You're standing in front of your mailbox, and there it is: another "important notice" about your healthcare. Honestly, trying to figure out the average monthly cost of medicare supplemental insurance feels like trying to solve a Rubik's Cube in the dark.

Prices jump. Rules change.

One neighbor says they pay $90 a month, while another swears they’re shelling out $300 for the exact same coverage. It’s enough to make anyone want to just stick their head in the sand. But here’s the thing: those premiums aren't just random numbers pulled out of a hat. They follow a logic—sorta—and knowing that logic can save you thousands over the next decade.

The 2026 price tag: What’s the ballpark?

If you're looking for a quick answer, most people in 2026 are seeing monthly premiums fall between $120 and $240 for the most popular plans.

Specifically, if you're 65 and just signing up, the national average for the gold-standard Plan G is hovering around $189 per month. If you’re a bit older, say 75, that average climbs closer to $238.

But averages are tricky. They’re like saying the average temperature in the United States is 55 degrees—it doesn't help you much if you're shivering in Maine or sweating in Miami.

Why the massive range?

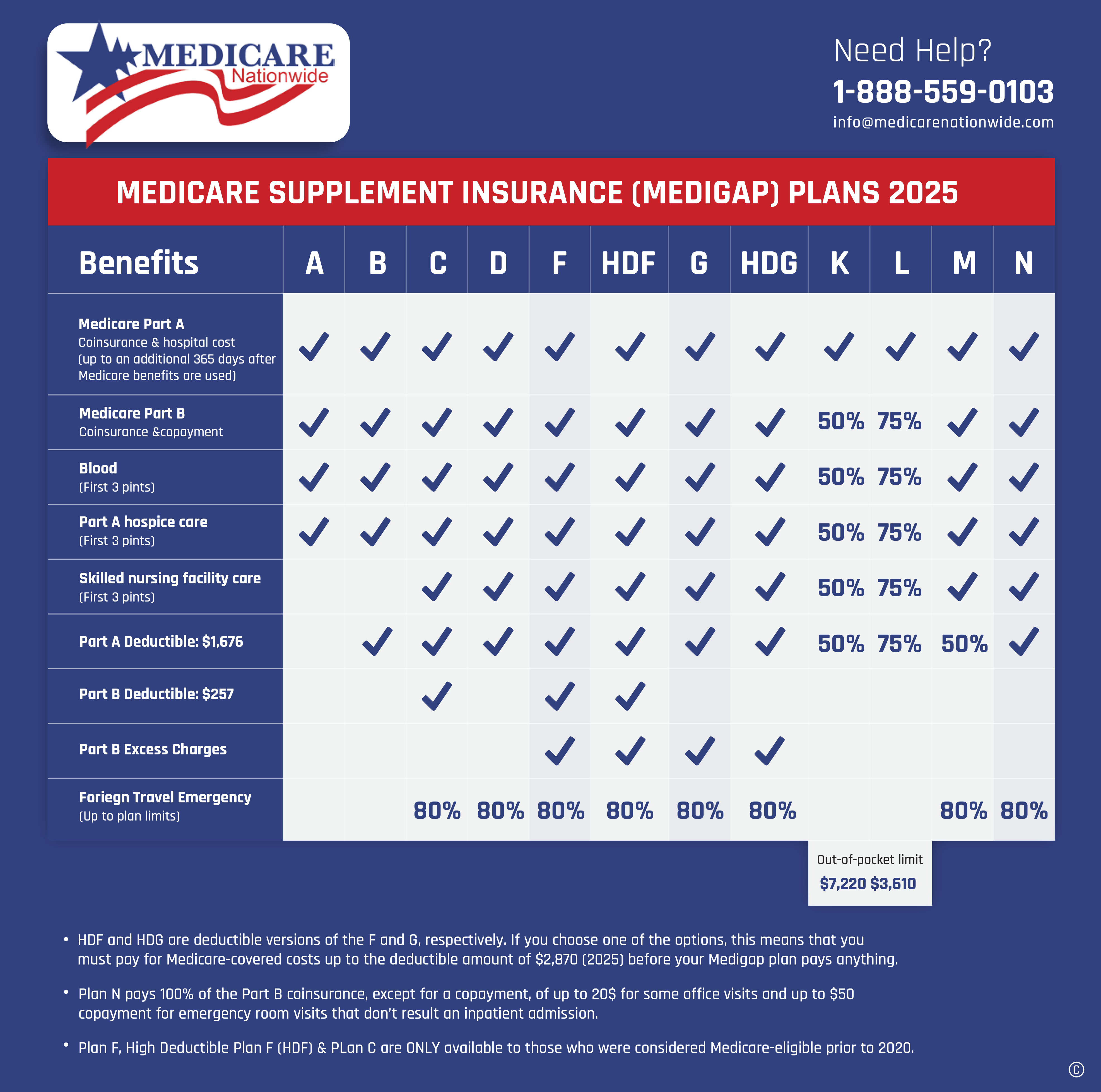

Medicare Supplement (Medigap) plans are standardized by the government. This means a Plan G from Company A has the exact same benefits as a Plan G from Company B. They both cover your Part A coinsurance, your hospital costs, and that pesky 20% that Part B doesn't touch.

