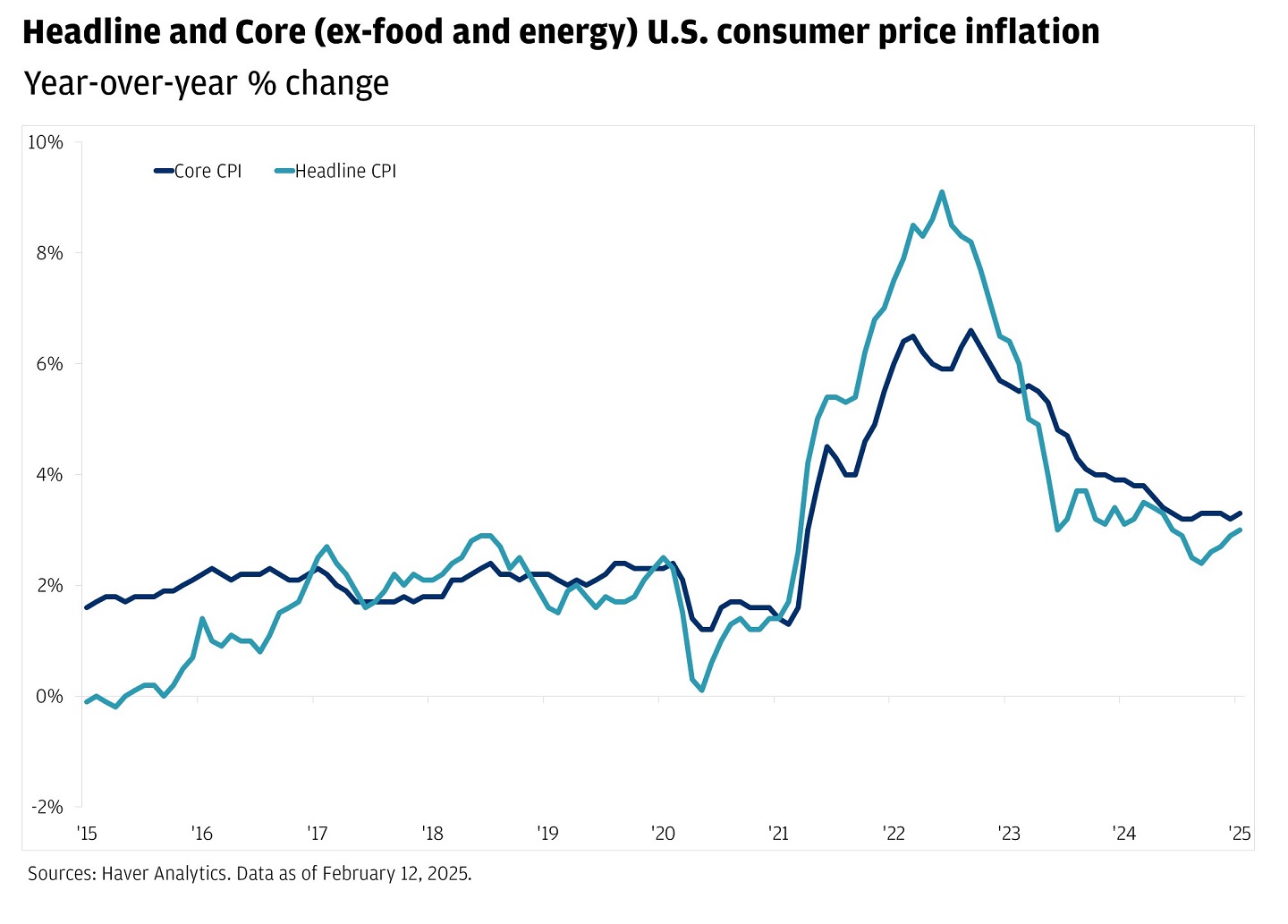

So, you're looking at your grocery receipt or checking out the price of gas and wondering if the numbers on the news actually match your reality. Honestly, they rarely do. But if we’re talking hard data, the current inflation rate in the us is sitting at 2.7% as of the latest Bureau of Labor Statistics (BLS) report released in January 2026.

That number represents the 12-month change ending in December 2025. It’s a bit of a mixed bag. On one hand, it’s a lot lower than those scary 9% peaks we saw a few years back. On the other hand, it’s still parked above the Federal Reserve’s "magic number" of 2.0%.

