If you just looked at the headlines this week, you’d think we finally beat the monster. The Bureau of Labor Statistics just dropped the latest numbers, and they show the current inflation rate in the US sitting at 2.7% for the 12 months ending December 2025.

That sounds great, right? It’s a far cry from that terrifying 9.1% peak we saw back in 2022. But honestly, if you’re still feeling a localized heart attack every time you check out at the grocery store, you aren't imagining things.

There is a massive gap between "inflation is slowing down" and "prices are going down." Inflation is just the speed at which prices rise. Even at 2.7%, the car is still moving forward; it’s just not flooring it anymore. The reality on the ground is that the "sticker shock" from the last three years has basically baked itself into our daily lives.

📖 Related: Finding the Right Bank of America in Gulf Breeze: What to Know Before You Drive

Why that 2.7% headline feels like a lie

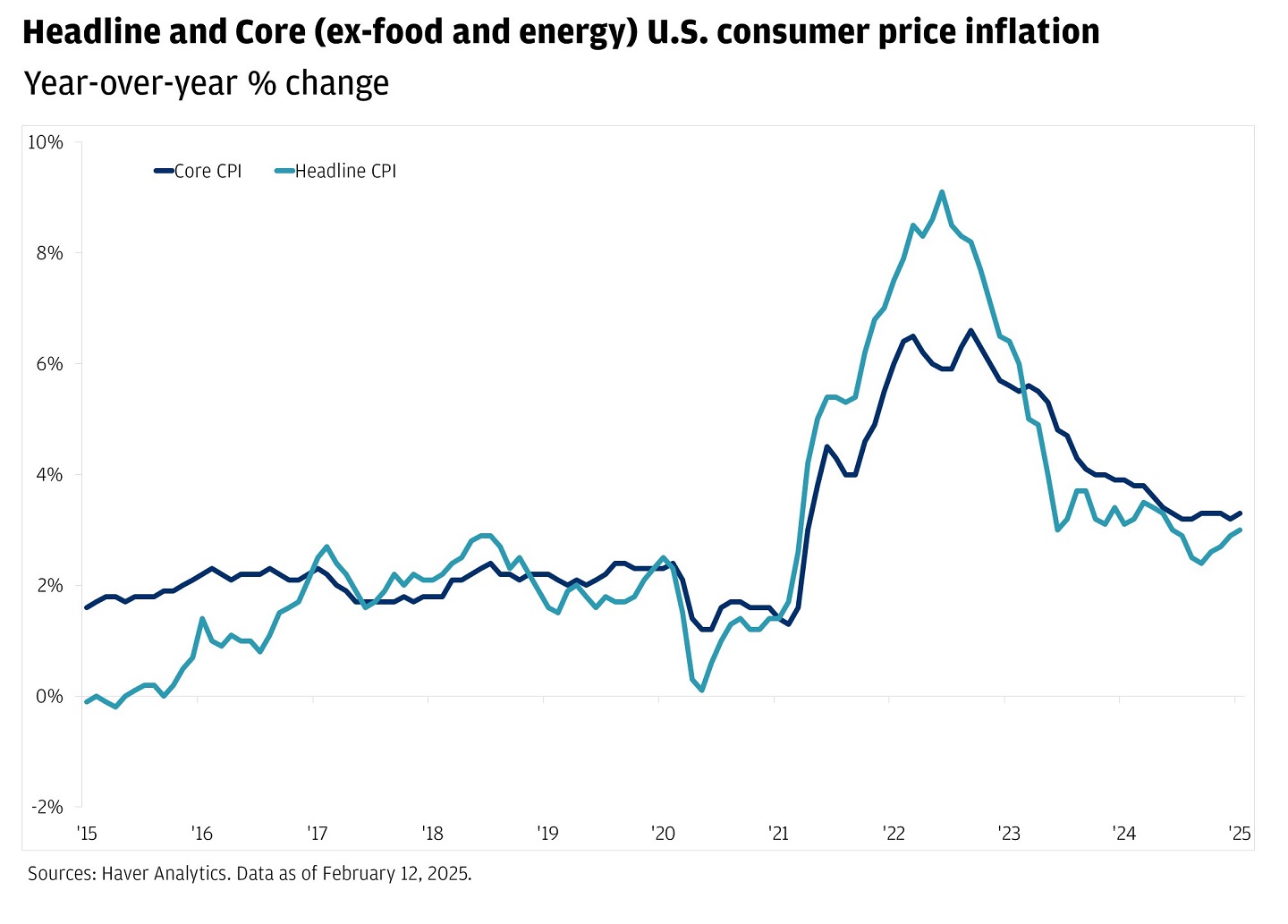

When the government talks about the current inflation rate in the US, they use the Consumer Price Index (CPI). It’s basically a giant shopping basket of stuff—everything from haircuts to heating oil.

