Selecting a health insurance plan usually feels like a math test where the numbers keep moving. You want the best care, but you also don't want to go broke paying for a "what if" scenario. Among the sea of acronyms, Blue Cross Blue Shield PPO plans often stand out as the premium choice for people who hate being told which doctor they can see.

It's about freedom. Honestly, the biggest reason people gravitate toward a PPO (Preferred Provider Organization) is that they don't want a gatekeeper. With an HMO, you basically have to ask your primary doctor for permission—a referral—to see anyone else. PPOs don't do that. You just go.

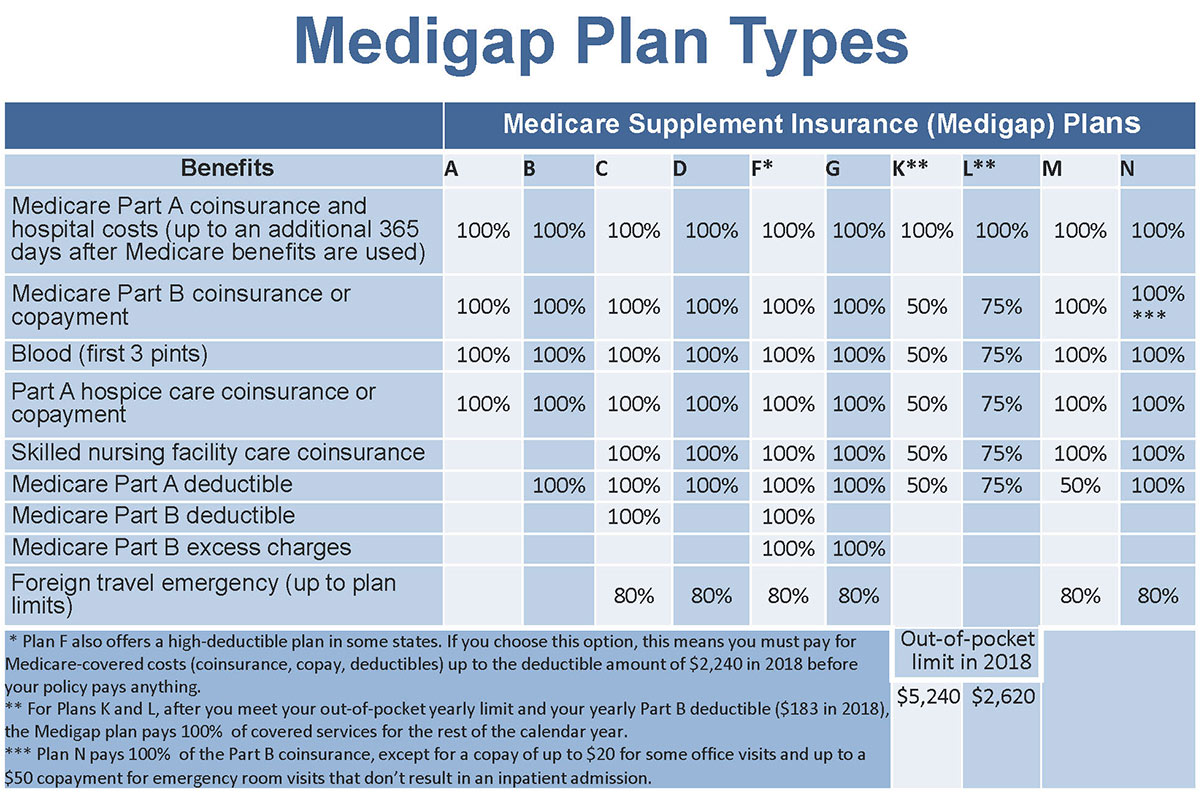

👉 See also: Toric Lenses vs Regular: What Your Optometrist Might Not Mention

What Makes Blue Cross Blue Shield PPO Plans Different?

The "Blue" network is massive. That’s not just marketing fluff. Because Blue Cross Blue Shield (BCBS) is actually a federation of 33 independent companies, their reach is nationwide. When you have a PPO through them, you’re usually tapping into the BlueCard® program. This is a big deal if you travel. It means you can use the local BCBS network in almost any state as if you were back home.

Most plans today are restrictive. They want you in a tight little circle of doctors to keep costs down. BCBS PPO plans take the opposite approach. They give you a "preferred" list of providers where you pay the least, but they still pay something if you go out of network.

Expect to pay more for this. It's the trade-off. PPOs generally have higher monthly premiums than HMOs or EPOs. You're paying for the right to skip the referral line and see a specialist in another city if that’s where the best care is located.

The Referral-Free Life

Imagine you wake up with a weird skin spot.

With an HMO:

- Call your primary care doctor.

- Wait a week for an appointment.

- Get the doctor to look at it.

