You’ve probably seen the blue octagon everywhere. It’s on every corner in Manhattan and scattered across suburban strip malls from coast to coast. Chase is a behemoth. But when it comes to the chase 3 month cd rate, things get a little weird. People often assume that a bank this big would offer the best rates. Honestly? That is rarely the case.

Banking with a giant like JPMorgan Chase is usually about convenience, not squeezing every penny of interest out of your savings. If you walk into a branch today, the person behind the desk might pitch you on their "featured" terms. But if you aren't careful, you might end up with a rate so low it's basically a rounding error.

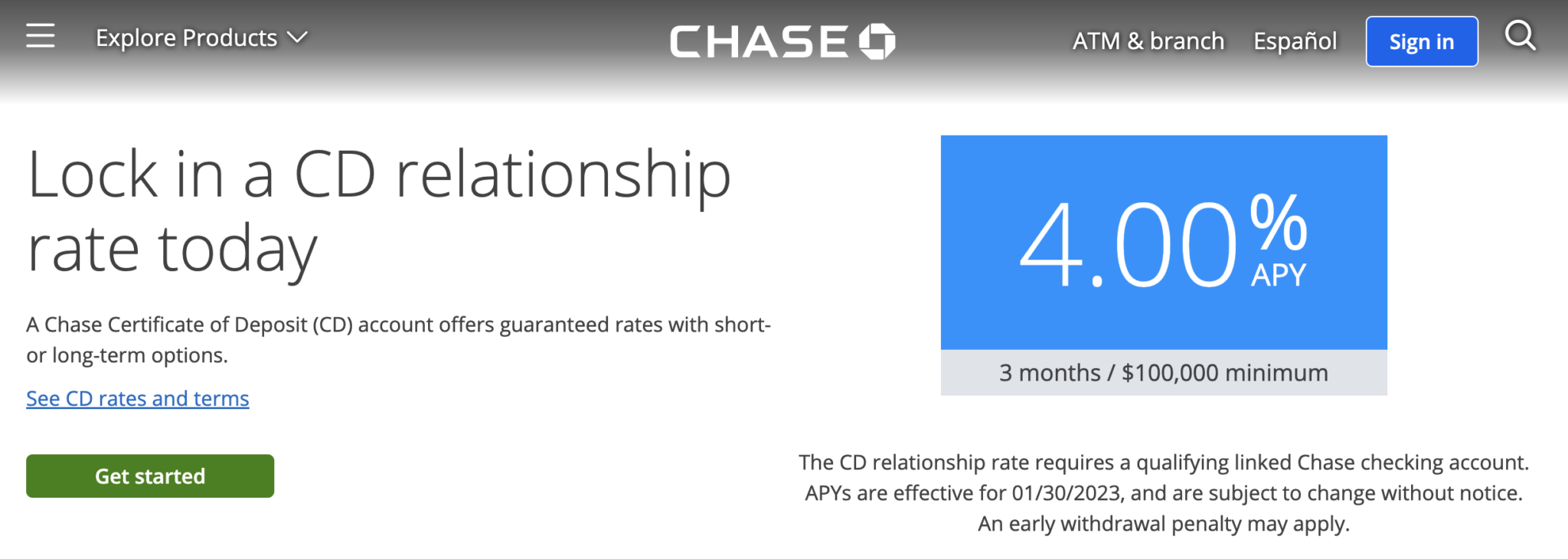

The Truth About the Chase 3 Month CD Rate

Here is the deal. Chase has two very different rate tiers. There is the "Standard" rate and the "Relationship" rate.

If you just have a random thousand dollars and you want to open a 3-month CD without having a checking account there, you're looking at a standard rate of 0.01% APY. No, that isn't a typo. It is basically zero. You would earn more money finding a stray nickel on the sidewalk.

However, if you link a qualifying Chase checking account, you jump into the "Relationship" tier. For January 2026, the chase 3 month cd rate for relationship customers is significantly better, often hovering around 4.25% APY.

That sounds great, right? It is. But there is a catch.

Why the Relationship Matters

To get that 4.25%, you can't just be a stranger. You need to have an active checking account. Chase uses these higher CD rates as a "hook" to keep you in their ecosystem. They want your direct deposit. They want you using their app.

- Standard Rate: 0.01% APY (Basically a piggy bank).

- Relationship Rate: Up to 4.25% APY (Actually competitive).

