You open your paycheck. You see the gross amount and think, "Nice." Then you see the net amount and think, "Wait, what?" If you live in the Golden State, that gap is usually wider than a Hollywood red carpet. Honestly, the California tax rate table is notorious for being one of the most aggressive in the country, but most people don't actually understand how the math works until they're staring at a surprise bill in April.

California uses a progressive system. This basically means the more you make, the more the Franchise Tax Board (FTB) wants from you. It isn't a flat fee. It’s a ladder.

How the California Tax Rate Table Actually Functions

Most folks assume that if they land in the 9.3% bracket, the state just takes 9.3% of everything. That’s wrong. It's a common misconception that keeps people from taking raises because they "don't want to move into a higher bracket." Relax. That’s not how it works.

California has ten different tax brackets. Yes, ten. They range from 1% all the way up to 13.3% if you’re pulling in seven figures. You pay the lowest rate on your first chunk of income, and then only the money above that threshold gets hit with the next higher rate. It’s like a series of buckets. Once the 1% bucket is full, the rest of your money spills into the 2% bucket, and so on.

For the 2024 and 2025 tax years, these thresholds shift slightly because of inflation adjustments. The FTB isn't totally heartless; they do try to account for the fact that a dollar doesn't buy as much sourdough in San Francisco as it used to.

The Low End: 1% to 4%

If you're a single filer making under $10,000, you're mostly in the 1% zone. It’s almost negligible. As you climb toward $25,000 or $30,000, you start hitting the 2% and 4% rungs. For many young professionals or those in entry-level service roles, this is where they live. It’s manageable. You might feel the pinch, but it isn't soul-crushing yet.

The "Middle Class" Trap: 6% to 9.3%

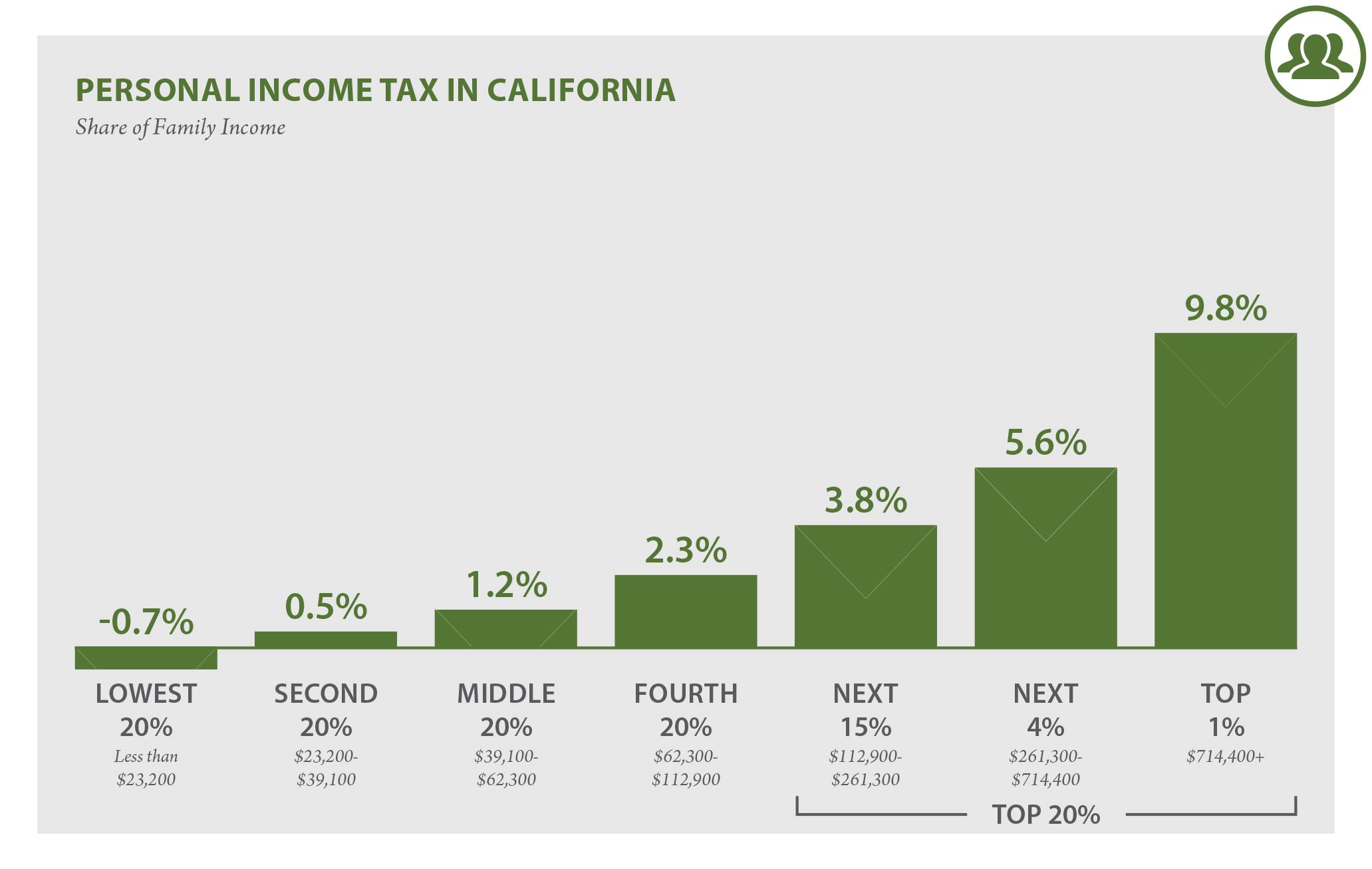

This is where it gets spicy. Once a single filer clears roughly $37,000, they jump to 6%. If you’re making between $68,000 and $341,000 (a massive range, frankly), you’re likely looking at the 9.3% bracket for your top dollars.

