Honestly, if you ask three different people what a "good" income looks like in America today, you’re going to get three wildly different answers. One person might say $60,000 is plenty if you’re living in rural Ohio, while someone in San Francisco would tell you that $150,000 feels like poverty. But what does the actual data say?

As we move through 2026, the noise around "the average" has never been louder. Politicians use one number, your neighbor uses another, and your bank account likely has its own opinion. If you’re trying to figure out where you stand, you’ve got to look past the surface-level headlines.

The average household income in the united states is a tricky beast because of how the math works. When you take the total income of everyone—from the billionaire in a penthouse to the student working part-time—and divide it by the number of households, the "mean" or average gets pulled way up. In 2025, that average sat around $121,000.

But wait.

Does the "average" American family actually bring home six figures? Not even close.

The Median vs. Average Trap

Basically, the "mean" average is a bit of a liar. If Elon Musk walks into a dive bar, the average person in that bar is suddenly a billionaire, even if everyone else is broke. This is why economists prefer the median.

The median is the true middle. It’s the point where exactly half of the country makes more and half makes less. According to the most recent Census Bureau and Federal Reserve data for 2024 and 2025, the median household income is roughly $83,730.

That’s a massive $37,000 gap between the "average" and the "middle."

💡 You might also like: Replacement Walk In Cooler Doors: What Most People Get Wrong About Efficiency

Why the Gap Matters

This discrepancy exists because the top 1% and 5% of earners have seen their incomes skyrocket while the middle class has mostly just... hovered. In 2025, the top 1% of households pulled in an average of $659,060. When you factor those massive numbers in, it drags the national average up, making the economy look "richer" on paper than it feels in the grocery store checkout line.

What’s Changing in 2026?

We’re currently navigating what some experts, like those at U.S. Bank, call a "K-shaped" economy. It’s a weird vibe. Some sectors are thriving thanks to AI-driven productivity gains, while others are feeling the squeeze of the "One Big Beautiful Bill Act" (OBBBA) changes that shifted social safety nets and tax credits earlier this year.

Inflation has cooled significantly compared to the 2022-2023 spike, but it's not gone. In early 2026, we're seeing headline inflation hover around 2.9%. This means that even if your nominal income—the number on your paycheck—went up by 3%, you're effectively just breaking even. You aren't "richer"; your money just buys the same amount of eggs and gas it did last year.

- Real Wages: When adjusted for inflation, many Americans are finding that their "real" income hasn't moved much since 2019.

- The 80-Hour Rule: New Medicaid and SNAP work requirements enacted in 2025 mean that for many lower-income households, maintaining "income" now requires a strict 80-hour-per-month work floor, which has shifted the labor participation of the bottom 20%.

