Honestly, if you looked at Baidu’s stock chart a couple of years ago, you probably would’ve yawned. For a long time, the company felt like that veteran athlete who was great in their prime but was now just sort of... there. People called it the "Google of China," but it felt more like a legacy search engine struggling to find its footing in a world dominated by TikTok and WeChat.

But things have changed. Drastically.

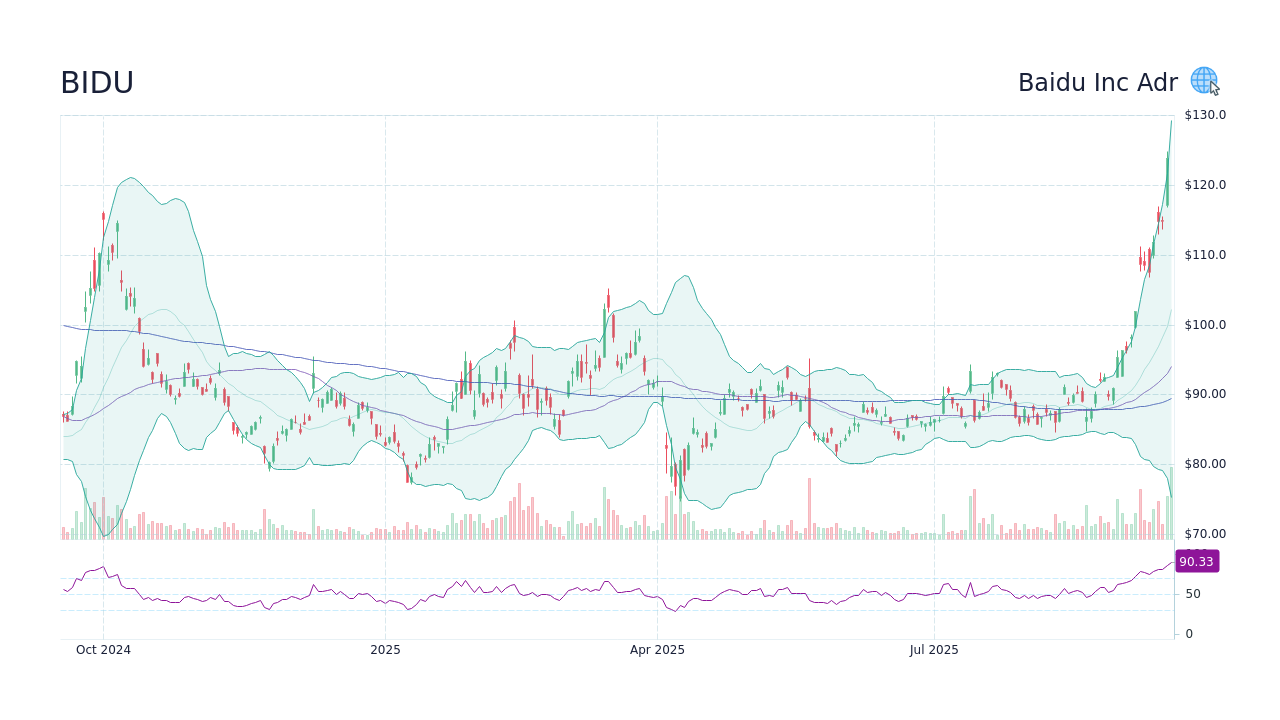

As of mid-January 2026, Baidu's Hong Kong stock (9888.HK) is sitting around the HK$146 mark, a massive recovery from the double-digit lows we saw in 2024. In fact, it recently touched a 52-week high of HK$148 on January 13, 2026. This isn't just a random pump. It’s the result of Baidu finally proving that its multi-billion dollar bet on AI wasn't just corporate fluff.

The company has essentially split into two stories: the old "cash cow" advertising business that’s fighting to stabilize, and the "new" Baidu, which is basically an AI and robotics powerhouse.

The ERNIE Factor and the Death of "Blue Links"

You can’t talk about Baidu without talking about ERNIE Bot. While Western markets were obsessed with GPT-4, Baidu was quietly iterating. In November 2025, they dropped ERNIE 5.0 at the Baidu World conference. This wasn't just a minor update. Robin Li, Baidu’s CEO, called it a "native multimodal model." Basically, it doesn't just "read" text; it sees, hears, and thinks simultaneously.

By January 2026, ERNIE 5.0-0110 hit the top of the LMArena leaderboard for Chinese models, even outranking some versions of GPT-5 and Gemini in specific reasoning tasks.

What does this mean for the stock? It means search is changing.

📖 Related: Oil Market News Today: Why Prices Are Crashing Despite Middle East Chaos

About 70% of Baidu’s mobile search results now feature AI-generated content. Instead of clicking through ten blue links to find a recipe or a flight, the AI just builds the answer for you. This "AI-native" pivot initially scared investors because they didn't know how Baidu would make money if people weren't clicking on ads.

The answer? AI Agents.

Baidu has launched a platform called GenFlow, which has over 20 million active users. These aren't just chatbots; they are digital employees that help businesses sell products and book services. In Q3 2025, revenue from these AI-native marketing services surged by a staggering 262%. That’s the kind of number that makes institutional investors at firms like Citigroup and UBS keep their "Buy" ratings.

