So, you’re looking at the Ally Financial stock price and wondering if the dip is a trap or a massive "buy" signal. Honestly, it’s a bit of both. As of January 16, 2026, Ally (ALLY) closed at $43.61. That’s a tiny nudge down—about 0.10% on the day—but if you zoom out, the story gets way more interesting.

The stock has been a bit of a rollercoaster lately. Just a week ago, it was flirting with $47.06. Now? It’s down roughly 4.6% over the last seven days. While a 5% drop might make some folks sweat, you've gotta remember where this thing started. A year ago, it was much lower. Three years ago? Way lower. We're talking a 54% gain over a three-year stretch. Not exactly "dead money."

But let's talk about the elephant in the room: the auto market.

The Ally Financial stock price and the used car "hangover"

Most people assume Ally is just a bank. Kinda. But really, they are the kings of auto lending. When the used car market went nuts a few years back, Ally was printing money. Now that things are "normalizing," the bears are coming out of the woodwork. They’re worried about delinquencies. They’re worried about people not paying back those $800-a-month truck loans.

Is the worry justified? Sorta.

✨ Don't miss: Funny Team Work Images: Why Your Office Slack Channel Is Obsessed With Them

Actually, the data shows Ally's retail auto loan portfolio is holding steady at about $83.9 billion. That’s a huge chunk of change. Analysts like the ones over at Wells Fargo have actually been turning more bullish lately. They recently upgraded the stock to Overweight with a price target of $52.00. Their logic? They expect "reserve releases" in 2026. Basically, that’s bank-speak for "we set aside too much money for bad loans, so now we get to count it as profit."

- Net Interest Margin (NIM) expansion: As interest rates (currently in the 3.5-3.75% range) potentially settle, Ally’s funding costs—what they pay you for your savings account—might finally stop eating their lunch.

- The Dividend: They’re still paying out $0.30 per quarter. That’s a 2.75% yield. It’s not a "get rich quick" dividend, but it's reliable.

- Valuation: The stock's P/E ratio is sitting around 25x, which looks high compared to the industry average of 9x. But wait. If you look at forward earnings, the math changes.

What the "smart money" is watching right now

If you’re tracking the Ally Financial stock price, you need to circle January 21, 2026 on your calendar. That’s the Q4 2025 earnings call.

The consensus EPS (earnings per share) forecast is $1.01. Last year, for the same quarter, they hit $0.78. If they beat that dollar mark, the stock could easily reclaim that $47 level. If they miss? Well, the 52-week low is **$29.52**, though we’re a long way from those dark days.

There’s also the "strategic pruning" factor. Ally hasn't just been sitting on its hands. They dumped their credit card business and stopped doing new mortgage originations. They are basically doubling down on what they do best: cars and digital banking. It’s a cleaner, leaner business model, but it makes them a "one-trick pony" in the eyes of some critics. If the auto market catches a cold, Ally gets the flu.

🔗 Read more: Mississippi Taxpayer Access Point: How to Use TAP Without the Headache