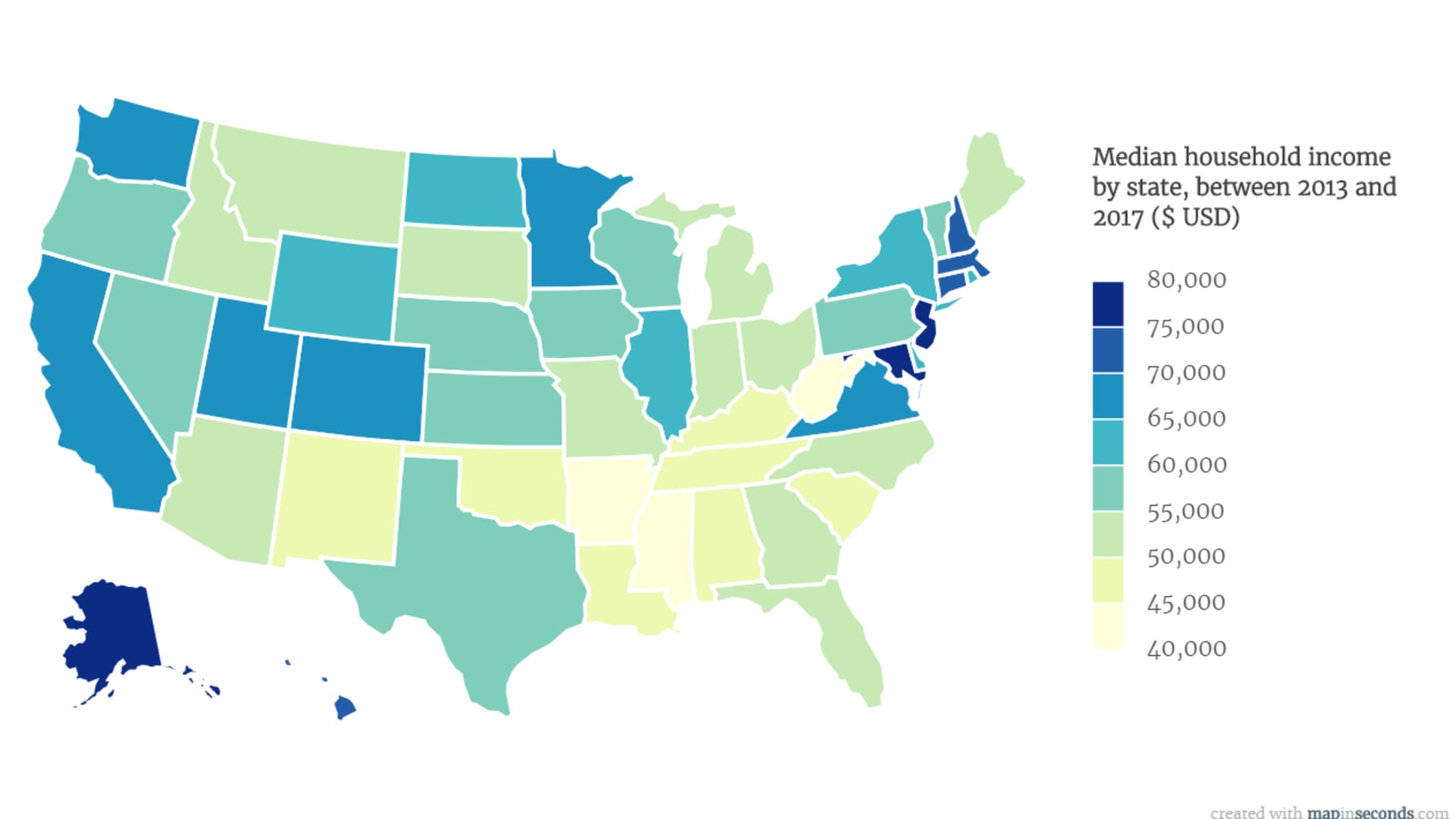

Geography is Destiny (Sorta)

You can't talk about the average household income in the united states without talking about where people actually live. A dollar in Mississippi just isn't a dollar in Massachusetts.

Take a look at how the median income shifts across the map:

- Maryland & DC: Consistently at the top. Maryland’s median often clears $101,000, largely due to the concentration of high-paying federal jobs and tech hubs.

- The Coastal Giants: New Jersey, Massachusetts, and Washington state are all members of the $90k+ club.

- The Deep South: Mississippi remains the lowest-income state, with a median often hovering near $54,000.

This creates a massive disparity. If you earn $80,000 in West Virginia, you are living like a king. If you earn $80,000 in New York City, you're probably looking for a roommate.

The "Comfortable" Income

A 2025 SmartAsset study highlighted that to live "comfortably" (defined as the 50/30/20 rule: 50% for needs, 30% for wants, 20% for savings), a single adult in Hawaii needs to pull in over $124,000. Meanwhile, a family of four in Massachusetts might need upwards of $313,000 to hit that same "comfort" level.

📖 Related: Share Market Today Closed: Why the Benchmarks Slipped and What You Should Do Now

Education and the Income Ceiling

It’s an old trope, but the data still backs it up: your degree (or lack thereof) is the biggest predictor of which side of the "average" you fall on.

Recent BLS data shows:

- Advanced Degree: Median of ~$102,000/year.

- Bachelor’s Degree: Median of ~$83,000/year.

- High School Diploma: Median of ~$49,500/year.

There’s a clear "education premium," but it's getting more complicated. With the rise of specialized trades and the cooling of the "everyone needs a four-year degree" sentiment, we’re seeing vocational income—electricians, plumbers, specialized HVAC techs—start to outpace entry-level white-collar roles in many regions.

The Gender and Race Gap in 2026

We have to be honest here—the numbers aren't equal across the board. The gender pay gap has actually seen a slight widening recently. In 2024 and 2025, women earned about 81% of what men earned. Specifically, the median for men was roughly $71,090, while for women it was $57,520.

Race also plays a massive role. Hispanic households saw a significant jump in real income recently (up about 4.3%), but Black households have faced a 3.3% decline in the same period. This highlights the "uneven" nature of the current recovery.

Surprising Details You Won't See on the News

Did you know that the "National Average Wage Index" used by the Social Security Administration for 2024 is $69,846?

This is the number they use to calculate your future benefits. It’s different from the "household" income because it only looks at individuals. It's a useful benchmark if you’re trying to see how your personal salary stacks up against the rest of the workforce, rather than combining your earnings with a spouse or partner.

👉 See also: Where Did Dow Close Today: Why the Market is Stalling Near 50,000

Another weird thing? The "top 5%" in places like New York earn an average of $575,505, while the bottom 20% in that same state earn just $13,647. That is one of the highest wealth disparities in the country. It’s why New York feels like two different planets existing in the same five boroughs.

Actionable Steps: What to Do With This Info

Knowing the average household income in the united states is interesting, but it doesn't pay your bills. Here is how you should actually use this data to your advantage.

Benchmark Your Location

Stop comparing yourself to people on Instagram. Use the Department of Justice’s "Median Income Tables" for your specific state and family size. This gives you a realistic view of what "middle class" actually looks like where you live.

Calculate Your "Real" Raise

If you get a 4% raise this year, but the cost of your specific "basket of goods" (rent, groceries, utilities) went up by 5%, you actually took a 1% pay cut. Track your personal inflation rate to know when it’s time to negotiate for a higher salary or look for a new role.

Diversify Beyond the Salary

The gap between the "average" (mean) and the "middle" (median) is largely driven by asset ownership—stocks, real estate, and business equity. Most people at the top aren't just earning a high salary; they own things that appreciate. If you're stuck near the median, the goal should be moving some portion of your income into assets to bridge that gap.

Stay Ahead of the K-Curve

With the labor market tightening and immigration flows changing, "healthy" job growth numbers look different than they used to. If you are in a sector being disrupted by AI or policy shifts, now is the time to pivot toward "high-moat" skills—things that require human judgment, complex physical movement, or high-level emotional intelligence.

The "average" is just a number. Your goal is to make sure your specific household has the resilience to handle whatever the 2026 economy throws at it.