The energy in Omaha right now is... different. For sixty years, we all looked at the Berkshire Hathaway ticker and saw Warren Buffett’s shadow. But it’s early 2026, and the "Post-Buffett Era" isn't a theory anymore. It’s the reality we’re trading in every single morning.

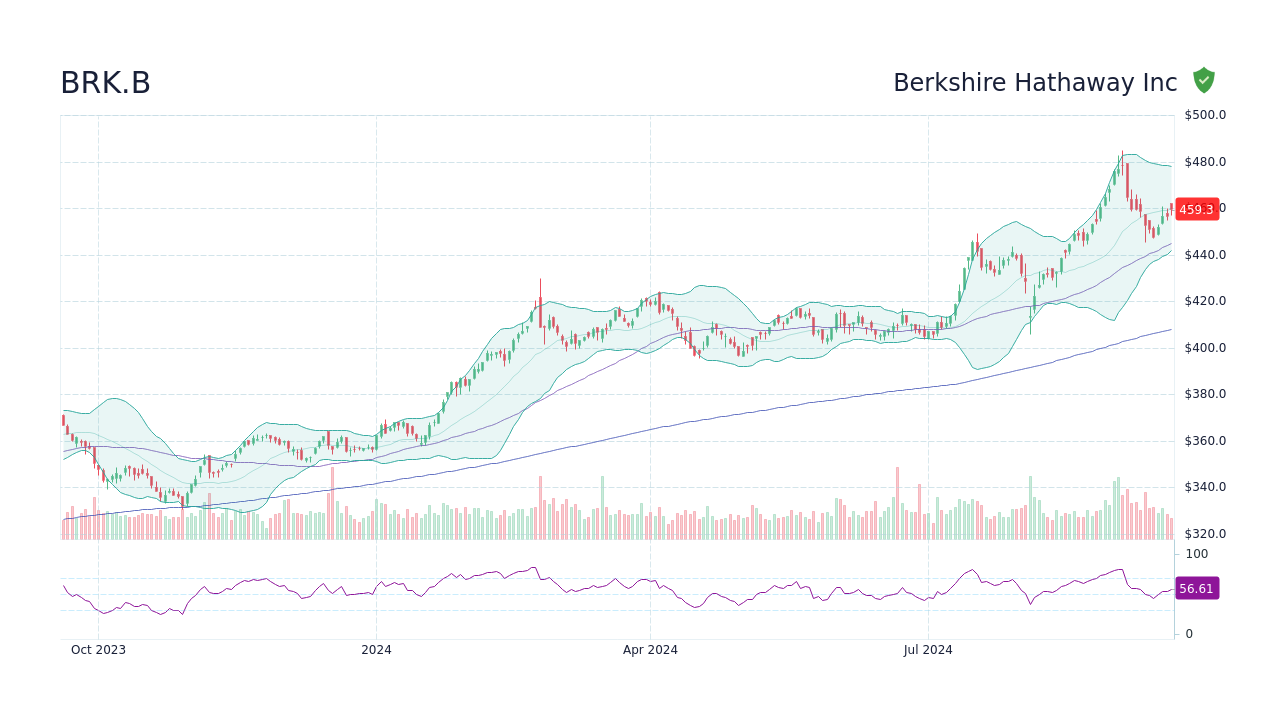

If you’re checking the stock price brk b today, you’ll see it hovering around $493.51. Honestly, it’s been a bit of a tug-of-war lately. We saw the stock flirt with all-time highs near $542 last year, but since the calendar flipped to 2026, the market seems to be holding its breath.

Is Greg Abel the real deal? Can a guy getting paid a $25 million salary—a massive jump from Buffett’s iconic $100,000—keep the magic alive? People are worried. Or maybe they're just cautious. Either way, the "Omaha Oracle" has officially retired from the CEO seat, and the Class B shares are acting like a teenager trying to find their own identity.

What’s Actually Driving the Stock Price BRK B Right Now?

Let's cut through the noise. Most people look at the stock price and think "insurance and railroads." Sure, GEICO and BNSF are the backbone. But the real story in 2026 is that $381 billion cash pile. It is, quite literally, a mountain of money.

Greg Abel isn't just sitting on that cash to be safe. On January 2, 2026, Berkshire closed a $9.7 billion deal to snap up OxyChem, the chemical unit of Occidental Petroleum. It was a classic Berkshire move: quiet, massive, and deeply industrial.

- The Valuation Gap: Simply Wall St recently put out a DCF model suggesting the intrinsic value is way higher—like $787 per share.

