Money moves fast. One minute you’re looking at a flight from Manila to Los Angeles, and the next, you’re staring at a checkout screen wondering why the math doesn't add up. If you've got exactly 9500 PHP to USD in your head as a budget, you might think you have a solid handle on the situation. You don't.

Rates flicker.

By the time you finish reading this sentence, the mid-market rate for the Philippine Peso has probably ticked up or down by a fraction of a cent. While that sounds like "small potatoes," it’s the difference between getting a fair deal and getting fleeced by a hidden "spread" at a kiosk or a digital wallet.

The Math Behind 9500 PHP to USD Today

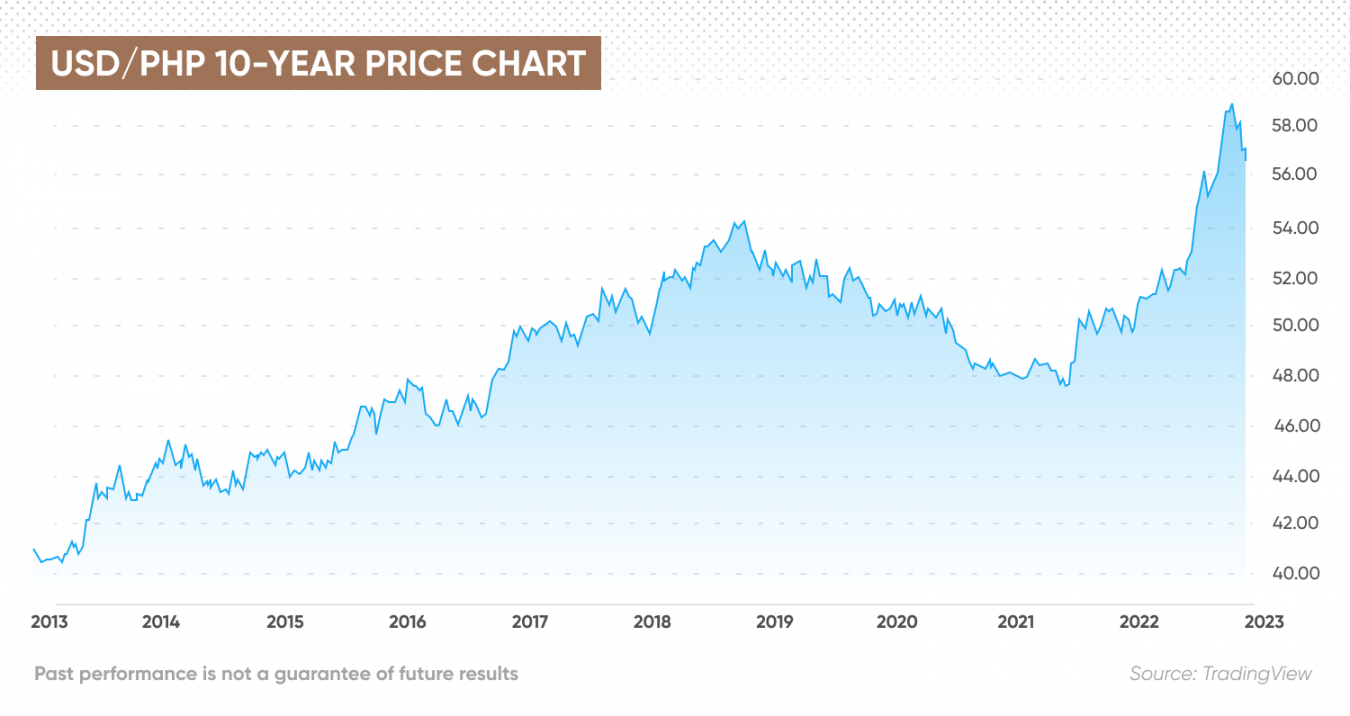

Right now, the exchange rate is hovering in a specific zone. To get the "real" value of 9500 Philippine Pesos in US Dollars, you have to look at the Bangko Sentral ng Pilipinas (BSP) benchmarks and the global Forex market. Generally, the Peso has been sitting between 55 and 58 per dollar over the last year.

💡 You might also like: Social Security Admin Phone Numbers: How to Actually Reach a Human

If we take a hypothetical rate of 56.50 PHP per 1 USD, your 9500 PHP comes out to roughly $168.14.

But here is the kicker: you will almost never see that $168.14 in your bank account. Why? Because the "mid-market rate" is the price banks use to trade with each other, not the price they give to humans. You're likely looking at a "retail rate."

When you go through a service like GCash, Maya, or a traditional bank like BDO or BPI, they shave a bit off the top. Sometimes it’s a flat fee. More often, it’s an exchange rate markup. If the market says 56.50, they might sell it to you at 58.00. That difference is how they keep the lights on. It’s sneaky. It’s annoying. It’s also just how the world works.

Why the Peso Fluctates So Much

The Philippine Peso isn't a static entity. It breathes. It’s heavily influenced by the Federal Reserve in the United States. When the Fed raises interest rates, the Dollar gets stronger, and the Peso usually takes a hit.

Then you have remittances.