- Minimum Deposit: $1,000.

If you have $100,000 or more, sometimes that rate nudges up slightly, but for most people, the jump from standard to relationship is the only one that matters.

Is 3 Months Actually Long Enough?

Short-term CDs are having a moment. With the Federal Reserve having cut rates three times in 2025, everyone is nervous about where yields are going in 2026. A 3-month term is sort of the "sweet spot" for people who are indecisive.

It's a "park it and wait" strategy.

Maybe you’re waiting to buy a house. Or perhaps you’re just terrified the market is going to tank and you want your cash safe. A 3-month CD gives you a guaranteed return without locking you up for a year. But remember, APY stands for Annual Percentage Yield.

If you put $10,000 into a 3-month CD at 4.25%, you aren't getting $425 at the end of 90 days. You’re getting about $106. You only get the full 4.25% if you keep the money in for a full year. It’s a common mistake. People see the big number and forget to do the math.

The Penalty Trap

Let's talk about the "oh no" scenario. You put your money in, and two months later, your car's transmission explodes.

If you break a Chase CD with a term of less than 6 months, the penalty is 90 days of interest.

💡 You might also like: Rupee to Turkish Lira: Why Your Money Doesn't Go Where It Used To

Think about that. On a 3-month (90-day) CD, the penalty is 90 days of interest. If you pull the money out early, you basically forfeit all the interest you earned. You’ll get your original deposit back, but the bank keeps the profit. It’s a steep price for a little bit of liquidity.

How Chase Compares to the "Online" Guys

If you’re chasing the absolute highest yield, Chase usually loses to online-only banks. Banks like OMB Bank or Ivy Bank are often pushing 3-month rates above 4.11% or even 4.50% without requiring a "relationship" account.

Why? Because they don't have to pay for thousands of physical buildings and ATMs.

But there’s a nuance here. If you already do your banking at Chase, moving $20,000 to a random online bank just to earn an extra 0.20% might not be worth the headache. Opening a new account, waiting for the ACH transfer to clear, and managing another login... it's a lot of work for a few extra bucks.

That’s what Chase is counting on. They know "good enough" is usually enough to keep you from leaving.

What Most People Get Wrong About CD Ladders

You've probably heard of "laddering." It's the strategy where you split your money into different CDs so they mature at different times.

A 3-month CD is the perfect bottom rung for a ladder.

💡 You might also like: Inside The Weather Channel Headquarters: Why It’s Not Just a TV Studio

If you have $40,000, you don't put it all in one 12-month CD. You put $10k in a 3-month, $10k in a 6-month, $10k in a 9-month, and $10k in a year. Every three months, you have cash becoming available. If rates go up, you reinvest at the higher rate. If you need the money, it's there.

The mistake people make is using Chase for the whole ladder. Since Chase's 6-month and 12-month rates are often lower than their 3-month "featured" rate, your ladder ends up looking more like a broken staircase.

Actionable Steps for Your Cash

If you are looking at the chase 3 month cd rate right now, don't just click "open" in the app.

First, check your account type. If you don't see the word "Relationship" next to the rate, stop. You are about to sign up for 0.01%, which is a waste of time. Talk to a banker or check your online portal to see if you can link your checking account to unlock the better tier.

Second, look at the "Featured Terms." Chase usually picks one or two specific months—like 3 months or 7 months—and gives them a massive boost while leaving the other terms at nearly zero. If the 3-month is the featured term, take it. If the 4-month is the featured term, that extra 30 days might double your interest.

Finally, mark your calendar. Chase CDs have a 10-day grace period. When that 3-month term ends, you have exactly ten days to move your money. If you miss it, they will automatically roll you into a new CD at the current rate—which might be much lower than what you started with.

✨ Don't miss: Gold and Bags Pawn Shop: How to Actually Get Paid What Your Luxury is Worth

Don't let your money go on autopilot in a big bank. They thrive on customers who forget to check the fine print.

Check the current "Relationship" offer on the Chase website. Compare it against a high-yield savings account (HYSA). If the CD rate isn't at least 0.50% higher than a standard savings account, the lack of liquidity probably isn't worth it.

Decide if the convenience of having all your money in one app outweighs the extra $20 you'd make at an online bank. If it does, lock in that featured 3-month rate, but set a reminder for the maturity date the second you open the account.