- The Reality Check: The market is currently pricing it closer to $493. Why the gap? Investors are pricing in "succession risk."

- The Technicals: We just saw a "Golden Cross" on the charts in early January. For the chart nerds, that’s when the 50-day moving average crosses above the 200-day. It’s usually a bullish sign, but the volume has been a bit thin.

The $25 Million Question: Greg Abel vs. The Legend

The transition hasn't been perfectly smooth for everyone’s nerves. Warren Buffett is 95. He’s still Chairman, but he’s not the one calling the shots on the daily operations anymore.

📖 Related: Yangshan Deep Water Port: The Engineering Gamble That Keeps Global Shipping From Collapsing

Greg Abel has been running the non-insurance side for eight years, so he’s not a newbie. But the culture shift is real. Buffett’s salary was a symbol of "we’re in this together." Abel’s new compensation package is much more "Standard S&P 500 CEO." Some old-school value investors are grumbling, but honestly, if he deploys that $381 billion effectively, nobody is going to care about his paycheck.

Is Berkshire Still a "Forever" Stock?

I get asked this a lot. "Is the stock price brk b going to tank once the market fully realizes Warren isn't at the helm?"

Probably not. Berkshire isn't a stock; it's an ecosystem. Think about it. You've got:

- Energy: Berkshire Hathaway Energy is a beast in the renewables space.

- Insurance: The "float" (the money they hold between collecting premiums and paying claims) reached $176 billion last quarter.

- Manufacturing: From Precision Castparts to Fruit of the Loom, they own the "boring" stuff that makes the world turn.

The company’s operating profit jumped 34% in the last reported quarter (Q3 2025). That doesn't happen by accident. Even with Todd Combs and Ted Weschler managing parts of the portfolio, the "Abel Era" is focusing heavily on the industrial and energy demands triggered by the AI boom.

Why the Recent Softness?

If the company is so great, why did the stock price brk b dip from those $500+ levels we saw in December?

👉 See also: Why the Tractor Supply Company Survey Actually Matters for Your Next Visit

Mainly, it's the "Bank Rally." Berkshire actually missed out on some of the recent surges in the banking sector because they’ve been trimming positions in things like Apple and certain financials. They’re playing defense while everyone else is playing offense.

It’s sorta like being at a party where everyone is drinking tequila and you’re the guy drinking water because you have to drive the bus home. It’s not "fun" to watch the stock stay flat while tech goes to the moon, but when the market eventually trips over its own feet, you’ll be glad you’re on the bus.

Practical Steps for Investors in 2026

If you’re looking at your portfolio and wondering what to do with your BRK.B shares, here is the expert playbook for the current climate.

Watch the $490 Support Level

Technically, if the stock drops below $489, we might see a slide toward the $470 range. That has historically been a massive "buy the dip" zone for institutional investors. If you’re a long-term holder, these micro-fluctuations shouldn't keep you up at night.

Keep an Eye on the 13F Filings

The first filing of 2026 will be huge. It’ll show exactly how Greg Abel and the team are reshuffling the Apple stake. Buffett already trimmed it significantly in 2025; if they keep selling, it tells us they really do think the broader market is overpriced.

✨ Don't miss: Why the Elon Musk Doge Treasury Block Injunction is Shaking Up Washington

Don’t Expect a Dividend Yet

Wall Street analysts like Jonathan Boyar are screaming for a dividend now that the "Stock Picker In Chief" has stepped back. But Berkshire’s culture is anti-dividend. They’d rather buy back their own shares. If the stock price brk b stays below $500, expect the company to get very aggressive with share repurchases. That’s essentially a "synthetic dividend" for you anyway.

Assess Your Time Horizon

Honestly, if you need the money in six months, Berkshire is a coin flip right now because of the leadership transition noise. But if you’re looking at 2030? The underlying earnings power of the subsidiaries is stronger than it’s ever been.

To manage your position effectively, you should track the Price-to-Book (P/B) ratio. Historically, Berkshire is a "screaming buy" when it hits 1.2x book value. Currently, it’s sitting closer to 1.5x. It’s not "dirt cheap," but for the quality of the assets, it’s arguably one of the safest places to park cash in a volatile 2026 market.

Monitor the upcoming earnings report on February 23, 2026. This will be the first full quarterly report where Greg Abel is officially the man at the top. The commentary in that report will set the tone for the rest of the year. Pay less attention to the "Net Income" (which is skewed by stock market swings) and focus entirely on "Operating Earnings." That is the heartbeat of the company.