You’ve probably seen the headlines. Some government report drops, claiming the average household income us is climbing, yet you’re staring at a grocery receipt for three bags of food that cost $140. It’s a weird disconnect. Honestly, looking at "average" numbers in a country as massive as the United States is a bit like trying to describe the weather for the entire continent with one temperature. It's technically a number, but it doesn't tell you if you need a parka or a swimsuit.

The latest data from the U.S. Census Bureau and the Bureau of Labor Statistics shows a fascinating, albeit frustrating, tug-of-war between rising wages and the stubborn ghost of inflation. As of early 2026, the national narrative is one of "stability," but that stability feels very different depending on whether you’re renting in San Francisco or owning a home in rural Ohio.

The Big Number vs. The Real Number

First, let's get the terminology straight because this is where most people get tripped up. When we talk about the average household income us, we're often actually looking for the median.

The "average" (mean) is usually much higher—somewhere north of $110,000—because billionaires like Jeff Bezos and Elon Musk pull the statistical rug upward. The median is the "middle" house. If you lined up every household in America by income, the one right in the center is the median.

According to the most recent Census reports released in late 2025, the real median household income in the U.S. sits at approximately $83,730.

That sounds decent, right? But here’s the kicker: after adjusting for inflation, that number is basically flat compared to where we were in 2023. We are running faster just to stay in the same place. In 2024, the median was around $81,600. So while the dollar amount went up, your ability to buy a carton of eggs or a gallon of gas didn't necessarily improve.

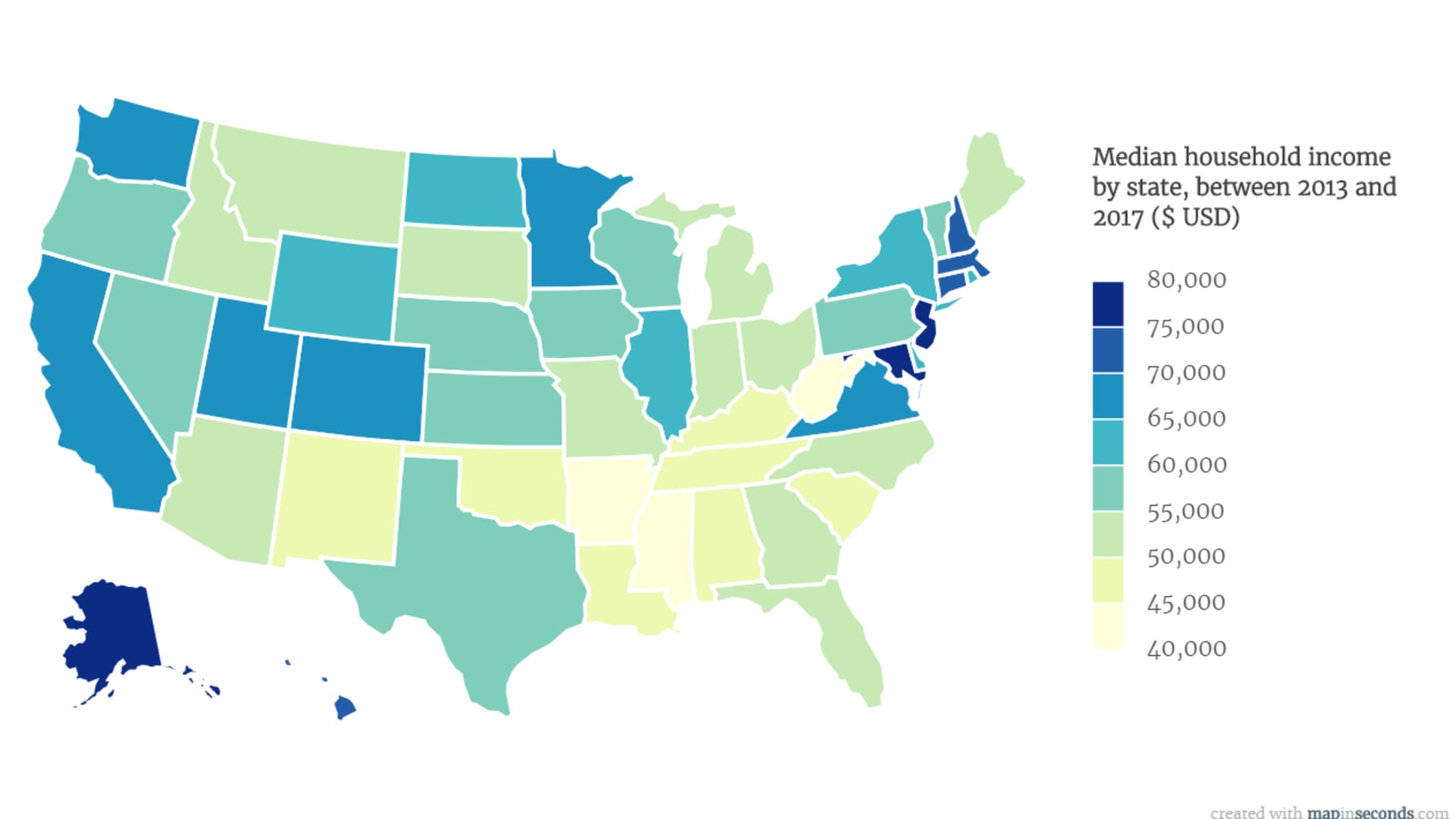

Why Your ZIP Code Is Your Financial Destiny

If you live in Massachusetts, you're likely seeing a median household income crossing the $104,000 mark. Meanwhile, if you’re in Mississippi, that number drops down toward $59,000. That is a massive chasm.

