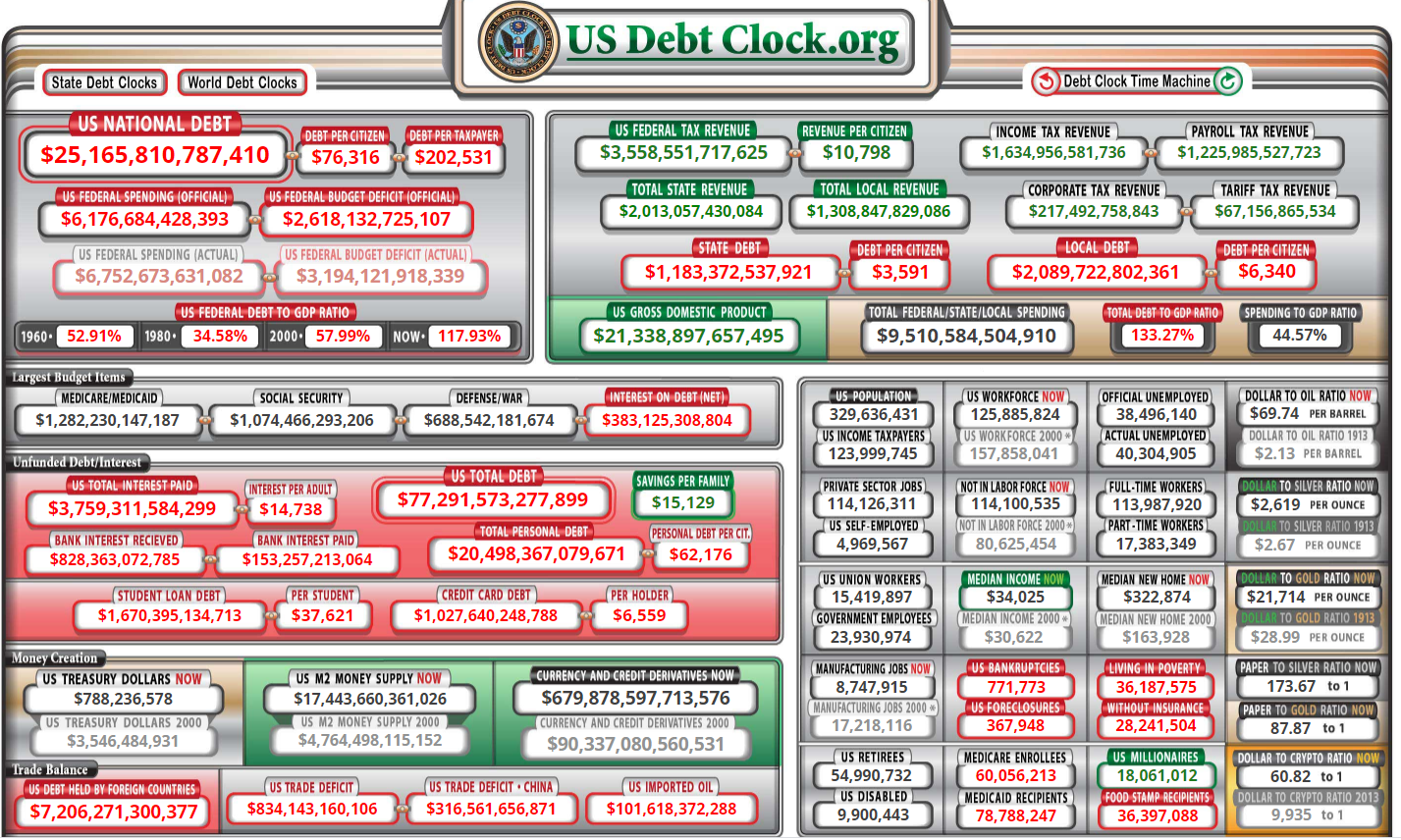

As of early 2026, the current national debt 2025 figures have officially crossed into territory that even seasoned economists find a bit dizzying. We are looking at a total gross national debt of roughly $38.43 trillion.

To put that in perspective, that is about $285,127 per household.

It’s a number so large it basically loses all meaning. It becomes background noise. But 2025 was a weirdly pivotal year for this pile of IOUs. We saw the passage of the "One Big Beautiful Bill Act" (OBBBA), which added trillions in projected spending, and a series of tariffs that shifted how money flows into the Treasury. If you feel like the ground is shifting under your feet regarding inflation and interest rates, you're not imagining it.

