Walk into any Chase or BMO branch on Michigan Avenue and you’ll see the same glossy posters. They promise "competitive" returns. But honestly? If you’re just taking whatever rate your neighborhood branch manager offers, you’re basically leaving a year’s worth of high-end steak dinners on the table.

Chicago is a weird banking town. We have a massive mix of global giants and tiny, hyper-local credit unions that most people have never heard of. Right now, in January 2026, the gap between a "standard" rate and a "special" rate is huge. It’s the difference between earning 0.05% and over 4.00%.

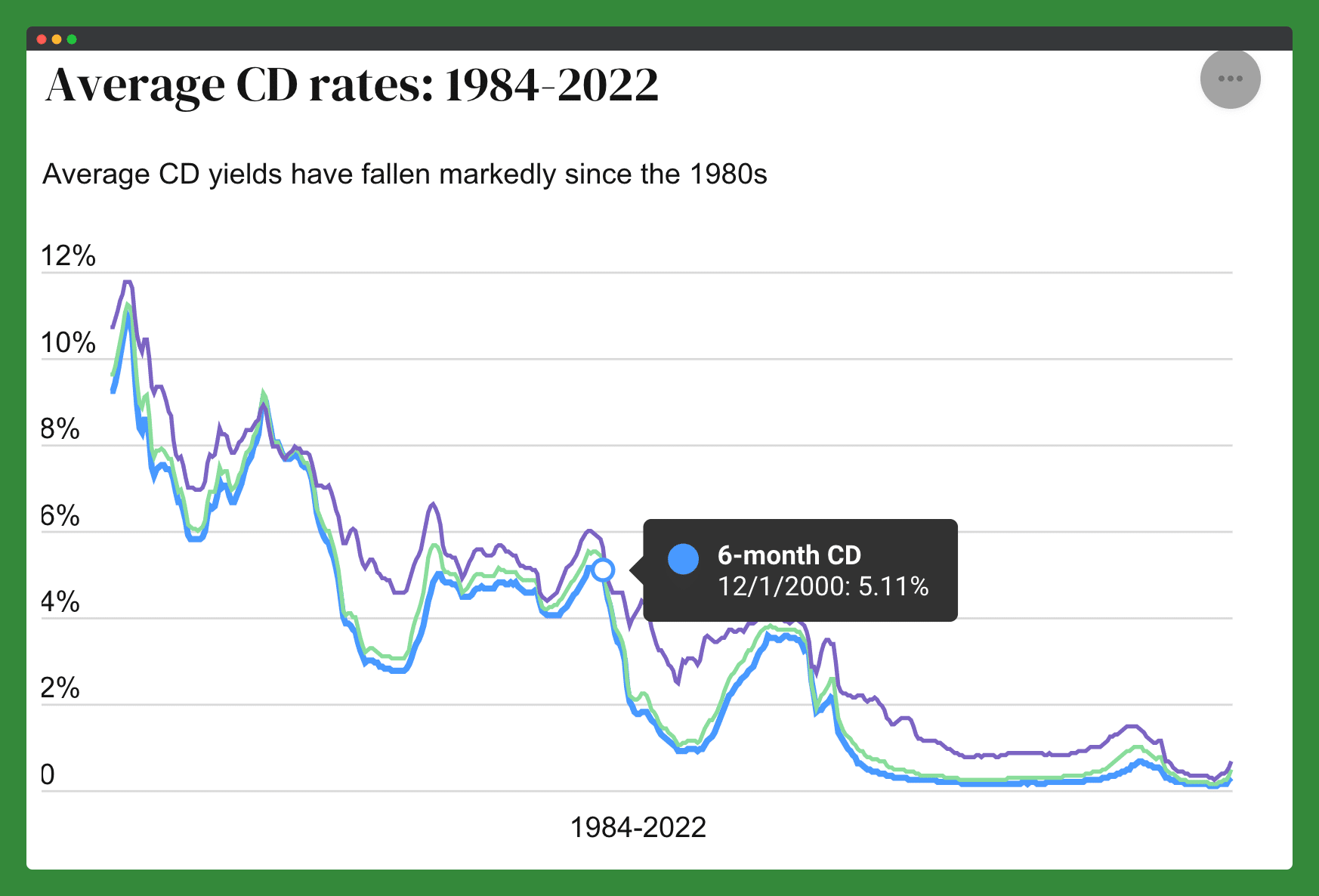

Inflation has cooled, but it’s still nibbling at your savings. If your money is sitting in a basic savings account at one of the "Big Four," you’re losing purchasing power every single day.

The Real Truth About CD Rates Chicago IL

You’ve probably noticed that the big banks aren't exactly begging for your deposits lately. They have plenty of cash. Because of that, their CD rates Chicago IL are often underwhelming—think 0.01% to 2.00% unless you're moving "new money" in six-figure chunks.

The real action is happening with local institutions like Byline Bank, Wintrust, and a handful of credit unions. For instance, as of mid-January 2026, Byline Bank is dangling a 5-month promo CD at 3.90% APY. That’s a very specific, odd-term length. Banks do this on purpose. They want to attract cash for short bursts to balance their books without committing to high payouts for years.