It’s not just about the paycheck, though. It’s the "cost of existing." A hundred grand in Boston doesn't buy the same life that sixty grand buys in Biloxi. This is why national averages feel like a lie to so many people.

High-Income Strongholds

- Maryland and New Jersey: Consistently hover near or above the $100k line due to proximity to DC and NYC.

- California: High wages, but the "sunshine tax" (housing) eats a huge chunk of that median $100,149.

- Utah and Colorado: These have become the "middle-of-the-country" powerhouses, with median incomes surging past $96,000 as tech hubs migrate inland.

Where the Struggle is Visible

The South still lags behind. West Virginia, Arkansas, and Louisiana all struggle with median incomes below $65,000. When you factor in that grocery costs in 2025 rose by about 6% nationally, those lower-income brackets are feeling a squeeze that the "average" data simply doesn't capture.

The Education Premium (and the Debt Trap)

We’ve been told for decades that a degree is the ticket to the middle class. The data still backs this up, but the "premium" is getting complicated.

If the head of the household has a Bachelor's degree or higher, the median income jumps significantly—often double what a household with only a high school diploma earns. In 2025, full-time workers with a degree saw median weekly earnings of roughly $1,747. Compare that to $980 for high school grads.

But here is the nuance: debt. A household earning $120,000 but paying $2,000 a month in student loans is effectively living a $80,000 life. The "average" doesn't subtract the debt, which is why a lot of "high-income" Millennials and Gen Z-ers feel broke.

The Racial and Gender Gap: Still There, Still Messy

Honestly, it's 2026 and the gaps aren't closing as fast as anyone hoped. Asian households continue to lead the pack with a median income well over $108,000. Non-Hispanic White households follow around $92,500.

The real concern is for Black and Hispanic households. While Hispanic median income saw a nice 5.5% bump recently—hitting about $70,950—Black household income actually dipped slightly in real terms to around $56,020.

And the "pink tax" on wages? Women are still earning about 81 to 82 cents for every dollar a man makes. In 2024 and 2025, this ratio actually slipped backward a bit for the first time in years. It's a reminder that "progress" isn't a straight line.

✨ Don't miss: Arvind Mills Stock Price: Why 2026 Could Be a Turning Point

What Most People Get Wrong About "Middle Class"

Pew Research defines the middle class as two-thirds to double the median income. By that math, if you're a three-person household, "middle class" is roughly $56,000 to $170,000.

That is a huge range! Someone making $60k feels very different than someone making $160k. Yet, they both get lumped into the same political talking points.

One thing that really stands out in the 2024-2025 data is the "vibe-cession." Even though incomes are technically up, about 60% of adults say their financial situation feels worse because of price increases. It's a psychological weight. When your "average household income us" goes up by 4% but your rent goes up by 10%, you aren't winning. You're losing slowly.

Actionable Steps: Navigating the Numbers

Knowing the average is fine for trivia, but it doesn't pay the bills. If you're trying to figure out where you stand or how to move the needle, here’s how to use this data:

- Benchmarking: Don't compare yourself to the national average. Look at your specific Metropolitan Statistical Area (MSA). The Census Bureau’s "QuickFacts" tool is the best way to see what people in your city actually make.

- The 20% Rule: Since many high-income states saw a 20% gap above the national median, if you're moving for a "higher" salary, ensure the bump is at least 25% to account for the cost-of-living shift in those hubs.

- Watch the "Real Wage": When you get a raise, subtract the current inflation rate (which was around 2.5-3% heading into 2026). If your raise was 3% and inflation was 3%, you didn't get a raise. You got a cost-of-living adjustment. Use that realization to negotiate harder or look for a pivot.

- Diversify Beyond the W-2: The households in the top 20% (earning over $150k) almost always have multiple income streams—investments, side businesses, or rental income. The "average" person relies on one paycheck; the "above-average" household usually has three.

The average household income us is a benchmark, not a boundary. The economy of 2026 is increasingly fragmented, rewarding those who specialize or live in high-growth regions, while making it harder for those in traditional roles to keep up with the cost of a basic American life.

🔗 Read more: Income tax calculator nj: Why your paycheck feels lighter than you expected

Next Steps for Your Finances:

Start by calculating your "Real Income" change over the last 24 months. Total your household income from 2023 and compare it to your 2025 year-end totals. If the growth isn't at least 8-10% total, you've effectively lost purchasing power. This is your cue to either audit your recurring expenses or begin looking at skill-upgrading paths that align with high-growth sectors like healthcare technology or renewable energy infrastructure, which are currently outpacing the national median wage growth.