Tax season is usually a headache, but it gets way worse when you start staring at your health insurance bills and wondering if Uncle Sam is going to give you a break. You’ve likely heard a dozen different things from friends or that one "expert" coworker. Some say everything is deductible. Others say nothing is.

The truth? It’s complicated.

Basically, the answer to are health care premiums tax deductible depends entirely on how you get your insurance and how much you actually spent. It’s not a simple "yes" or "no" for everyone. For most W-2 employees, the answer is often a disappointing "no," but for the self-employed or those with massive medical bills, it's a massive "yes" that can save thousands.

The 7.5% Hurdle: Why Most People Can't Claim It

If you’re a standard employee and your boss takes the premium out of your paycheck, you’re probably already getting the tax benefit without realizing it. Most employer-sponsored plans are "pre-tax." This means the money is snatched away before the IRS even sees it. Since you never paid taxes on that money in the first place, you can’t deduct it again. That would be "double dipping," and the IRS hates that.

But let’s say you pay for your own plan with after-tax dollars. You might think you're in the clear to deduct every penny. Not so fast.

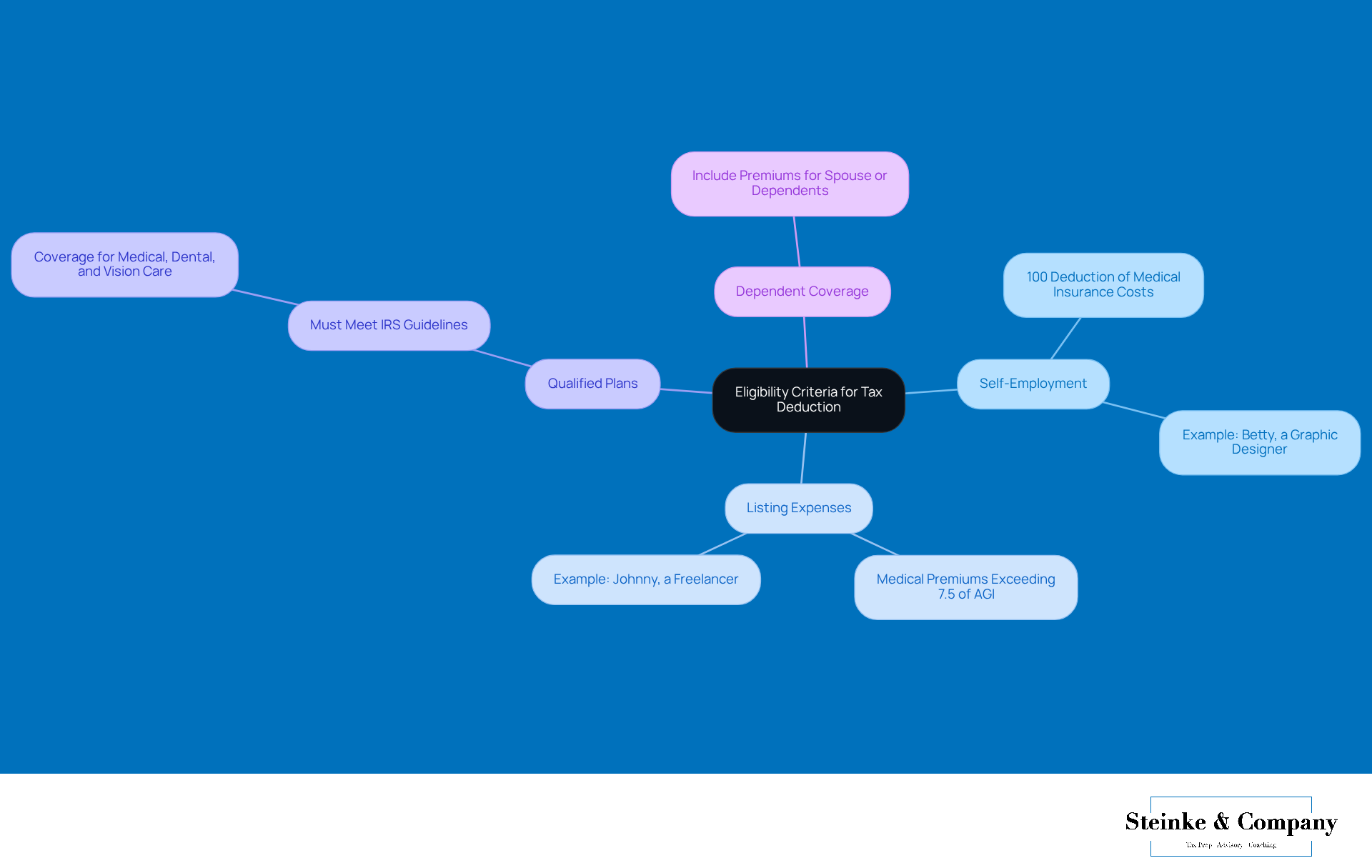

You have to itemize. Most people don't do that anymore because the standard deduction is so high these days. If you do itemize, you hit the 7.5% floor. This is the rule that kills the dream for most middle-class families. You can only deduct the part of your total medical expenses—including those premiums—that exceeds 7.5% of your Adjusted Gross Income (AGI).

Think about that for a second. If you make $100,000, the first $7,500 of your medical spending essentially doesn't exist to the IRS. You only start counting at dollar $7,501. It’s a high bar. Honestly, it's a hurdle designed to ensure only people with truly "catastrophic" or very high costs get the break.

The Self-Employed Loophole (The Good News)

Now, if you’re a freelancer, a contractor, or you run your own shop, things get much better. The self-employed health insurance deduction is one of the best perks of being your own boss.

