Living in California is basically a dream until you look at your pay stub. It's beautiful here, sure. But the "sunshine tax" is a very real thing that hits your bank account every time the Franchise Tax Board (FTB) comes calling. Honestly, if you're trying to figure out what is the income tax rate in california, you've probably realized it isn't just one number. It’s a ladder. A long, steep, sometimes confusing ladder.

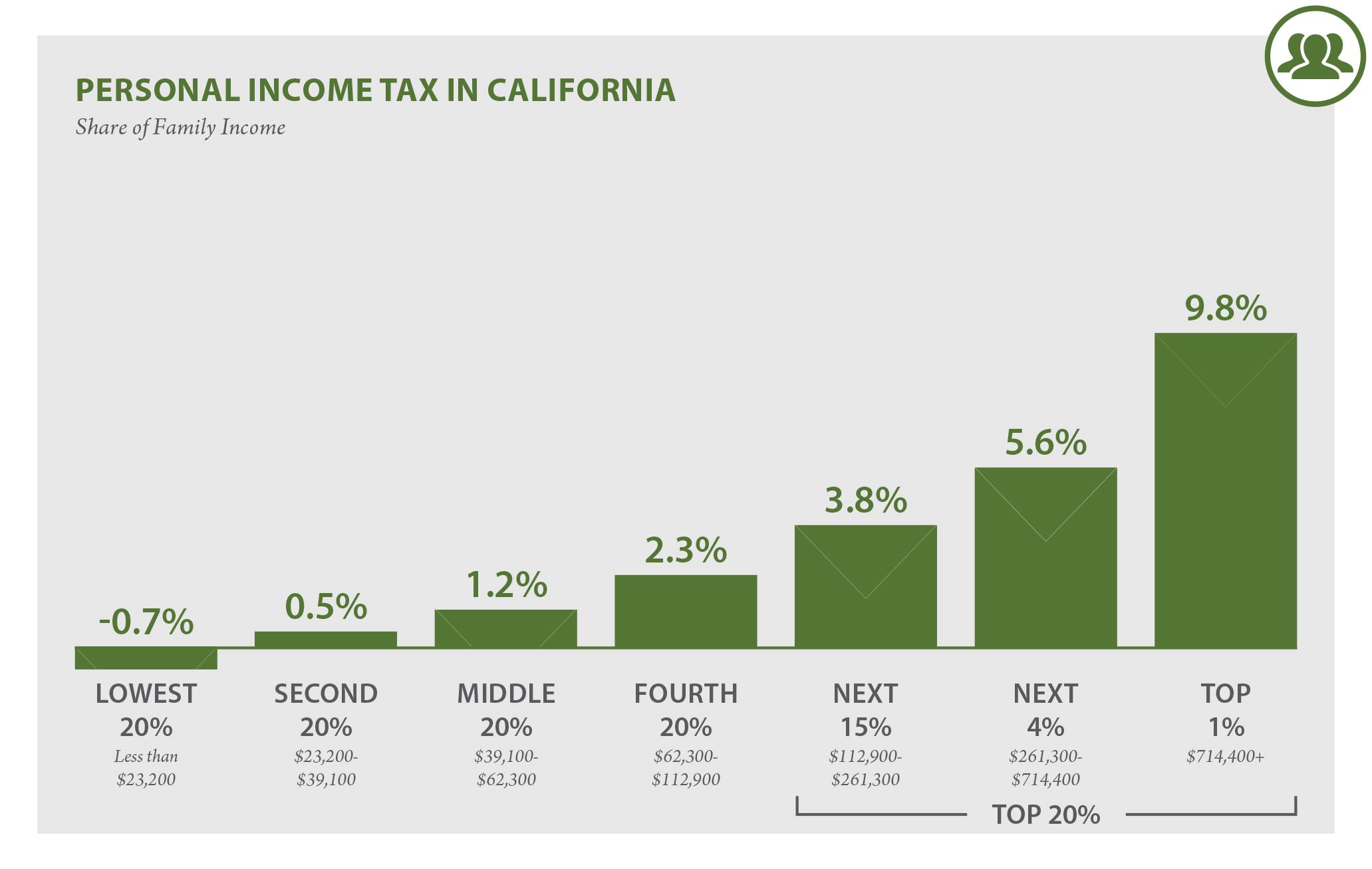

California uses a progressive tax system. This means as you earn more, the state takes a bigger bite out of each extra dollar. It’s not like a flat tax where everyone pays the same percentage regardless of whether they’re flipping burgers or running a tech giant in Cupertino.

The Real Numbers for 2025 and 2026

For the 2025 tax year (the taxes you’re likely thinking about right now), the rates start at a tiny 1% and climb all the way up to 12.3%. But wait, there’s a catch. If you’re a high earner making over $1 million, you get hit with an extra 1% surcharge for mental health services. That brings the top rate to 13.3%.

Wait, it actually gets higher.