Basically, prices aren't falling; they're just climbing a smaller hill than they used to.

Breaking Down the 2.7% Headline

When the government says the current inflation rate in the us is 2.7%, they’re looking at a giant bucket of stuff called the Consumer Price Index (CPI). But you’ve probably noticed that eggs and car insurance don't move in sync.

Take a look at how different categories are behaving right now:

👉 See also: Modern Office Furniture Design: What Most People Get Wrong About Productivity

- Food prices are actually outpacing the general rate, up 3.1% over the last year. If it feels like your lunch bill is higher, it’s because "food away from home" (restaurants and takeout) jumped 4.1%.

- Shelter costs remain the biggest headache. Rent and housing-related expenses rose 3.2%. Since housing makes up about a third of the typical household's budget, this is the main reason why the "official" rate still feels so high to most people.

- Energy is the weird outlier. It increased 2.3% overall, but that hides a lot of drama. Gasoline prices actually dropped 3.4% over the year, but your electricity bill likely went the other way, rising by 6.7%.

It’s kind of a "choose your own adventure" situation for your wallet. If you drive a lot but eat at home, you’re feeling okay. If you’re a renter who loves dining out, you're probably wondering why everyone is saying inflation is "cooling."

Why the Number Isn't Moving Much

There was a lot of hope that we’d be back to 2% by now. It hasn't happened. Economists like Jan Hatzius at Goldman Sachs and experts at J.P. Morgan have pointed to a few "sticky" reasons.

First, there’s the "catch-up" effect. Some businesses waited a long time to raise prices when their own costs went up in 2023 and 2024. Now, they’re finally pulling the trigger. Then you have the labor market. Even though hiring has cooled off, wages are still growing around 3.5% to 3.9%. That's great for workers, but it gives companies a reason to keep their prices slightly elevated to cover those payrolls.

We also can't ignore the policy shifts. The implementation of various tariffs throughout 2025 acted like a small, persistent tax on goods. Most analysts believe these tariffs added about 0.5 percentage points to the headline number. Without them, we might be looking at a current inflation rate in the us much closer to the Fed’s goal.

✨ Don't miss: US Stock Futures Now: Why the Market is Ignoring the Noise

The Core vs. Headline Debate

You’ll often hear pundits talk about "Core CPI." This version strips out food and energy because those prices jump around like crazy based on a storm in the Gulf or a war halfway across the world.

Right now, Core CPI is at 2.6%.

The fact that the core rate is almost identical to the headline rate tells us that inflation is broad. It’s not just a spike in oil or a bad harvest; it’s baked into the services we use every day, from medical care (up 3.5%) to car repairs (up 5.4%).

What This Means for Your Bank Account

The Federal Reserve is in a tough spot. They want to cut interest rates to help the housing market and keep the economy growing, but they can't do it too fast if inflation stays stuck near 3%.

🔗 Read more: TCPA Shadow Creek Ranch: What Homeowners and Marketers Keep Missing

Last December, they nudged the interest rate down to a range of 3.5%–3.75%. But don't expect a flurry of cuts in early 2026. The consensus among big banks is that the Fed will likely stay on hold until the summer. They need to see those shelter costs finally trend downward before they feel safe.

If you're waiting for mortgage rates to tumble back to 3% or 4%, you might be waiting a long time. The "new normal" for a while seems to be this "higher for longer" environment.

Actionable Steps for 2026

Since we know the current inflation rate in the us is being driven by specific categories, you can actually hedge against it.

- Audit your "Services" spending: Insurance and maintenance are seeing the highest jumps. It’s a good time to shop around for new car insurance or homeowners' policies.

- Lock in fixed costs: If you're on a month-to-month lease, try to negotiate a longer-term contract now while some landlords are seeing vacancies rise.

- High-yield is still your friend: With interest rates still relatively high, don't leave your "emergency fund" in a standard savings account making 0.01%. You can still find accounts paying well over 4%, which beats the 2.7% inflation rate and actually grows your purchasing power.

The bottom line? We aren't in a crisis anymore, but the era of "cheap everything" hasn't returned yet. Keeping an eye on the monthly BLS releases (the next one is due February 11) will help you see if we're finally breaking toward that 2% target or if we're just stuck in the high twos for the foreseeable future.