Robotaxis: From Science Fiction to Real Revenue

If you visit Wuhan or Beijing today, seeing a car with no driver isn't a novelty anymore—it’s just how you get to work. Baidu’s autonomous driving arm, Apollo Go (known as Luobo Kuaipao in China), is arguably the most advanced robotaxi operation in the world right now, rivaling only Alphabet’s Waymo.

Here is the "meat" of the robotaxi business as of early 2026:

- Scale: They are operating in about 20 cities across China.

- Volume: In Q3 2025 alone, they provided 3.1 million fully driverless rides.

- The Breakeven Point: This is the big one. The operations in Wuhan have already hit "unit economic" breakeven. They aren't just burning cash anymore; they’ve proven the model can actually turn a profit.

And it’s going global. In January 2026, Dubai’s Roads and Transport Authority (RTA) issued Apollo Go its first fully driverless permit. They are setting up an operations center in Dubai Science Park and planning to deploy over 1,000 vehicles there. There's even talk of them hitting London and Germany later this year through a partnership with Lyft.

👉 See also: Cuanto son 100 dolares en quetzales: Why the Bank Rate Isn't What You Actually Get

The Financial Reality Check

Is everything perfect? No. Kinda far from it.

Baidu’s total revenue actually dipped about 7% year-over-year in late 2025, hitting roughly RMB 31.2 billion. The core advertising business—the stuff that pays the bills—is still feeling the weight of a shaky Chinese macroeconomy. Advertising revenue fell 18% in the last reported quarter because companies are simply spending less.

But the "AI Cloud" is picking up the slack. Revenue there grew 33%, driven by massive demand for AI infrastructure. Companies in China can’t easily get Nvidia’s top-tier chips due to export bans, so they are turning to Baidu’s Kunlun chips. In 2025, Baidu scored major orders from giants like China Merchants Bank and China Mobile.

Basically, you’re looking at a company in a painful transition. It’s like watching a caterpillar turn into a butterfly, but the caterpillar part of the body is still dragging on the ground a bit.

Key Metrics for 9888.HK (January 2026)

- Current Price: ~HK$146.20

- Market Cap: ~HK$402 Billion

- P/E Ratio (TTM): Around 43x (reflecting high growth expectations for AI)

- Cash Position: They are sitting on a massive pile of net cash—roughly HK$50 per share. That’s about 35-40% of the entire stock price just sitting in the bank.

What Most People Get Wrong About 9888.HK

A lot of retail traders think Baidu is just a "China play." They buy it when the Hang Seng Index goes up and sell it when it goes down. That’s a mistake.

Baidu is increasingly becoming a decoupled AI play. While the broader Hong Kong market has been volatile, Baidu has shown it can move on its own merits, especially when it announces new AI milestones or robotaxi expansions.

✨ Don't miss: Dealing With the IRS San Diego CA Office Without Losing Your Mind

The biggest risk isn't actually the technology. It’s the regulation and the "spin-off" factor. On January 2, 2026, Baidu announced plans to spin off its Kunlunxin chip business. While this unlocks value, it also means the "core" Baidu stock might lose some of its hardware shine.

Also, the competition is brutal. You’ve got Pony.ai and WeRide nipping at their heels in the robotaxi space, and Alibaba is dumping billions into its own large language models. Baidu has the first-mover advantage, but in tech, that can evaporate in a weekend.

Actionable Insights for Investors

If you're looking at bidu hong kong stock, you've got to stop thinking about it as a search engine. It’s a robotics and infrastructure company now.

- Watch the HK$148 Resistance: The stock has struggled to stay above this level. If it breaks out convincingly, analysts like those at DBS Bank see a path toward HK$175 based on a "Sum of the Parts" valuation.

- Monitor the "AI Revenue Mix": The magic number is 50%. Once more than half of Baidu’s revenue comes from non-advertising sources (Cloud, AI, Robotaxis), the market will likely re-rate the stock from a "slow-growth media" company to a "high-growth tech" company.

- Mind the Geopolitics: Since Baidu is listed in both New York (BIDU) and Hong Kong (9888.HK), any friction between the US and China over AI chips will cause immediate ripples.

The bottom line? Baidu isn't the "safe" legacy play it used to be. It’s a high-stakes bet on the future of autonomy. If you believe that cars will eventually drive themselves and that AI will replace the search bar, the current valuation actually looks somewhat cheap, especially considering that nearly 40% of the price is backed by cold, hard cash.

But keep your eyes on those quarterly earnings. If the advertising business keeps shrinking faster than the AI business can grow, it's going to be a bumpy ride.

Next Steps for Tracking Baidu:

Check the next earnings report scheduled for February 18, 2026. This will be the definitive look at how ERNIE 5.0 performed during the peak Q4 holiday season and whether the robotaxi "breakeven" in Wuhan is translating to other cities like Foshan or Dongguan. Additionally, track the progress of the Kunlunxin spin-off, as the valuation of that separate entity will directly impact Baidu's balance sheet.