Tax season is basically the adult version of a horror movie, except you can't just turn off the TV when it gets too scary. You're sitting there, staring at a screen, wondering why the math doesn't seem to add up. Most people just want to calculate how much tax I will pay without feeling like they need a PhD in accounting. It’s frustrating. It's confusing. Honestly, it’s a bit of a scam that the IRS knows exactly what you owe but makes you play a guessing game anyway.

Let’s get real.

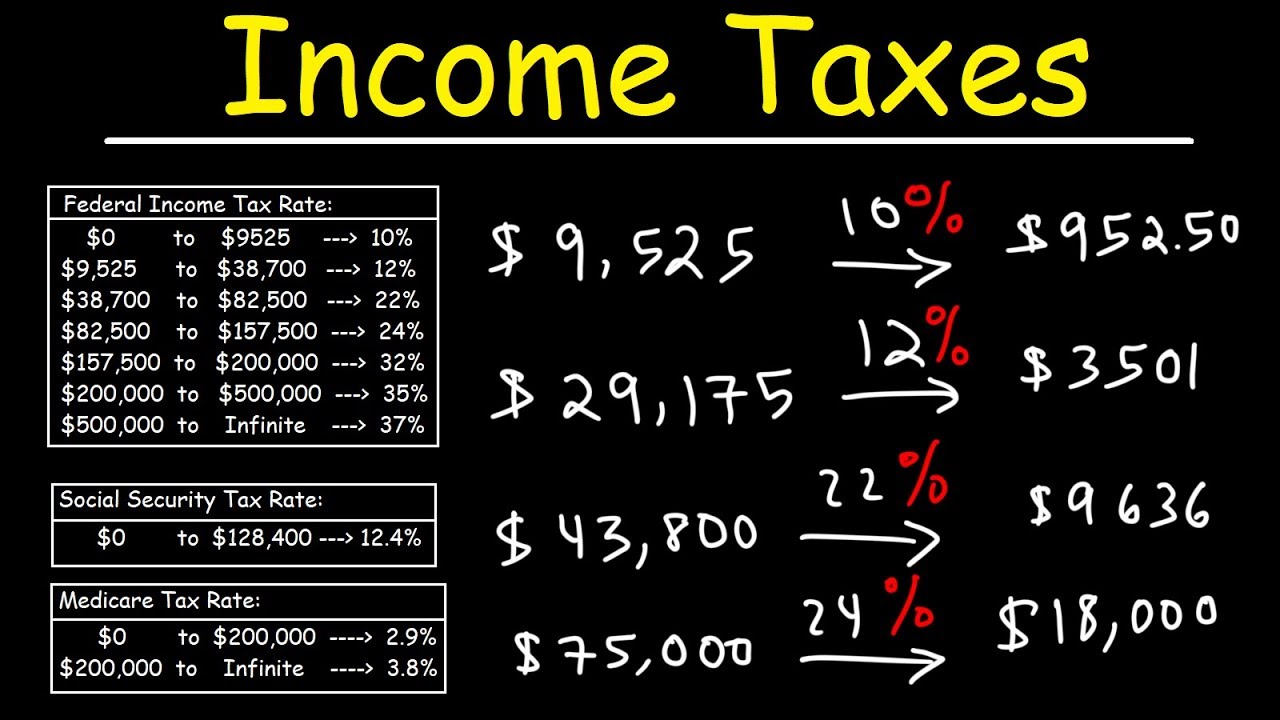

The biggest mistake people make is looking at their tax bracket and assuming that’s the percentage they pay on everything. If you're in the 22% bracket, you aren't losing 22 cents of every single dollar you earned to the federal government. That’s not how it works. We live in a progressive tax system. Think of it like a series of buckets. The first bucket fills up at 10%, the next at 12%, and so on. You only pay the higher rate on the money that "overflows" into that specific bucket.

Why Your Effective Rate Is the Only Number That Matters

When you try to calculate how much tax I will pay, you’ll likely see two different numbers: your marginal rate and your effective rate. Your marginal rate is just the highest bracket you touched. It’s a vanity metric. Your effective tax rate is the actual percentage of your total income that goes to Uncle Sam after all the dust settles.

For 2025 and 2026, the standard deduction is your best friend. It’s a massive chunk of money the government ignores before they even start counting your income. For single filers in 2025, that’s $15,000. If you’re married filing jointly, it’s $30,000. You don't even have to prove you spent it on anything. It’s just... gone. Poof. Tax-free.

If you earned $60,000 as a single person, you aren't being taxed on $60,000. You’re being taxed on $45,000. That’s a huge distinction.

The Hidden Tax: FICA and Self-Employment

If you’re a W-2 employee, you might notice your paycheck is already lighter because of Social Security and Medicare. That’s 7.65%. Your employer matches it. But if you’re a freelancer or a "side hustle" king, you get hit with both sides—the full 15.3%. This is the "Self-Employment Tax," and it catches people off guard every single April.

You're basically paying for the privilege of being your own boss.

