Cash is boring until it starts earning 5%. For a long time, business owners treated their operating reserves like a junk drawer—just a place to shove extra capital while waiting for a payroll spike or a tax bill. But things changed. When the Federal Reserve hiked rates aggressively throughout 2023 and held them steady into 2024, business cd interest rates suddenly became a legitimate line item for bottom-line growth. If you’re sitting on $50,000 or $500,000 in a standard business checking account, you’re essentially giving the bank a free loan. That’s a mistake.

Let's be real. Most people think a Certificate of Deposit is a "set it and forget it" tool for retirees. It's not. For a company, it’s a strategic liquidity play. You’re trading immediate access for a guaranteed return. But the market is fragmented right now. You’ll see one-year rates at a local credit union hovering around 3.00% while an online-first player like Live Oak Bank or Capital One is pushing way higher. The spread is massive.

The Yield Curve Is Weird Right Now

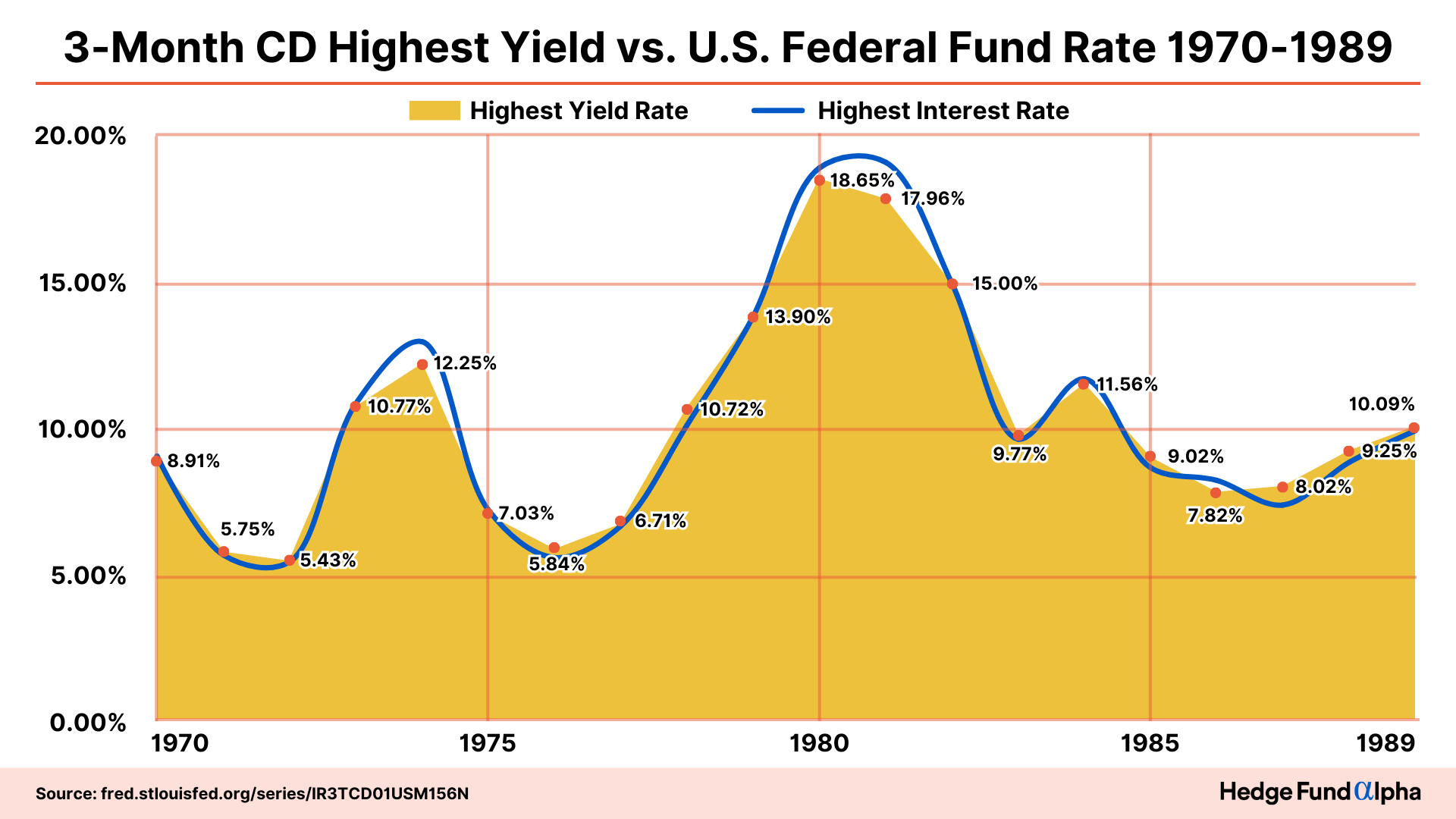

Normally, if you lock your money up for five years, you get a higher rate than if you lock it up for six months. That’s how a "normal" world works. But we’ve been living through an inverted yield curve. This means short-term business cd interest rates have frequently outperformed long-term ones.

Why? Because banks are betting that rates will drop in the future. They are willing to pay you 5.25% for a 6-month term because they think by next year, the going rate will be 4.00%. If you lock in a 5-year CD at 4.50% today, you might actually be winning the long game, even if it feels "lower" than the short-term offers. It’s a game of chicken with the Fed.