As of 2024 and continuing through 2026, California removed the wage cap on State Disability Insurance (SDI). That’s an extra 1.1% tax on all your wages. So, if you’re at the very top of the food chain, your all-in marginal rate can actually touch 14.4%.

What Is the Income Tax Rate in California? Breaking Down the Brackets

Most people think if they "fall into" a high bracket, all their money is taxed at that rate. That is a total myth.

If you’re single and your taxable income is $100,000, you don't pay 9.3% on the whole hundred grand. You pay 1% on the first chunk, 2% on the next, and so on. It’s like filling up buckets. You only pay the higher rate on the money that spills over into the higher bucket.

2025 Filing Brackets (Single Filers)

For someone filing single or married filing separately, here is how those "buckets" look for the 2025 tax year:

- 1% on income from $0 to $10,756

- 2% on income from $10,757 to $25,499

- 4% on income from $25,500 to $40,245

- 6% on income from $40,246 to $55,866

- 8% on income from $55,867 to $70,606

- 9.3% on income from $70,607 to $371,479

- 10.3% on income from $371,480 to $445,771

- 11.3% on income from $445,772 to $742,953

- 12.3% on everything over $742,953

If you are married and filing jointly, those income thresholds basically double. It makes the "marriage penalty" a bit less painful in the Golden State compared to some other places.

Why Your "Taxable Income" Isn't Your Salary

You've got to remember that these rates apply to taxable income, not your gross salary. Before the FTB applies these percentages, they let you take some deductions. For 2025, the California standard deduction is $5,706 for singles and $11,412 for joint filers.

🔗 Read more: Why Really Neat Cleaning 4000 Ponce De Leon is Changing the Coral Gables Office Scene

It’s a bit lower than the federal standard deduction, which is why more people in California end up itemizing things like mortgage interest or charitable donations on their state returns even if they don't do it for the IRS.

The "Millionaire Tax" and Other Surprises

California loves its surcharges. Since 2004, the Mental Health Services Act has added that 1% tax on any taxable income above $1 million. In 2024, Prop 1 actually expanded how that money is spent, focusing heavily on housing and substance abuse treatment. If you're lucky enough to have $2 million in taxable income, that first million is safe from this specific surcharge, but the second million gets hit with it.

Then there's the SDI change. This one sort of flew under the radar for a lot of people until they saw their January paychecks. Previously, California stopped taking the 1.1% SDI tax once you hit a certain income (it was around $153,000 in 2023). Now? There is no limit. If you earn $10 million, you pay 1.1% on all of it.

Capital Gains: No Special Treatment

In the federal system, if you hold an investment for over a year, you get a lower "long-term capital gains" rate.

👉 See also: Pennymac Mortgage Customer Service Explained: What Most People Get Wrong

California? Nope.

The state treats your stock profits and Bitcoin gains exactly like the money you earn at your 9-to-5. It’s all "ordinary income." This is a massive factor for tech workers with RSU or stock option packages. If you sell your NVIDIA stock for a $100,000 profit, California is going to want its piece at your top marginal rate.

Credits That Actually Help

It's not all bad news. California has some of the most robust tax credits in the country if you qualify.

- CalEITC: For lower-income working families, this can put up to $3,756 back in your pocket for the 2025 tax year.

- Young Child Tax Credit (YCTC): If you have a kid under 6, you might get an extra $1,177.

- Renter’s Credit: It’s small—usually $60 for singles or $120 for joint filers—but if you make under certain limits (around $50k-$100k depending on status), it's a little something back.

Residency: The Trap Most People Fall Into

You can't just buy a house in Las Vegas, spend two weekends there, and tell California you're no longer a resident. The FTB is notoriously aggressive about "residency audits." They look at everything: where you're registered to vote, where your doctors are, where your kids go to school, and even where you keep your "prized possessions" (like your dog or your art collection).

If you earn money from a California source—like a rental property in San Diego or a job based in LA—you’re likely paying California taxes on that specific income even if you live in Timbuktu.

Moving Forward With Your Taxes

Understanding the California tax landscape is basically a part-time job. With rates ranging from 1% to over 14% when you count all the bells and whistles, the difference between a good tax strategy and a "just winging it" approach can be thousands of dollars.

Actionable Steps to Take Now:

- Adjust Your Withholding: If you were surprised by a big bill last April, go to the FTB website and use their withholding calculator to update your DE-4 form with your employer.

- Track Your Deductions: Since California's standard deduction is low, keep meticulous records of medical expenses that exceed 7.5% of your AGI and any disaster-related losses.

- Max Out Pre-Tax Accounts: Contributions to a 401(k) or traditional IRA lower your California AGI, which can actually keep you in a lower tax bracket.

- Check Your Residency Ties: If you're planning a move, start documentating the "closest connection" to your new state immediately to avoid a residency audit down the line.

The rules for the 2025 and 2026 tax years are already locked in, so the best time to plan is before the year ends.