If you’ve ever sat at your kitchen table staring at a pile of bills and wondered why "the average American" seems to be doing better than you, there is a very good reason for that. Honestly, the "average" is a bit of a lie. When we talk about the American average income, we are usually mixing up two very different mathematical concepts: the mean and the median. It sounds like high school math, but it’s the difference between feeling stable and feeling broke.

Most people hear "average" and think of the mean. You take everyone's pay, add it up, and divide by the number of people. But in a country with billionaires like Elon Musk or Jeff Bezos, those massive numbers pull the average way up. It creates a distorted picture. As of early 2026, the average annual household income in the U.S. has climbed to roughly $121,000.

Wait. Does that sound right to you? For most of us, it doesn't.

That’s because the median—the actual middle point where half the country makes more and half makes less—is much lower. In late 2025, the U.S. Census Bureau and Bureau of Labor Statistics (BLS) data pointed to a median household income of about $83,730. That’s a nearly $40,000 gap between the "average" and the "typical" experience.

The American Average Income: Why Your Neighbor Probably Makes Less Than You Think

Kinda crazy, right? We’re living in a time where wage growth is finally, slowly, beating inflation. According to recent 2026 forecasts from groups like Mercer and Payscale, employers are budgeting for about a 3.5% pay increase this year. While that's not exactly a "buy a private island" kind of raise, it’s a steady climb after the chaos of the early 2020s.

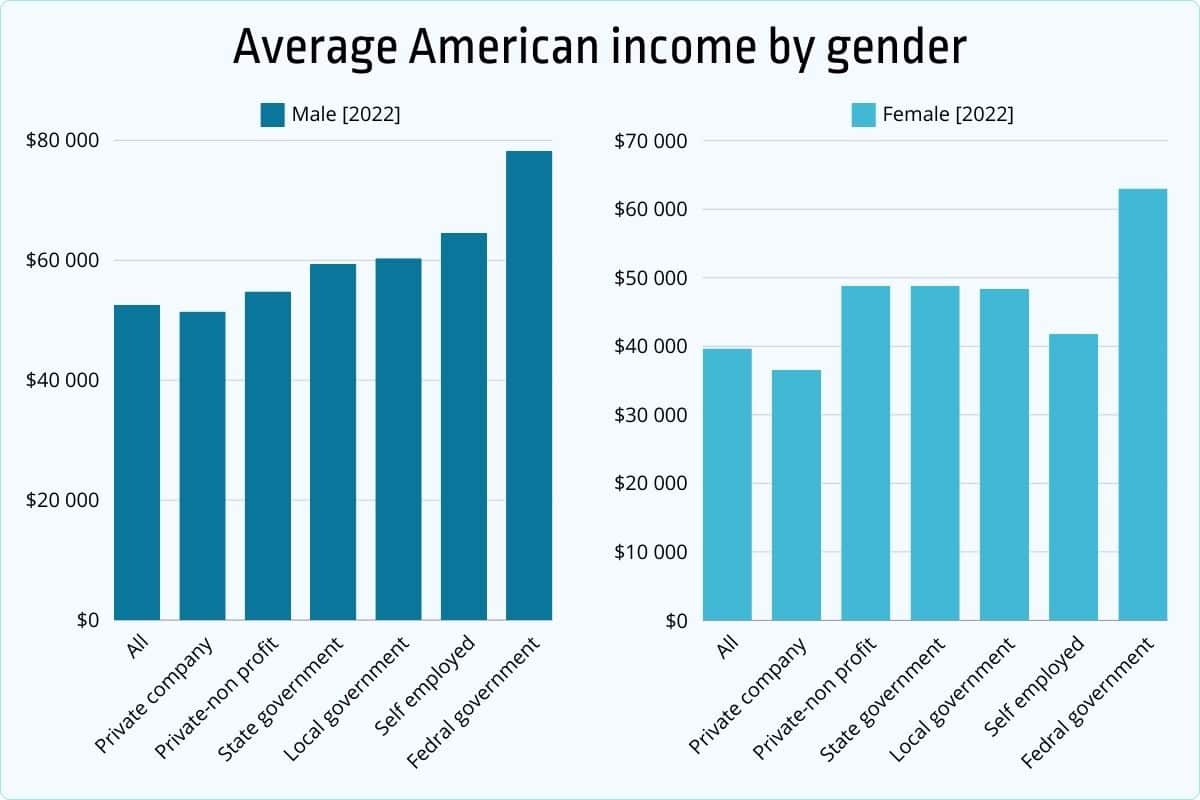

But those numbers change wildly depending on who you are and where you live. For instance, if you're a full-time worker, the BLS reported that the median weekly earnings hit $1,214 in the third quarter of 2025. Annualize that, and you're looking at about $63,128. But if you’re a woman, that number drops to about $1,076 a week, while men are bringing home $1,333.