✨ Don't miss: Taylor Swift Masters Cost: What Really Happened with the $300 Million Deal

The $38 Trillion Elephant in the Room

Most people think the debt is just one big "amount owed." It’s actually more like a layered cake.

You've got the debt held by the public, which is about $30.8 trillion. This is the stuff held by investors, foreign governments, and probably your own 401(k) via Treasury bonds. Then you have intragovernmental debt, which is basically the government borrowing from its own pockets, like the Social Security Trust Fund.

During 2025, the debt grew by about $8 billion every single day.

That's not a typo.

Every hour, the debt climbed by more than $330 million. It’s relentless. The Congressional Budget Office (CBO) had originally hoped for a bit more stability, but between farm aid packages and new tax provisions, the "net new debt" added in 2025 alone hit $1.5 trillion.

Why 2025 Changed the Math on Interest

For a long time, the debt didn't "hurt" because interest rates were basically zero. It was like having a million-dollar mortgage with a 0.5% interest rate; it’s a lot of money, but the monthly payment is a breeze.

💡 You might also like: Why Every College Student Business Card Strategy Is Probably Wrong

That era is dead.

By December 2025, the average interest rate on our marketable debt climbed to about 3.36%. That sounds low compared to a credit card, but when you apply it to $38 trillion, the math gets scary fast. We are now spending roughly **$970 billion a year just on interest**.

Think about that.

We are paying nearly a trillion dollars a year just to "stay current" on the debt, without actually paying back a dime of the principal. In 2025, interest payments became one of the fastest-growing parts of the federal budget, actually rivaling the entire defense budget.

What Most People Get Wrong About the "Collapse"

You'll hear people on the news claiming the U.S. is going "bankrupt."

Kinda, but not really.

A country that prints its own currency can’t technically go bankrupt in the traditional sense. It can always create more dollars to pay the bill. The real risk isn't a "shuttered window" at the Treasury; it's inflation. If the world decides those dollars aren't worth as much because there are too many of them, your groceries get more expensive.

That is the hidden tax of the national debt.

In late 2025, we saw inflation stay stubbornly above the 2% target, partly due to the friction of new tariffs and the sheer volume of government spending. When the government competes with you for loans, it pushes interest rates up for everyone. Your mortgage, your car loan, and your business credit line all feel the weight of that $38 trillion.

The Looming Deadlines of 2026

We entered 2026 with some pretty heavy baggage from the previous year.

- The Debt Limit: In early 2025, the CBO warned that "extraordinary measures" would run out by late summer. We narrowly avoided a default, but the political scars remained.

- The 2017 Tax Act Expirations: Many of the tax cuts from years ago are scheduled to sunset. If they aren't extended, taxes go up. If they are extended, the debt grows even faster. It's a classic "pick your poison" scenario.

- The $39 Trillion Milestone: At the current pace, we are expected to hit $39 trillion by April 2026.

What You Can Actually Do

It’s easy to feel helpless when the numbers have twelve zeros. But fiscal policy eventually hits your dinner table.

First, watch the 10-year Treasury yield. It’s the benchmark for almost all consumer debt. When the government’s borrowing costs go up, yours do too. If you’re planning to buy a home or refinance, 2025 taught us that waiting for "rock bottom" rates might be a losing game.

Second, diversify your "inflation hedges." Since the primary risk of the national debt is the devaluation of the dollar, owning assets like stocks, real estate, or even certain commodities can act as a buffer.

Third, stay informed on tax changes. The 2025 legislative session was chaotic, and the ripple effects on capital gains and income brackets will be felt through 2026.

✨ Don't miss: News About UPS Today: Why Your Shipping Costs Are Actually Shifting

The national debt isn't going to disappear. There is no political will in Washington—on either side of the aisle—to actually balance the books. The goal for you shouldn't be to "fix" the country's balance sheet, but to make sure your own balance sheet is resilient enough to handle the volatility.

Next Steps for Your Finances:

- Review your fixed-rate vs. variable-rate debt. With interest costs rising for the government, variable rates are increasingly risky.

- Consult with a tax professional about the 2025 tax law changes to see how your specific bracket is affected.

- Look at your investment portfolio’s exposure to inflation. If the dollar weakens under the weight of $39 trillion in debt, are you protected?