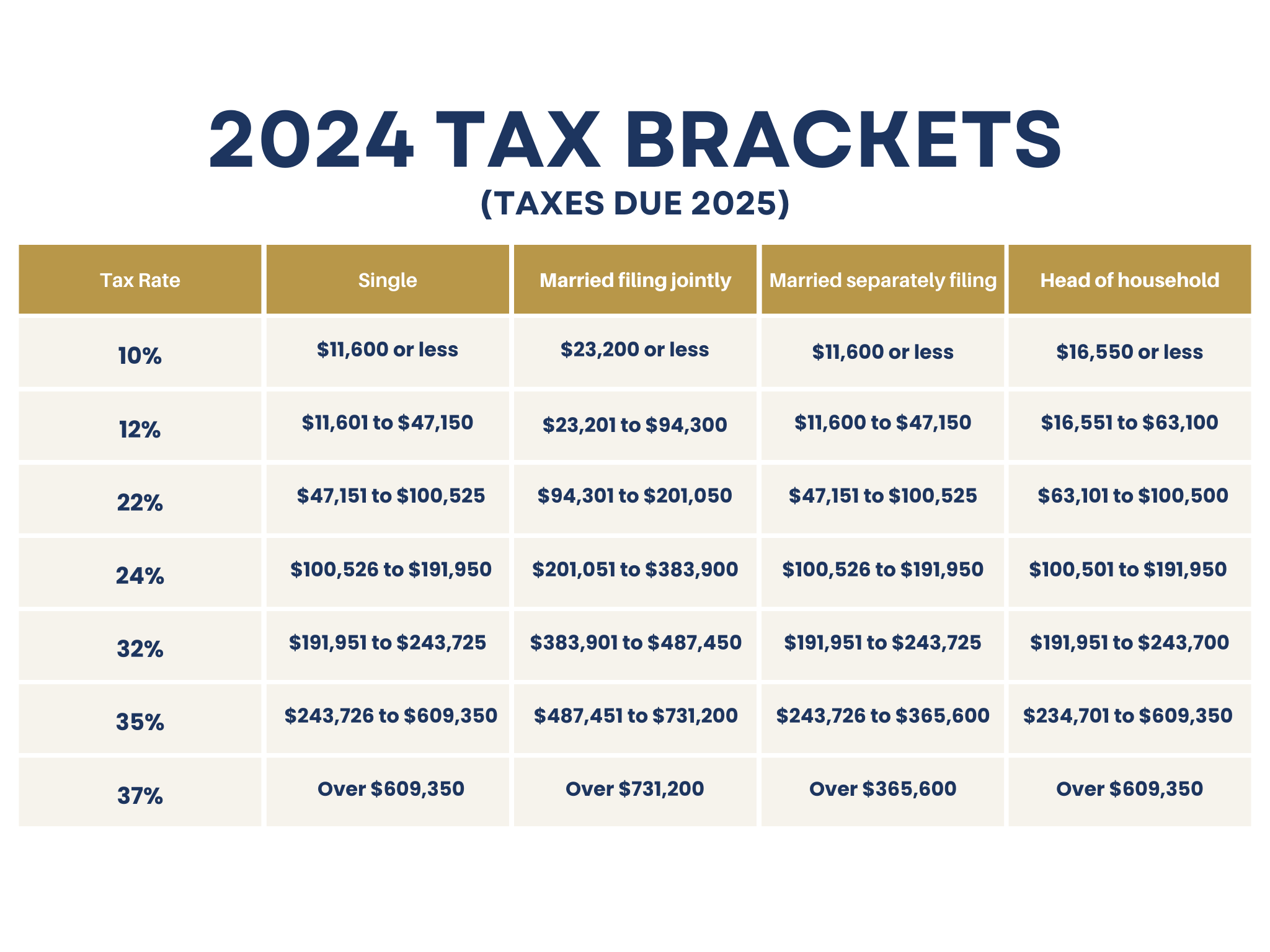

Living in the Golden State comes with a "sunshine tax." We all know it. But when you sit down to look at the california income tax rate brackets 2025, things get messy fast. California doesn't just have a high tax rate; it has one of the most complex, progressive systems in the entire country.

It’s a bit of a rollercoaster.

If you’re making a modest income, your rate might actually be lower than what you’d pay in a "red" state like Indiana or Utah. But once you start climbing that professional ladder? Yeah, the Franchise Tax Board (FTB) starts taking a much bigger bite. Honestly, most people just see the 13.3% headline number and freak out, but hardly anyone actually pays that top marginal rate. You have to be doing incredibly well to hit those numbers.

How the Brackets Shifted for 2025

California adjusts its tax brackets every year based on the California Consumer Price Index (CCPI). Basically, they try to prevent "bracket creep." That’s the annoying phenomenon where inflation pushes you into a higher tax bracket even though your actual purchasing power hasn't changed at all. For the 2025 tax year (the taxes you’ll file in early 2026), the brackets have shifted upward by about 3.1%.

This is a good thing for your wallet. It means more of your income stays in those lower-percentage "buckets" before jumping to the next level.

Let's look at how the single filers stack up this year. If you're single, your first $10,756 of taxable income is taxed at a measly 1%. That's practically nothing. But the ladder gets steep. The next chunk, up to $25,499, is taxed at 2%. Then it jumps to 4%, 6%, 8%, and 9.3%.

Most middle-class Californians find the bulk of their income sitting in that 9.3% bracket. For single filers in 2025, that 9.3% rate kicks in once you pass $68,889 in taxable income. If you're married filing jointly, that threshold doubles to $137,778.

The Mental Trap of Marginal Rates

People get this wrong constantly. They think if they "hit" the 9.3% bracket, all their money is taxed at 9.3%.