👉 See also: MYR to US Dollar: What Most People Get Wrong About the Ringgit

The gap isn't just about gender. It’s about age, too.

You’ve probably noticed that your peak earning years don't happen when you're 22. Data shows that folks between 35 and 54 are the ones really carrying the load, with median weekly earnings hovering around $1,380. Meanwhile, the 16-to-24 crowd is scraping by on about $750 a week. It’s the "experience premium," basically.

Does Education Still Pay Off?

Short answer: Yeah, it does. But it’s getting more complicated.

The divide between someone with a high school diploma and a bachelor’s degree is now a canyon. A report from the Census Bureau highlighted that households headed by someone with a bachelor’s degree or higher earned a median of $132,700 in 2024—more than double the $58,410 earned by those with just a high school diploma.

- Professional Degree holders: Often clearing $1,900+ per week.

- Bachelor’s Degree holders: Averaging around $1,559 per week.

- High School graduates: Sitting closer to $960 per week.

It's not just the starting pay; it's the trajectory. Over the last twenty years, the "real" (inflation-adjusted) earnings for college grads rose about 6.3%, while high school grads only saw a 3.2% bump. When you account for the rising cost of eggs, gas, and rent, that 3.2% barely feels like moving at all.

Geography is Your Financial Destiny

Where you park your car at night matters just as much as what you do for a living. If you’re in Massachusetts or Washington state, the American average income looks great. Washington currently leads the pack with average weekly wages around $1,489.

On the flip side, Mississippi remains the lowest at $993 per week.

But there’s a catch.

You might make $120,000 in San Francisco, but after paying $4,000 for a one-bedroom apartment, you’re basically living like someone making $50,000 in Ohio. When you adjust for "Regional Price Parity"—which is just a fancy way of saying "what things actually cost where you live"—states like North Dakota and Minnesota suddenly look a lot more attractive. You make good money, and that money actually buys stuff.

What’s Actually Happening in 2026?

We are currently seeing a "cooling" of the labor market. The 2026 Cost-of-Living Adjustment (COLA) for Social Security was set at 2.8%, which gives us a hint of where the government thinks inflation is headed. It's lower than the massive jumps we saw in 2023, which is a bit of a relief, but it also means employers aren't feeling the same pressure to hand out 10% raises to keep people from quitting.

🔗 Read more: What Really Happened With the Trump China Tariff Cut

Most businesses are now being "strategic." They aren't giving everyone a flat 5% raise. Instead, they’re dumping money into "critical roles"—think AI specialists, maintenance technicians, and healthcare workers. If you’re in a "high-demand" field, your personal version of the American average income is likely much higher than the national stats.

Real-World Action Steps

Knowing the numbers is one thing, but using them is another. If you're looking at these stats and realizing you're on the wrong side of the median, here is how you actually move the needle:

- Audit Your Role: Don't just look at national averages. Use tools like the BLS Occupational Outlook Handbook to see if your specific job is growing. If you're in a "stagnant" field, no amount of hard work will fix a low ceiling.

- Negotiate with Real Data: Most people go into a salary review saying, "I work hard." Instead, go in saying, "The median weekly earnings for this role in this zip code have increased by 4.2% this year, and my performance metrics exceed the benchmark."

- Focus on "Real" Income: If you get a 3% raise but your rent goes up 10%, you didn't get a raise; you got a pay cut. Moving to a lower-cost area (if your job allows) is often the fastest way to increase your disposable income without changing your salary.

- Watch the COLA: If you’re a freelancer or a business owner, use the 2.8% to 3.5% benchmarks as your minimum price increase for 2026. If you aren't raising your rates by at least that much, you're losing money.

The American average income tells a story of a country that is growing, but unevenly. The middle is holding steady, but the "typical" experience is vastly different from the headlines. Whether you're in the $63,000 median or the $121,000 average, the goal is the same: making sure your "real" wages stay ahead of the world's prices.

To get a true sense of your standing, calculate your household's post-tax income and compare it against the $72,330 national post-tax median. If you are below that mark, focusing on skill acquisition in high-growth sectors like technology or specialized trades remains the most reliable path upward in the 2026 economy.