Unlike the itemized mess mentioned above, this is an "above-the-line" deduction. You don't have to itemize. You don't have to hit a 7.5% threshold. You just subtract the premiums directly from your gross income on Schedule 1 of your Form 1040.

✨ Don't miss: Williams Sonoma Deer Park IL: What Most People Get Wrong About This Kitchen Icon

There are catches, of course. There are always catches.

- You can't claim the deduction if you were eligible for a plan through your spouse's job. It doesn't matter if you didn't take it; if you could have had it, the deduction vanishes.

- You can't deduct more than your business actually earned. If your business lost money this year, you can't use the health insurance deduction to create a bigger loss.

What About Medicare?

A lot of retirees get confused here. They see the Social Security check come in, notice the Medicare Part B premium is already gone, and assume it’s just a lost cost.

Actually, Medicare premiums are absolutely deductible medical expenses. This includes Part B, Part D (prescription drugs), and even Medicare Supplemental insurance (Medigap). If you’re self-employed and over 65, you can often use that same "above-the-line" deduction for these premiums.

Wait. There’s a catch for Part A. Most people get Part A for free because they worked long enough. If you have to pay for it voluntarily, you can deduct it. But you cannot deduct the 0.9% Medicare tax that was withheld from your wages back when you were working. That’s a tax, not a premium. Subtle difference, but the IRS is picky about words.

The Marketplace and Premium Tax Credits

If you bought your plan on the Health Insurance Marketplace (Obamacare), you might be getting a subsidy. This is the Premium Tax Credit.

If the government is already paying for half your premium through a credit, you definitely can't deduct that half. You can only deduct the part you paid out of your own pocket. If you try to claim the whole thing, you’re asking for an audit. Don't do that.

Are Long-Term Care Premiums Different?

Yes. Sorta.

The IRS views long-term care insurance (LTC) as a "qualified medical expense," but they put a cap on how much you can deduct based on your age. If you’re 40 or younger, you can only deduct a few hundred bucks. If you’re over 70, you can deduct thousands. These limits change every year to account for inflation, so you have to check the current IRS Publication 502 to see the exact number for the current tax year.

🔗 Read more: Finding the most affordable way to live when everything feels too expensive

It’s an age game. The older you get, the more the government encourages you to have this coverage by letting you write off more of it.

Common Mistakes and Weird Exclusions

People try to write off some wild stuff. I’ve seen people ask if they can deduct their gym membership because "it keeps them healthy and lowers their risk."

Nice try. No.

Generally, you can't deduct:

- Life insurance premiums (even though it's "insurance")

- Disability insurance premiums

- Non-prescription "wellness" supplements

- Cosmetic surgery (unless it’s to fix a deformity from a disease or injury)

- Health savings account (HSA) contributions if you already took the deduction for the contribution itself.

It’s all about the "why." If the expense is for the "diagnosis, cure, mitigation, treatment, or prevention of disease," it’s usually okay. If it’s just for "general health," like a Peloton subscription or organic kale, you’re out of luck.

Breaking Down the Math

Let’s look at a quick, messy example.

Imagine Sarah. She’s a freelancer. She makes $60,000 a year. She pays $500 a month for her own health insurance. That’s $6,000 a year.

Since she's self-employed, she takes that $6,000 right off the top. Her taxable income is now $54,000. She saves her marginal tax rate—let's say 22%—which is about $1,320 in cold, hard cash she doesn't have to send to the IRS.

💡 You might also like: Executive desk with drawers: Why your home office setup is probably failing you

Now imagine Dave. Dave is a W-2 employee at a big tech firm. He also pays $500 a month for insurance, but his company takes it out "pre-tax." On his W-2, his income is already $54,000. He doesn't get an extra deduction because he never "saw" that $6,000. He got the same tax break as Sarah, just through a different door.

Then there's Martha. She's retired, has no business income, and pays $10,000 a year in premiums and dental work. Her AGI is $50,000.

7.5% of $50,000 is $3,750.

Martha can deduct $6,250 ($10,000 minus $3,750), but only if all her itemized deductions (mortgage interest, etc.) add up to more than the standard deduction. If she’s a single filer, the standard deduction is likely higher than her total itemized list, so she gets zero extra benefit for her premiums.

It’s brutal.

How to Handle an Audit (Just in Case)

If you decide to claim these deductions, keep your receipts. Seriously. The IRS doesn't care about your bank statement saying "Insurance Payment." They want to see the policy declaration page. They want to see that the plan is "qualified."

If you’re self-employed, keep a record showing you weren't eligible for a spouse’s plan. This is the first thing they’ll check. A simple letter or a copy of your spouse's open enrollment guide showing you weren't on the list can save you a world of pain.

Final Action Steps for This Tax Year

Stop guessing and start organizing. Tax laws change, and while the 7.5% rule has been steady for a bit, the specific amounts for long-term care and self-employed limits shift annually.

- Check your W-2 or pay stubs. Look for "Section 125" or "Cafeteria Plan." If your premiums are there, they’re pre-tax. You’re done. You already got the break.

- Total your medical spending. If you spent a ton on surgery, dental work, or glasses this year, you might actually clear that 7.5% floor. Don't just look at premiums; look at everything.

- If you're self-employed, claim it on Schedule 1. Do not put it on Schedule C. Putting it on Schedule C is a common mistake that can mess up your self-employment tax calculations.

- Gather your 1095-A. If you’re on a Marketplace plan, you need this form to reconcile your credits. You cannot file correctly without it.

- Consult a pro if you're over 65. Medicare and Medigap deductions are a goldmine that many seniors leave on the table because they think "Social Security handles it."

Knowing whether are health care premiums tax deductible for your specific situation requires looking at your employment status first. Once you identify your "bucket"—W-2, self-employed, or retiree—the path becomes much clearer. Don't leave money on the table, but don't try to cheat the system with gym memberships either.