If you’ve spent any time looking at your CommSec account lately, you’ve probably noticed the asx commbank share price is doing something it hasn't done in a while. It’s making people nervous. Honestly, for years, CBA was the "bulletproof" stock of the ASX. You bought it, you tucked it away, and you collected those juicy franked dividends while the capital value slowly marched upward. But as we sit here in mid-January 2026, the vibe has shifted. The stock is currently trading around $154.08, down about 4% since the start of the year.

Some analysts are calling it a "valuation reset." Others, like the team at Morgans, are being way more dramatic, putting out price targets as low as $96.07. That’s a massive gap. When you have one group of experts saying the bank is a pillar of stability and another saying it could crater by 30%, it’s hard to know who to believe. Basically, the market is having a massive argument with itself over whether CBA is actually worth its premium.

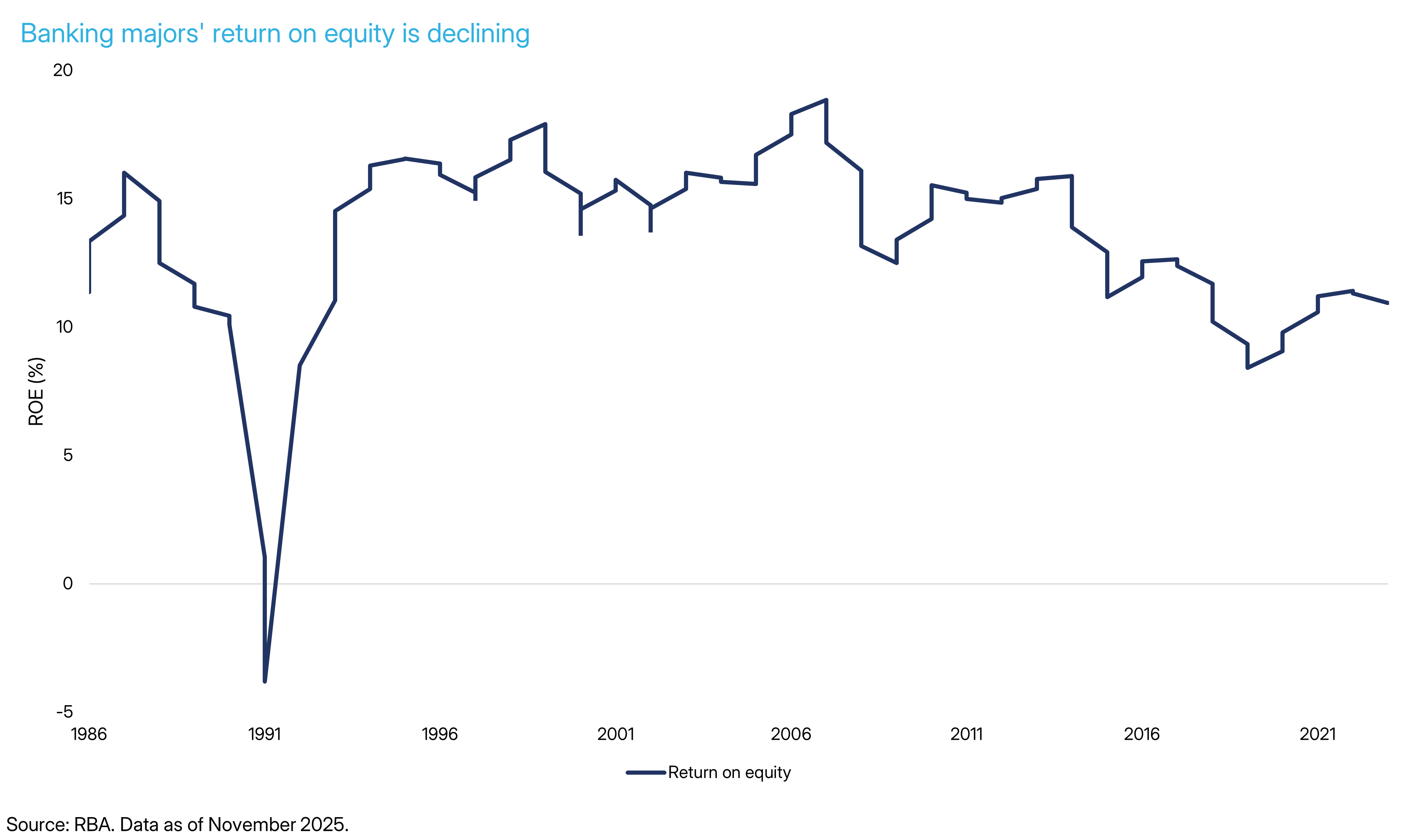

The Reality of the ASX Commbank Share Price Today

The thing about CBA is that it’s always expensive. It trades at a massive premium to peers like Westpac or ANZ—sometimes as much as 45% higher on a price-to-earnings (P/E) basis. Right now, that P/E is sitting around 25.46x. For a bank, that is genuinely astronomical. Most global banks trade at half that.