Yet, Company A might charge you $150 while Company B wants $220.

📖 Related: The Human Heart: Why We Get So Much Wrong About How It Works

Why? Because they can. They’re private companies. They have different overhead, different "risk pools" (the health of the other people they insure), and different marketing budgets. You’re basically paying for the brand name and the customer service, not the actual medical coverage.

Breaking down the costs by plan type

Not all plans are created equal. If you want the "Cadillac" of plans, you'll pay for it. If you're okay with a "Toyota" plan that has a few more out-of-pocket costs, you can get a serious discount.

Plan G: The Crowd Favorite

This is the big one. Since Plan F was phased out for new enrollees back in 2020, Plan G has become the go-to. It covers everything except the Part B deductible. In 2026, that deductible is $283.

- Typical 2026 Cost: $140 – $220 per month.

Plan N: The Budget-Friendly Alternative

Plan N is great if you don't mind a few "hoops." You’ll pay a small copay (up to $20) for doctor visits and up to $50 for the ER. It also doesn't cover "excess charges," though those are actually pretty rare these days.

- Typical 2026 Cost: $110 – $180 per month.

High-Deductible Plan G: The "In Case of Emergency" Choice

This is for the gamblers—or the very healthy. You pay a tiny monthly premium, but you have to pay the first $2,950 of your medical bills yourself before the plan kicks in.

- Typical 2026 Cost: $45 – $85 per month.

The "Where You Live" Factor

Your ZIP code is probably the biggest factor in your average monthly cost of medicare supplemental insurance that you can't actually change (unless you're ready to pack your bags).

Take Florida. It’s notoriously expensive. A 65-year-old in the Sunshine State might see Plan G quotes starting at $213. Meanwhile, that same person in North Carolina or Iowa might find a plan for $123 or $126.

👉 See also: Ankle Stretches for Runners: What Most People Get Wrong About Mobility

States like New York and Connecticut have "community rating" laws. This sounds good—it means they can't charge you more just because you're older—but it often results in higher baseline premiums for everyone. In New York, it’s not uncommon to see Plan G rates north of $350 because the insurance companies are hedging their bets against an aging population.

Age is more than just a number

Most Medigap plans use "attained-age" rating. This is the one that bites you later.

Basically, the premium is based on how old you are right now. So, every time you have a birthday, your premium goes up a little bit. It starts cheap at 65 but can get heavy by the time you're 85.

Some companies use "issue-age" rating. Your price is based on how old you were when you first bought the policy. These start more expensive but don't go up just because you got older (though they still go up for inflation). If you plan on staying in the same house for 20 years, an issue-age plan is almost always the better deal long-term.

Tobacco, Gender, and the "Fine Print"

It’s annoying, but it’s true: being a man usually costs more. Men generally have higher healthcare costs in their later years, so insurers tack on a few extra dollars.

And if you smoke? Prepare to pay a "tobacco surtax." We’re talking a 10% to 30% markup on your monthly bill.

Then there are the discounts. Many companies offer a "household discount" if two people in the same house have policies with them. This can shave 5% to 12% off your bill. It’s one of those things people forget to ask about, but it's basically free money.

✨ Don't miss: Can DayQuil Be Taken At Night: What Happens If You Skip NyQuil

The 2026 Part B Reality Check

Don't forget that your Medigap premium is on top of your Medicare Part B premium. In 2026, the standard Part B premium is $202.90.

So, if you buy a Plan G for $190, your total monthly "subscription" for healthcare is actually **$392.90**.

How to actually get the lowest price

The "Open Enrollment Period" is your one-shot deal. It starts the month you turn 65 and are enrolled in Part B. For six months, insurance companies must sell you any plan they offer at the best available rate, regardless of your health.

If you miss this window and try to switch later, they can "underwrite" you. That’s insurance-speak for "we’re going to look at your medical records and either charge you double or reject you entirely."

Here is how you actually win the Medigap game:

- Ignore the Brand: Don't just go with the company that has the best commercials. Remember, the benefits are identical by law.

- Look at the Rate Increase History: Ask for a 5-year history of their premium hikes. A company that starts at $130 but raises rates 10% every year is worse than a company that starts at $150 and raises them 2% annually.

- Check for "Hidden" Copays: If you go with Plan N to save money, make sure you're actually okay with paying $20 every time you see a specialist. If you go three times a month, you've already lost your savings.

- Shop Local: Use a broker who has access to "regional" carriers. Sometimes the smaller, state-specific companies have much better rates than the national giants.

Actionable Steps for Your Search

Start by getting at least three quotes from different carriers for the exact same plan letter—usually Plan G or Plan N. Make sure you ask specifically if the pricing is attained-age, issue-age, or community-rated, as this tells you how much your bill will grow in five years. Finally, check if you qualify for a household discount; even if your spouse isn't on Medicare yet, some companies give you the discount just for living together.