🔗 Read more: Chase Early Direct Deposit: Why You Might (Or Might Not) See Your Paycheck Early

Wintrust Bank is currently playing a similar game. Their 7-month special is sitting around 3.75% APY. Is it the highest in the country? No. But if you want a physical branch in Lakeview or Lincoln Park where you can actually talk to a human, it’s a solid local play.

Why Credit Unions Are Winning the Rate War

If you aren't looking at credit unions, you're missing the best CD rates Chicago IL has to offer. Period.

Take Alliant Credit Union, which is headquartered right here in Chicago (near O'Hare). They are consistently thumping the big banks. Currently, you can snag a 6-month CD at 4.10% APY with a $1,000 minimum.

Then there’s BCU (Baxter Credit Union). They’ve been running a 5-month special at 4.05% APY. These aren't just marginal gains; we're talking about doubling or tripling what a standard commercial bank offers.

- Vibrant Credit Union: They have an Illinois presence and recently offered a 6-month special at 4.15% APY.

- Chicago Firefighters Credit Union: Often features "neighborhood specials" that aren't advertised nationally but can hit 4.50% or higher for 12-month terms.

The "catch" with credit unions is usually membership. But in 2026, those old "you must work for this specific company" rules are mostly gone. Most let you join just by living in the Chicagoland area or making a tiny $5 donation to a specific non-profit. It’s a loophole worth jumping through.

Don't Fall for the "Longer is Better" Trap

Normally, you'd expect a 5-year CD to pay more than a 1-year CD. That’s "normal" economics. But right now? The yield curve is still acting a bit funky.

You’ll see 12-month CD rates Chicago IL that are significantly higher than 60-month rates. For example, Fifth Third Bank has been offering promotional 4-month and 8-month terms around 3.00% APY, while their long-term 84-month rates are a dismal 0.01% for standard accounts.

Locking your money up for five years at a lower rate than a six-month term makes zero sense. Unless you’re convinced that interest rates are going to absolutely crater by 2027, stick to the "sweet spot" terms: 5, 7, 9, or 13 months. These are almost always where the "special" pricing lives.

The "New Money" Hurdle

Here is something the brochures won't tell you: the best rates are almost always for "New Money."

If you already have $50,000 sitting in a Wintrust savings account and you want to move it into a high-rate CD, they might say no. Or rather, they’ll give you the "standard" rate instead of the "promo" rate.

Banks use CDs as a customer acquisition tool. They want fresh cash from outside their ecosystem. If you want the best CD rates Chicago IL offers, you might need to play "bank hopper." Move your maturing funds from Chase to Byline, then a year later, move it to Old National. It’s a pain, but it’s how you maximize yield.

Local Banks vs. Digital Disrupters

You don't have to stay local. Online giants like Marcus by Goldman Sachs or Discover Bank (which has a huge footprint in Riverwoods) are hovering around the 4.00% mark for 12-month terms.

The advantage of a place like Old National Bank—which has a 5-month CD at 3.75%—is the ability to walk in and resolve issues. If a digital bank freezes your account because of a "suspicious" transfer, you're stuck on a 1-800 number. At a Chicago branch, you can stand in the lobby until it’s fixed. For many, that peace of mind is worth a 0.20% lower rate.

👉 See also: Can You Copyright a Word? The Truth About Protecting Single Words

Checking the Fine Print

Early withdrawal penalties in Chicago are getting aggressive. Back in the day, you’d lose three months of interest if you broke a CD early. Now, some banks are charging "all interest earned" or even a percentage of the principal.

Old Second National Bank has some decent 6-month specials at 3.25%, but always ask about the "break fee." If you think you might need that cash for a sudden condo assessment or a car repair, a CD is the wrong move. Look at a Money Market account instead. Old National has a "Market Monitor" account at 3.25% APY for balances over $20,000. It’s nearly the same rate as a CD but without the "lock-in" handcuffs.

Tactical Steps to Take Now

Don't just stare at the numbers. Execution matters.

- Check your current "dusty" accounts. If you have money in a savings account earning less than 3%, you're losing.

- Scan the "odd terms." Look for the 7-month, 11-month, or 13-month specials. These are the marketing loss-leaders for banks like Wintrust and Byline.

- Join a Credit Union. Even if you don't use them for your daily checking, having an account at Alliant or BCU gives you access to their rate spikes.

- Ladder your cash. Instead of putting $50,000 into one 12-month CD, put $10,000 into five different CDs with staggered maturity dates. This gives you "liquidity events" every few months.

- Ask for a "Retention Rate." If you have a large balance at a bank like Fifth Third, tell them you’re thinking of moving to a competitor for a better rate. Sometimes—not always—they can pull a "private" rate out of the drawer to keep you.

The Chicago banking market is competitive enough that you should never settle for the national average. If a bank isn't giving you at least 3.50% right now for a short-term commitment, they aren't serious about your business.