The Philippines is one of the world's largest recipients of money sent home from overseas. During the holidays—specifically late November through December—there is a massive influx of Dollars being converted into Pesos. This surge in supply and demand can cause temporary swings that make your 9500 PHP to USD conversion look very different on Tuesday than it did on Sunday.

Where Most People Lose Money in the Conversion

Most people just click "accept."

They see the conversion on PayPal or a credit card statement and assume it's the best they can get. It isn't. PayPal, for instance, is notorious for having some of the widest spreads in the industry. If you’re converting 9500 PHP on their platform, you might lose 3% to 4% just in the conversion margin. That’s essentially a "convenience tax" that adds up if you're doing this frequently.

Then there’s the airport.

Honestly, if you are changing money at NAIA or any international airport, you are basically burning cash. Those physical booths have high overhead. They pay for the space, the staff, and the security. They pass those costs to you. You might walk away with $155 instead of the $168 you expected. That’s a couple of decent meals in Manila gone just because of the location of the transaction.

Digital Wallets vs. Traditional Banks

In the Philippines, the battle is between the old guard and the new apps. GCash has become the de facto currency for many, but their international conversion for 9500 PHP to USD depends heavily on the card network (Visa or Mastercard) rather than their own internal rates.

- Wise (formerly TransferWise): They use the real mid-market rate. You pay a small, transparent fee. It’s usually the cheapest way to move money if you have a US bank account to receive it.

- Western Union: Good for cash pickups, but their rates are "kinda" mid-tier. You won't get the best rate, but you won't get the worst.

- Crypto P2P: Some people use USDT (Tether) to bridge the gap. You buy 9500 PHP worth of USDT on a platform like Binance, then sell it for USD. It’s fast. It’s also risky if you don't know what you're doing with wallet addresses.

The "Hidden" Costs You Forgot to Calculate

When calculating 9500 PHP to USD, don't forget the receiving end.

If you send that money to a US bank, the receiving bank might charge an "incoming wire fee." These can range from $15 to $30. If you’re only sending $168, a $25 fee is a catastrophe. That’s nearly 15% of your total value gone.

If you're using a credit card for a purchase priced in USD, check your "Foreign Transaction Fee." Most basic cards charge 3%. Some premium travel cards charge 0%. If you have a card with a 3% fee, your 9500 PHP purchase suddenly costs you 9785 PHP. It’s a slow bleed.

Real World Examples: What 9500 PHP Buys in the US

Let's put this into perspective. If you successfully convert your 9500 PHP and end up with roughly $165 in your pocket, what does that actually look like in the States?

It’s not as much as it used to be. Inflation has been a beast.

In a city like New York or San Francisco, $165 is a nice dinner for two with drinks and a tip. That’s it. In a smaller town in the Midwest, it might cover a week's worth of groceries for a small family if you’re shopping at Aldi and skipping the expensive cuts of meat.

If you're a gamer, that 9500 PHP is roughly two-and-a-half AAA titles at the current $70 price point. Or, if you’re looking at tech, it’s about the price of a mid-range pair of noise-canceling headphones or a very entry-level Android tablet.

The Psychological Gap

There is a weird psychological thing that happens when you convert Pesos to Dollars. 9500 sounds like a lot of money. It’s nearly a month’s salary for some entry-level roles in the provinces of the Philippines. But when it turns into $165, it feels smaller. This "value perception gap" is why many travelers overspend. They think in the currency of the country they are in, but their bank account is still thinking in Pesos.

Actionable Steps for the Best Conversion

Don't just wing it.

If you need to move 9500 PHP to USD, start by checking the Google Finance rate just to have a baseline. That is your "north star." If any service is offering you significantly less than that, keep walking.

Second, use a multi-currency account if you do this often. Services like Wise or Revolut allow you to hold "jars" of different currencies. You can convert when the rate is favorable—say, when the Peso strengthens for a day or two—and keep it in USD until you need to spend it.

Third, avoid the "Dynamic Currency Conversion" (DCC) trap at ATMs or credit card terminals. If a machine asks, "Would you like to be charged in PHP or USD?" always choose the local currency of the machine. If you are in the US, choose USD. If you are in the Philippines, choose PHP. If you let the machine do the conversion, it will use its own "house rate," which is almost always a total rip-off.

Finally, keep an eye on the clock. The Forex market is closed on weekends. If you try to convert 9500 PHP to USD on a Saturday, many apps will add a "weekend markup" to protect themselves against the market opening at a different price on Monday morning. Convert during mid-week business hours for the tightest spreads.

The goal isn't just to convert the money. It's to keep as much of it as possible. Every percentage point you save is a few more Dollars in your pocket, and in this economy, every cent counts.

Next Steps for You:

- Check the Current Mid-Market Rate: Use a tool like XE.com or Google Finance to see the live 9500 PHP to USD rate right now.

- Audit Your Apps: Open your banking app and look at their "Sell" rate for USD. Compare that to the mid-market rate to see exactly how much they are charging you in "hidden" fees.

- Choose Your Method: Use Wise for the lowest fees on transfers, or a zero-foreign-transaction-fee credit card for direct purchases to avoid the 3% surcharge.