Think about that.

💡 You might also like: New Zealand currency to AUD: Why the exchange rate is shifting in 2026

A nurse in Sacramento and a software engineer in San Jose might both be seeing nearly 10% of their "top" dollars go to the state, even though their lifestyles look completely different. This 9.3% bracket is the workhorse of the California tax rate table. It covers the vast majority of skilled workers in the state.

The Millionaire's Tax and the 13.3% Ceiling

You’ve probably heard people complain that California has the highest income tax in the U.S. They aren't lying. While the top nominal rate on the standard table is 12.3%, there is an extra kicker.

It’s called the Mental Health Services Act.

Passed back in 2004 (Proposition 63), this adds a 1% surcharge on taxable income in excess of $1 million. So, if you're a high-flyer, your top rate is actually 13.3%. This is why you see professional athletes or tech founders occasionally fleeing to Florida or Texas. When you’re dealing with $10 million in income, that 13.3% vs. 0% state tax difference is enough to buy a private island. Or at least a very nice boat to get to one.

Credits and Deductions: Your Only Defense

Standard deductions in California are actually pretty decent compared to some other states. For the 2024 tax year, a single filer gets a standard deduction of $5,363. Married couples filing jointly get $10,726.

It isn't a fortune.

However, California offers specific credits that can wipe out your liability dollar-for-dollar. The California Earned Income Tax Credit (CalEITC) is a big one for lower-income households. If you have kids, the Young Child Tax Credit can add another $1,100+ to your pocket.

📖 Related: How Much Do Chick fil A Operators Make: What Most People Get Wrong

Then there’s the Renter’s Credit. It’s tiny—$60 for singles, $120 for couples—and hasn't been significantly adjusted in ages, but hey, it’s a burrito and a drink on the state’s dime. Honestly, it feels a bit insulting given California rents, but you should still take it.

Why Your "Effective" Rate is Lower

Don't confuse your bracket with your effective rate. Your bracket is the highest rate you pay on your last dollar earned. Your effective rate is the actual percentage of your total income that goes to Sacramento.

Example: A single person earning $100,000 might be in the 9.3% bracket, but because of the lower brackets and the standard deduction, their actual state tax bill might be closer to $6,000. That’s an effective rate of 6%. Still a lot? Sure. But it sounds better than 9.3%.

The Hidden Complexity of Residency

One thing people get wrong about the California tax rate table is thinking they can just "live" in Nevada for three months a year and avoid it. The FTB is like the Terminator. They do not stop. They look at where your "center of gravity" is. Where is your car registered? Where do you vote? Where is your primary doctor? If you spend more than nine months in California, you are presumed to be a resident. Even if you spend less, if your "permanent" home is here, they want their cut of everything you earn globally.

Capital Gains Are Treated Like Income

Unlike the federal government, which gives you a break on long-term capital gains (assets held over a year), California doesn't care. If you sell stock or a house for a profit, that gain is dumped right into your regular income and taxed according to the standard California tax rate table.

This is a massive trap for people selling a home. If you have a huge gain on a property sale, you could easily find yourself pushed into that 12.3% or 13.3% bracket for that one year. Plan for it. Set that money aside immediately.

Real-World Math: A Single Filer's Journey

Let’s look at a hypothetical freelancer in Los Angeles making $85,000.

👉 See also: ROST Stock Price History: What Most People Get Wrong

- The first ~$10k is at 1%.

- The next ~$14k is at 2%.

- The next ~$14k is at 4%.

- The next ~$15k is at 6%.

- The rest is at 8% and 9.3%.

By the time the math is done, they’ll owe roughly $4,800 to $5,200 depending on deductions. This doesn't include federal taxes, Social Security, or Medicare. It’s no wonder people feel "California broke" even with a decent salary.

Actionable Steps for Tax Season

First, check your withholdings. If you always owe the state money in April, go to your payroll department and adjust your DE-4 form. The federal W-4 doesn't always translate perfectly to California's specific brackets.

Second, maximize your 401(k) or 403(b). California generally follows federal rules for these. Every dollar you put in your 401(k) is a dollar the state can't touch. If you're in the 9.3% bracket, contributing $20,000 to your retirement effectively "saves" you $1,860 in state taxes alone.

Third, keep track of your "Above-the-Line" deductions. Educator expenses, student loan interest, and certain moving expenses for military members can lower your California Adjusted Gross Income (AGI).

Fourth, look at the Middle Class Tax Refund or any one-time stimulus credits. California occasionally issues these when the state budget has a surplus. They usually don't happen every year, but when they do, you need to make sure you've filed a return to get them.

Finally, if you’re a business owner, look into the Pass-Through Entity (PTE) Elective Tax. It’s a way to work around the $10,000 federal cap on State and Local Tax (SALT) deductions. It’s complicated—you’ll want a CPA for this—but it can save you thousands of dollars by allowing your business to pay the state tax on your behalf.

California is beautiful, but the "sunshine tax" is real. Understanding where you sit on that table is the only way to keep your head above water and avoid a nasty surprise when you're trying to file your return. Focus on lowering your AGI and utilizing every credit available. Sacramento already has enough of your money; don't give them a tip.