In December, the CPI rose 0.3% on a monthly basis. That doesn't sound like much until you look at what actually moved. Shelter costs—basically your rent or mortgage—jumped 0.4% in a single month. That’s the heavy hitter. It makes up about a third of the entire index, and it’s been incredibly stubborn.

Then you’ve got food. Food prices rose 0.7% in December alone. If you feel like your eggs and cereal are still getting more expensive, it's because they are. Specifically, nonalcoholic beverages jumped 5.1% over the last year.

The Core vs. Headline debate

Economists love to talk about "Core CPI." This version ignores food and energy because those prices jump around like crazy. Currently, Core CPI is sitting at 2.6%.

The logic is that if you remove the "noise" of a sudden oil spike or a bad harvest, you see the true underlying trend of the economy. But you can't eat "Core CPI." You can’t drive your car on it. For most of us, the headline number—the one that includes the 2.3% rise in energy costs—is the only one that actually matters for the bank account.

The weird 2026 economic landscape

We’re in a strange spot right now. Usually, when inflation stays above the Federal Reserve’s 2% target, they keep interest rates high to cool things down. But 2025 was a chaotic year. We had a government shutdown that lasted from October to mid-November, which actually messed up the data collection. We’re only now getting a clear look at the damage.

There's also the "tariff effect." Goldman Sachs recently pointed out that new tariffs likely added about 0.5 percentage points to the inflation we’re seeing right now. Without those one-time policy shocks, we might actually be closer to that 2% goal.

What’s actually getting cheaper?

It isn't all bad news. Some things are actually seeing "deflation"—meaning the price is lower today than it was a year ago.

- Dairy products fell 0.9% over the last 12 months.

- Gasoline is actually down 3.4% compared to this time last year.

- Used cars are finally normalizing, though insurance for those cars is still a nightmare.

Speaking of nightmares, let's talk about services. While the price of "stuff" (commodities) is only up 1.4%, the price of "doing things" (services) is up 3.0%. This is the "sticky" part of inflation. Haircuts, car repairs, and medical visits are getting more expensive because labor costs are staying high.

What to expect for the rest of 2026

Most experts, including those at J.P. Morgan and Vanguard, think we’re going to stay in this "low-grade fever" state for a while. They’re forecasting the current inflation rate in the US to drift down toward 2.4% by the end of the year, but it’s going to be a bumpy ride.

We’ve got a few "X-factors" that could blow up these predictions:

- The Dollar: If the trade-weighted dollar stays weak, imports get more expensive.

- The Labor Market: We’ve moved into a "low-hire, low-fire" phase. If companies can't find workers, they raise wages, and then they raise prices to cover those wages.

- Fiscal Stimulus: There’s talk of more tax breaks or government spending in late 2026. That’s like throwing gasoline on a dying fire.

Real-world survival steps

Since we can't wait for the Fed to fix everything, here is how to actually handle the current inflation rate in the US without losing your mind.

Audit your "Service Creep"

Since services are the main thing driving inflation right now, look at your subscriptions and insurance. Auto insurance premiums actually saw some declines recently after a massive spike. If you haven't shopped your rate in six months, you’re probably overpaying.

👉 See also: Finding a Letter of Intent Sample That Doesn't Look Like Every Other Template

Watch the "Food Away From Home" index

The cost of eating out rose 4.1% this year, while groceries ("food at home") only rose 2.4%. The gap is widening. Basically, you’re paying a massive premium for the service and labor of the restaurant, not just the food. Eating in isn't just a suggestion anymore; it’s a mathematical necessity if you want to beat the CPI.

Hedge with high-yields

The silver lining of the Fed keeping rates high to fight inflation is that savings accounts actually pay something now. If your money is sitting in a traditional big-bank savings account earning 0.01%, you are effectively losing 2.7% of your wealth every year. Move it to a high-yield account or a money market fund that tracks closer to 4% or 5%.

The big takeaway

The current inflation rate in the US is cooling, but the "cost of living" is still a mountain. We've moved from a crisis of "prices are exploding" to a grind of "everything is just expensive." Staying ahead of it requires shifting your focus from the headline numbers to the specific categories—like shelter and services—where the heat is still on.

Keep an eye on the next BLS release on February 11, 2026. That will be the first "clean" data set of the year and will tell us if this 2.7% is a permanent plateau or just a pit stop on the way back to normal.