I talked to a CFO last month who was furious. He had $2 million in a "high-yield" sweep account earning 2.10%. He realized that by moving just half of that into a tiered CD ladder, he could cover the salary of a junior marketing assistant just on the interest alone. That is the scale we are talking about. It isn’t just "pennies." It’s headcount. It’s R&D budget.

How to Avoid the Liquidity Trap

The biggest fear every business owner has is the "what if." What if the oven breaks? What if we get sued? What if a massive inventory opportunity drops in our lap next Tuesday?

🔗 Read more: 121 GBP to USD: Why Your Bank Is Probably Ripping You Off

If your money is in a CD, it’s "locked."

But "locked" is a relative term. Most business CDs come with an Early Withdrawal Penalty (EWP). Usually, this is something like 90 days or 180 days of interest. Honestly, if you’re earning 5% and you have to break the CD early, you often still end up ahead compared to leaving that money in a 0.05% checking account for six months. You just lose the "bonus" profit.

Strategy: The Ladder vs. The Barbell

Don't just dump all your cash into a single 12-month CD. That's amateur hour.

The Ladder: Split your $100k into four chunks of $25k. Put one in a 3-month, one in a 6-month, one in a 9-month, and one in a 12-month. Every three months, a "rung" matures. If you need the cash, take it. If you don't, roll it into a new 12-month CD. You’ve created a cycle of perpetual liquidity.

The Barbell: Put some in a very short-term liquid account (like a money market) and the rest in a long-term 2-year CD. This ignores the "middle" ground. It’s for businesses with very predictable cash flows but a need for a high-interest "anchor."

💡 You might also like: Yangshan Deep Water Port: The Engineering Gamble That Keeps Global Shipping From Collapsing

What Most People Get Wrong About Business CD Interest Rates

Credit unions. Seriously. Everyone looks at Chase, Wells Fargo, or BofA. Those "too big to fail" banks often have the worst business cd interest rates because they don't need your deposits. They have plenty of cash.

Small, regional banks and credit unions are often "hungry" for deposits to fund their local lending. You’ll find "specials"—like an 11-month CD or a 17-month CD—that offer significantly higher yields than the standard 12 or 24-month terms. These odd-term durations are almost always where the best deals hide.

Also, watch out for the "Business" vs. "Personal" distinction. Some banks offer incredible rates on personal CDs but give business entities the cold shoulder with lower rates and higher minimums. You have to ask specifically for the business rate sheet. Sometimes, you can negotiate. If you're bringing $250,000+ to the table, don't just accept the website rate. Call the branch manager. Ask them if they can "bump" the rate by 10 or 20 basis points to win your business. It works more often than you'd think.

Is the High-Interest Era Over?

We've been spoiled. For a while, getting 5% was easy. As inflation cools, the pressure on the Fed to cut rates increases. We've already seen the "peak" for many institutions.

If you're waiting for rates to go back to 7%, you're probably going to be waiting a long time. The move right now for most savvy operators is "locking in" duration. If you can get a 4.50% or 4.75% rate on a 2-year business CD, that might look like a genius move 18 months from now when the standard savings rate has plummeted back toward 2%.

📖 Related: Why the Tractor Supply Company Survey Actually Matters for Your Next Visit

The Fine Print That Bites

Read the "Section 7" or whatever the boilerplate is on the signature card. Specifically, look at:

- Automatic Renewal: Most CDs will automatically roll over into a new term once they mature. The problem? They often roll over into the "standard" rate, which is usually garbage compared to the "special" rate you initially signed up for. You usually have a 10-day grace period to pull your money out. Mark it on your calendar. If you miss it, you're stuck for another year at a bad rate.

- Compounding Frequency: Does it compound daily, monthly, or quarterly? Daily is best. Over a large balance, the difference between quarterly and daily compounding can be hundreds of dollars.

- Minimum Balance for APY: Some banks require a $10,000 minimum just to open the account, but you might need $50,000 to actually hit the advertised Annual Percentage Yield (APY).

Why Not Just Use a Money Market Account?

Money Market Accounts (MMAs) are great because they offer checks and debit cards. But the rate is "variable." The bank can drop your rate on a Monday morning without asking you.

With a CD, you’re buying a contract. They cannot lower your rate. That certainty is worth the lack of a debit card, especially if you know that money is earmarked for next year's expansion or a specific tax obligation.

Actionable Steps for Your Business Reserve

Stop letting your cash rot. Follow this sequence:

- Audit your "Idle" Cash: Look at your lowest balance over the last 12 months. If you never dipped below $40,000, then that $40,000 is effectively "idle." It should be earning for you.

- Check Online Giants First: Look at providers like EverBank, Live Oak Bank, or Alliant Credit Union. These often set the benchmark for high-end business cd interest rates.

- The Local "Ask": Take those online rates to your local bank where you have your primary checking. Tell them, "I want to keep my money here, but I can't ignore a 2% difference in yield. Can you match this?"

- Document the EWP: Before you sign, write down exactly how much it costs to break the CD. If the penalty is only 3 months of interest, and you're 9 months into a 12-month term, you've already "won" even if you have to close it early.

- Set the Grace Period Reminder: Put an alert in your phone for 7 days before the CD matures. This is your window of power. Don't let the bank auto-renew you into a low-yield trap.

Managing a business is hard enough. Don't make it harder by leaving free money on the table. In a world where margins are tight and labor is expensive, the interest earned on your reserves might just be the easiest "profit" you'll ever make.