That’s not how it works.

Tax brackets are like a series of buckets. You fill the 1% bucket first. Then the 2% bucket. Only the dollars that spill over into the 9.3% bucket get taxed at that higher rate. Your effective tax rate—the actual percentage of your total income that goes to Sacramento—is always going to be lower than your top marginal bracket.

🔗 Read more: At Home French Manicure: Why Yours Looks Cheap and How to Fix It

The Millionaire’s Tax and the Mental Health Services Act

We can’t talk about california income tax rate brackets 2025 without mentioning the extra stuff. California has a "Mental Health Services Act" tax. This is an additional 1% surcharge on taxable income in excess of $1 million.

So, if you’re a high-earner, your top rate isn’t just the 12.3% found in the standard table. It’s 13.3%. This is why you see headlines about professional athletes or tech founders fleeing to Florida or Texas. When you're making $5 million a year, that 13.3% is a massive number. For the rest of us? It’s a distant concern, but it’s the reason California holds the title for the highest top marginal rate in the U.S.

Standard Deductions and Personal Credits

Your "taxable income" isn't the same as your salary. Thankfully.

For 2025, the California standard deduction has increased. For single filers, it’s now $5,463. For married couples filing jointly, it’s $10,926. You subtract this from your adjusted gross income before you even look at the tax brackets.

Then there are the personal exemption credits. These are actually pretty decent in California compared to other states. For 2025, the personal exemption credit is $148 for individuals. If you have dependents, you get another $475 credit per dependent.

Think about that for a second. If you’re a married couple with two kids, you’re looking at over $1,200 in direct tax credits. That’s not a deduction from your income; that’s a straight-up reduction of your tax bill. It helps take the sting out of those higher percentages.

Why the 2025 Numbers Matter Right Now

You might think, "Why do I care about 2025 rates when I haven't even finished my 2024 taxes?"

Because of withholding.

If you’re an employee, your company is already using these 2025 tables to figure out how much to take out of your paycheck. If you had a big life change—got married, had a kid, bought a house—your withholding might be totally out of whack. California’s high rates mean that if you under-withhold, the penalty and the year-end bill can be brutal.

💡 You might also like: Popeyes Louisiana Kitchen Menu: Why You’re Probably Ordering Wrong

Check your pay stub. If the "CA State Tax" line looks too small or too large, you might want to update your DE 4 (the California version of the federal W-4).

The Impact of High Inflation on Your Tax Bill

While the 3.1% adjustment for 2025 is better than nothing, it’s worth noting that it doesn't always keep pace with the actual cost of living in places like San Francisco, San Diego, or Los Angeles.

Rent is higher. Groceries are higher.

When the state adjusts brackets, they use a statewide average. If you live in a high-cost coastal city, you might feel like you're being pushed into higher brackets even though you're barely treading water. This is the "hidden" side of California's progressive tax structure. It assumes that if you're making $100,000, you're doing well. In Fresno, maybe. In Palo Alto? That’s barely making rent.

Capital Gains: The Great Equalizer (In a Bad Way)

Here is a kicker that most people forget until April. California does not have a preferential rate for long-term capital gains.

Federal taxes give you a break if you hold an investment for more than a year. California says, "Nope." Whether you earned that money at a desk job or by selling Apple stock you held for a decade, it’s all taxed at the same california income tax rate brackets 2025.

If you sold a home or some crypto in 2025, be prepared. You’ll owe the state the same percentage on those gains as you do on your salary. This catches a lot of people off guard, especially those moving into the state from places like Nevada where there is no state income tax at all.

Understanding the "SDI" Tax on Your Paycheck

If you look at your California paycheck, you'll see more than just "PIT" (Personal Income Tax). You’ll see SDI.

State Disability Insurance is technically a tax, though it’s separate from the income tax brackets. As of 2024, California removed the taxable wage cap for SDI. It used to be that you stopped paying into SDI once you earned over a certain amount (around $153k). Now? You pay 1.1% on every single dollar of wages, no matter how much you make.

📖 Related: 100 Biggest Cities in the US: Why the Map You Know is Wrong

For high earners, this was effectively a massive tax hike that flew under the radar. It stays in place for 2025. When you’re calculating your "California tax burden," you really have to add that 1.1% on top of the bracket rates to see the true picture.

The Bottom Line on California Taxes

It’s easy to complain about California’s taxes, and many people do—with good reason. We have some of the highest rates in the country. But for the average worker, the system is designed to be highly progressive.

If you’re a teacher or a nurse making $75,000, your state tax bill isn't actually the monster people make it out to be once you factor in the standard deduction and credits. The real pain is felt by the "middle-upper" class—those making between $150,000 and $400,000—who hit those high single-digit and low double-digit brackets while still facing a massive cost of living.

What You Should Do Next

Don't wait until next April to see how these brackets affect you.

First, grab your last pay stub and look at your year-to-date California withholding. Compare it against the 2025 brackets to see if you're on track.

Second, if you’re a business owner or an independent contractor, adjust your estimated tax payments now. The 3.1% bracket shift means you might be able to pay slightly less in estimates than you did last year, or at least keep more of your money if your income stayed flat.

Third, look into California-specific deductions. While California doesn't follow all federal tax laws (it's a "non-conformity" state), there are still ways to lower your taxable income, like contributing to a 401(k) or a traditional IRA, which reduces your federal AGI and, by extension, your California taxable income.

The california income tax rate brackets 2025 are set. The math is the math. The only thing you can control is how you plan for it. Stay on top of your withholding, keep receipts for any potential deductions, and maybe—just maybe—the "sunshine tax" won't feel quite so heavy this year.