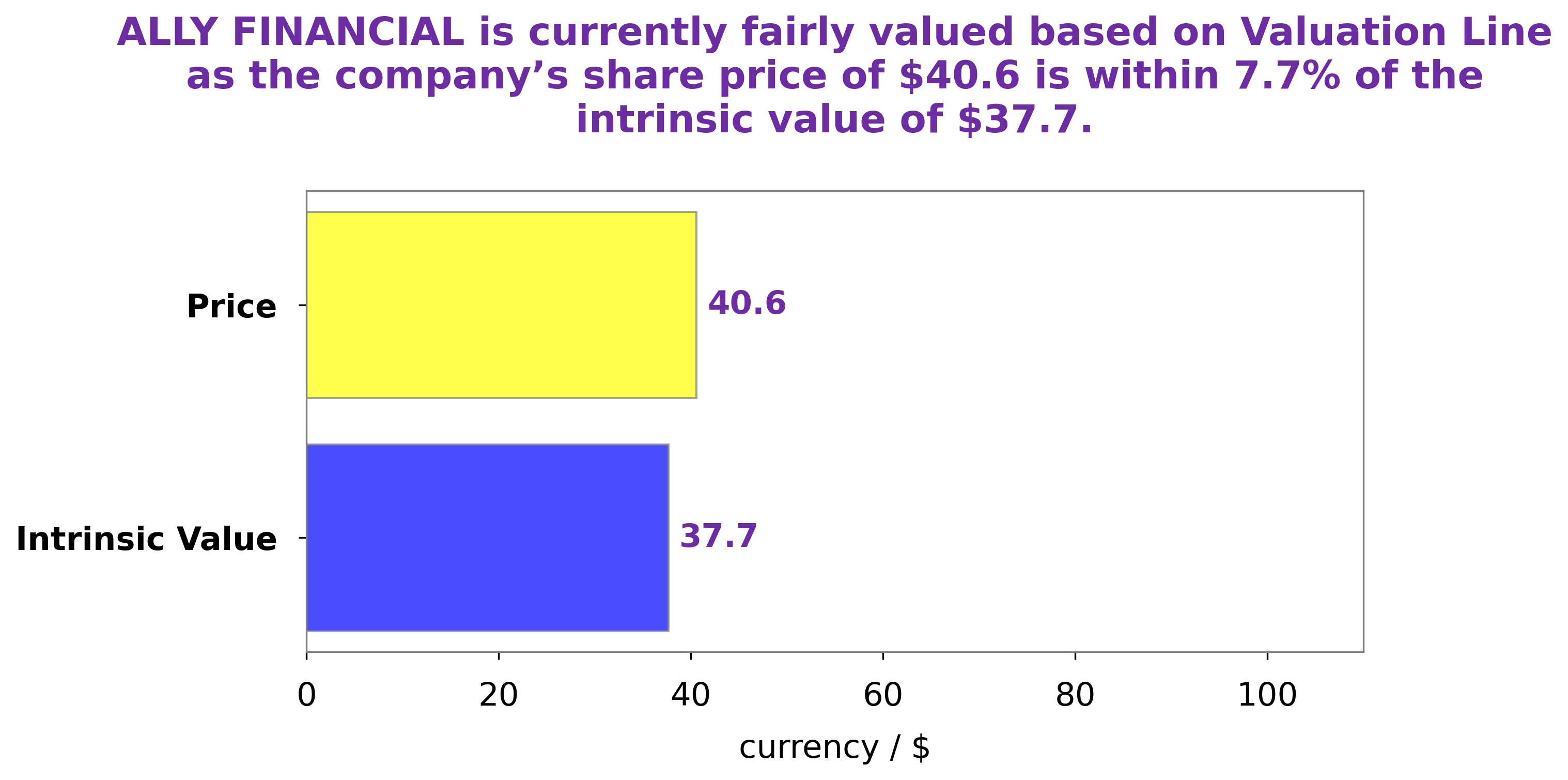

Is $50 a realistic target?

Some analysts are screaming that the stock is undervalued. Simply Wall St’s "Excess Returns" model puts the intrinsic value at $50.57. That’s about a 13.8% upside from where we are today.

But here’s the thing.

The market is currently pricing in a "soft landing." If the economy jitters and unemployment spikes, those auto loans become a liability fast. Right now, the "bears" point to the shrinking commercial auto loan portfolio—down nearly 6%. That’s a signal that dealerships aren't stocking up as aggressively as they used to.

On the flip side, the digital bank side of things is a fortress. People love Ally's platform. Their deposit base gives them a lower-cost way to fund those car loans compared to smaller competitors. That’s a massive competitive moat that doesn’t show up on a simple price chart.

💡 You might also like: 60 Pounds to USD: Why the Rate You See Isn't Always the Rate You Get

What you should actually do

Don't just stare at the daily tickers.

If you're already in, the 2.75% dividend is a nice "pay to wait" feature. If you're looking to buy, keep an eye on that $43.50 support level. If it breaks that, we might see $41 before the next leg up.

Next steps for your portfolio:

- Check the Earnings Beat: Watch the January 21st report. If the "Net Interest Margin" (NIM) expands even by a few basis points, it’s a green light for the bulls.

- Monitor Used Car Pricing: Indices like Manheim tell you the health of Ally's collateral. If used car prices crater, the stock price will likely follow.

- Set a Limit Order: Given the recent 4.6% pullback, setting a limit order near the $42.80 mark could capture a further "mini-dip" before the pre-earnings run-up.

- Diversify within Finance: If you're heavy on Ally, consider balancing with a "boring" big bank like JPMorgan to hedge against the specific risks of the auto-lending sector.

The Ally Financial stock price isn't going to double overnight. It’s a value play. It’s about a company that’s survived the "higher for longer" rate environment and is now coming out the other side with a very clean balance sheet. Just keep an eye on those delinquencies.