🔗 Read more: African Rand to US Dollar: What Most People Get Wrong

Why do we pay it? Because CBA is a tech company that happens to have a banking license. Their app is better. Their data is better. Their proprietary home loan growth—meaning loans they write themselves without paying a middleman broker—hit 68% recently. That is a huge structural advantage. But even a great company can be a bad investment if you pay too much for it.

What’s actually dragging the price down?

- The "Interest Rate Cliff" that never ended: Back in 2025, everyone thought the RBA would be cutting rates by now. Instead, the cash rate is stuck at 3.6%, and some economists from Citi and Macquarie are actually predicting hikes in February and May 2026.

- Shrinking Margins: When rates stay high, you’d think banks make more money. Kinda. But customers are getting smarter. They are moving money out of 0% transaction accounts and into high-interest savers. That’s called "deposit switching," and it’s eating into CBA’s Net Interest Margin (NIM).

- Inflationary Creep: IT costs and wage inflation are up. CBA's operating expenses jumped 4% in their last quarterly update.

Why the Dividend Still Matters (Even if the Yield is Low)

If you're looking for a 6% or 7% yield, you aren't looking at CBA. At the current asx commbank share price, the yield is roughly 3.15%. That looks measly compared to some of the smaller miners or even Westpac. However, you've got to look at the franking. Because CBA pays 100% franked dividends, that 3.15% is actually closer to 4.5% for most taxpayers once you claim the credits back.

Last year, the bank paid out $4.85 per share in total. If you bought in years ago at $90 or $100, your "yield on cost" is fantastic. This is why the big institutional funds rarely sell. They don't care about the daily price swings as much as the reliable, tax-effective income stream.

The 2026 Outlook: Is a Crash Actually Likely?

Let’s talk about that $96 price target. It sounds terrifying. To get there, the asx commbank share price would need to fall another 35% or so. For that to happen, we’d likely need a "perfect storm."

✨ Don't miss: Stock Exchange Closing Today: Why the S\&P 500 Just Snapped Its Losing Streak

Imagine this: inflation stays sticky, the RBA hikes rates twice more, and suddenly those "resilient" Aussie households start defaulting on mortgages in record numbers. If arrears (late payments) spike significantly from their current low levels, the market will re-rate CBA instantly. We saw a hint of this in January 2026 when the stock dropped on news of a "mild earnings miss." The market is "priced for perfection," which means any tiny mistake gets punished.

But honestly? CBA is a fortress. Their Common Equity Tier 1 (CET1) capital ratio is 11.8%. That’s a fancy way of saying they have a mountain of cash sitting in the basement to survive a rainy day. They aren't going broke. The question is just whether the shares should be worth $150 or $120.

💡 You might also like: What Really Happened With the Trump and Powell Video

Major Risks to Watch

- BHP vs CBA: There is a literal battle for the "King of the ASX" title right now. As iron ore prices fluctuate, BHP is nipping at CBA's heels for the spot of the largest company by market cap.

- The 3-Month Trend: Technical analysts at places like StockInvest.us are currently flagging "sell" signals because the stock is trading below its short-term and long-term moving averages.

- Competition: Macquarie Group is aggressively hunting for CBA’s home loan customers. They are fast, digital-first, and they don't have the "big bank" baggage.

Tactical Moves for Investors

If you already own CBA, selling now might be a mistake because of Capital Gains Tax (CGT). If you bought at $110 and sell at $154, you’re handing a chunk of that profit to the ATO. For many, holding for the dividends is the "least worst" option.

If you’re looking to buy, it might pay to be patient. We are seeing a "falling wedge" pattern in the charts. Waiting for a support level around $140 could provide a much better margin of safety than jumping in today.

Actionable Next Steps:

- Check your portfolio weighting; if CBA is more than 10-15% of your total wealth, you are heavily exposed to the Australian housing market.

- Monitor the RBA's February meeting minutes; any talk of "tightening" will likely send the share price lower in the short term.

- Review the February half-year results (due soon) specifically for the "Net Interest Margin" figure—if that's falling faster than 2-3 basis points, the sell-off may continue.