🔗 Read more: Stock Market Today Hours: Why Timing Your Trade Is Harder Than You Think

Deductions vs. Credits: A Massive Difference

People use these terms interchangeably. They shouldn't.

A deduction reduces the amount of income you’re taxed on. If you’re in the 24% bracket and you have a $1,000 deduction, you "save" $240.

A credit is a straight-up gift. It’s a dollar-for-dollar reduction of your tax bill. If you owe $5,000 and you have a $2,000 Child Tax Credit, you now owe $3,000. Simple. Powerful. Always look for credits first. The Earned Income Tax Credit (EITC) is one of the most significant, but it has very specific income limits that change every year based on how many kids you have.

The Capital Gains Trap

Did you sell some Nvidia stock? Maybe you finally offloaded that Bitcoin?

If you held it for more than a year, you’re looking at Long-Term Capital Gains rates—0%, 15%, or 20%. Most people fall into the 15% camp. But if you sold it in less than a year, it’s taxed at your ordinary income rate. That could be a massive jump. Timing your sales by even a single day can save you thousands of dollars.

How to Actually Calculate How Much Tax I Will Pay Without Losing Your Mind

You don't need fancy software to get a "napkin math" estimate.

First, grab your total gross income. Subtract your 401(k) contributions (the traditional ones, not Roth) and your HSA contributions. These are "above-the-line" deductions. They lower your Adjusted Gross Income (AGI) before you even get to the standard deduction.

💡 You might also like: Kimberly Clark Stock Dividend: What Most People Get Wrong

Next, take that AGI and subtract your standard deduction ($15,000 or $30,000 for most).

Now you have your Taxable Income.

Take that number and apply the brackets. For a single filer in 2025:

- 10% on the first $11,925

- 12% on the amount between $11,925 and $48,475

- 22% on anything above $48,475 (up to $103,350)

If your taxable income is $50,000, you pay 10% on the first chunk, 12% on the middle chunk, and 22% only on the last $1,525.

It's tedious. I know.

What About State Taxes?

Don't forget the state. Unless you live in Florida, Texas, Washington, Nevada, Wyoming, South Dakota, or Tennessee, you’re likely writing another check. Places like California or New York have progressive systems similar to the federal one, while states like Illinois or Pennsylvania use a "flat tax" where everyone pays the same percentage regardless of income.

Common Blind Spots and Mistakes

I’ve seen people forget to account for their bonuses. Bonuses are often "withheld" at a flat 22% rate by employers, but that doesn't mean they are taxed at 22%. If your actual top bracket is 32%, you're going to owe more money come tax time because your employer didn't take out enough.

📖 Related: Online Associate's Degree in Business: What Most People Get Wrong

On the flip side, if you're in the 12% bracket, you’ll get a nice refund because they took out too much.

Another big one? The Alternative Minimum Tax (AMT). It was originally designed to prevent the ultra-wealthy from using too many loopholes, but inflation has pushed more upper-middle-class families into its crosshairs. If you have a lot of ISO (Incentive Stock Options) from a tech job, the AMT can absolutely wreck your finances if you aren't prepared for it.

Real-World Example: The "Surprise" Tax Bill

Imagine Sarah. She earns $100,000. She contributes $10,000 to her 401(k).

Her AGI is $90,000.

She takes the $15,000 standard deduction.

Her taxable income is $75,000.

Using the brackets, she’ll owe roughly $11,000 in federal income tax.

Her effective rate? About 11%.

But she also has to pay about $7,650 in FICA taxes.

Total federal hit: $18,650.

If she lived in a state with a 5% flat tax, add another $4,500.

Suddenly, Sarah is taking home $76,850 out of her $100,000 salary.

Moving Toward a Better Estimate

To truly calculate how much tax I will pay, you have to look at your "withholding" on your paystubs. If the total tax you’ve paid throughout the year is less than that final number Sarah hit, you’re writing a check to the IRS. If it’s more, you get a refund.

A refund isn't a "bonus." It's an interest-free loan you gave to the government. Ideally, you want your refund to be as close to zero as possible.

Specific Steps to Take Right Now

- Check your last paystub. Look at the "Federal Tax YTD" (Year to Date) line.

- Estimate your year-end income. Include interest from high-yield savings accounts—they send 1099-INT forms, and yes, that money is taxable.

- Use the IRS Tax Withholding Estimator. It’s a free tool on IRS.gov that is surprisingly decent. It helps you adjust your W-4 so you don't get a nasty surprise in April.

- Maximize your HSA. If you have a high-deductible health plan, the HSA is the only "triple-tax-advantaged" account. No tax going in, no tax on growth, and no tax coming out for medical bills. It’s the best legal tax dodge in existence.

- Gather your receipts if you itemize. Most people take the standard deduction, but if your mortgage interest, state/local taxes (up to $10,000), and charitable gifts exceed $15,000, you should itemize.

Stop guessing. Tax laws change, brackets shift with inflation, and life happens. Getting a handle on these numbers in October or November is much better than crying over a spreadsheet in April. Review your W-4 today and make sure you aren't overpaying—or worse, underpaying and facing penalties.