- Get a paper referral for a dermatologist.

- Wait another two weeks for the specialist.

With one of the Blue Cross Blue Shield PPO plans, you just find a dermatologist in the directory and call them. That’s it. You bypass the middleman. For people with chronic conditions or those who just value their time, this is the "killer feature" of the PPO.

Understanding the True Cost of Flexibility

Health insurance is never actually free, even if your employer pays the premium. You've got to look at the "metal" levels. Most BCBS companies categorize their PPO offerings into Bronze, Silver, Gold, and Platinum.

A Bronze PPO is kinda like a high-deductible safety net. You'll pay a low monthly fee, but if you actually get sick, you might have to shell out $7,000 or more before the insurance company starts covering the big bills. On the flip side, a Gold or Platinum plan has a scary-high monthly premium but might have a $0 deductible and very low copays for every visit.

Real-World Price Tags (2026 Estimates)

Looking at recent 2026 filings, a Silver-level PPO for a 40-year-old might range from $500 to $700 a month depending on the state.

In North Carolina, for instance, the Blue Advantage (PPO) often costs significantly more than the Blue Value (a more restrictive network) because it grants access to nearly every hospital in the state.

💡 You might also like: Why a pic of 6 week old fetus looks nothing like what you expect

- In-Network Copay: Usually $25–$50 for a primary visit.

- Specialist Copay: Often $60–$100.

- Out-of-Network: You might pay 50% of the cost, and the doctor can "balance bill" you for the rest.

Don't ignore the out-of-pocket maximum. This is the most important number on your insurance card. It is the absolute limit on what you will pay in a calendar year for covered services. For 2026, many BCBS PPO plans have an in-network maximum around $9,000 for individuals, though some premium plans keep it much lower.

The "Out-of-Network" Trap

PPOs allow you to see out-of-network doctors, but there is a catch that catches people off guard.

Insurance companies use something called "Allowed Amounts."

Say your out-of-network surgeon charges $5,000 for a procedure.

Your BCBS PPO plan says the "allowed amount" for that surgery is $3,000.

Even if your plan says they cover 50% of out-of-network care, they are only paying 50% of that $3,000.

You are responsible for the other $1,500 PLUS the $2,000 difference the doctor charged above the allowed amount.

This is why staying "in-network" is still the smartest move even when you have the freedom to leave it. The PPO just ensures you aren't stuck with 100% of the bill in an emergency or a niche specialty situation.

👉 See also: How to induce period early: What actually works versus what is just a myth

Is a BCBS PPO Plan Right for You?

It really comes down to your lifestyle.

If you are healthy, rarely see a doctor, and don't mind staying in a local network, a PPO is probably overkill. You're paying for a "luxury" feature you aren't using.

However, you should seriously consider a PPO if:

- You have a preferred specialist who doesn't participate in many HMOs.

- You split your time between two states (like snowbirds).

- You have a complex medical history and don't want to wait for referrals.

- You want the peace of mind that comes with the widest possible hospital choice.

Many people find that the "BlueOptions" or "BlueChoice" versions of these plans offer a middle ground. They use a slightly smaller network than the massive national PPO but still keep the "no referral" rule. It’s a way to shave $50 off the monthly premium without losing the core benefit.

Actionable Steps for Choosing Your Plan

Don't just look at the monthly premium. That's a rookie mistake. Total up your expected costs: 12 months of premiums + your average number of doctor visits + the cost of your regular prescriptions.

- Check the "National" vs. "Local" network. Some BCBS PPOs are "Local PPOs," meaning you get out-of-network coverage, but you don't get the "in-network" rates when you travel to another state. Look for the "PPO" inside a small suitcase icon on the member ID card—that signifies the national BlueCard® access.

- Verify your specific medications. Every BCBS plan has a "formulary" (a list of covered drugs). A PPO might be great for doctor access but terrible for your specific brand-name prescription. Check the 2026 drug tiers before signing.

- Search the Provider Finder tool. Don't assume your doctor takes it. BCBS networks change every year. Use the online tool and filter specifically by the plan name (like "Blue Preferred" or "Preferred Blue") to be 100% sure.

- Look for "Value Choice" providers. Many 2026 plans offer $0 or $10 copays if you use specific designated clinics or virtual care options, even on a PPO.

The real value of Blue Cross Blue Shield PPO plans isn't just in the coverage—it's in the lack of friction. If you can afford the higher monthly "tax" for that convenience, it's often the most stress-free way to handle American healthcare.

Check your employer's open enrollment portal or the healthcare.gov marketplace to compare these PPOs against the available HMO options. Always download the "Summary of Benefits and Coverage" (SBC) PDF for any plan you are seriously considering; it’s the only place where the fine print about deductibles and emergency room costs is actually clear.