Money is weird. One day you’re looking at a bank balance in Manila and it feels like a fortune, but the second you try to move that cash into a US dollar account, the reality of global markets hits you square in the face. If you are sitting on 8 million PHP to USD, you aren't just looking at a simple math problem. You are dealing with the Bangko Sentral ng Pilipinas (BSP), the Federal Reserve’s hawkish stance on interest rates, and the annoying spread that banks hide in their exchange rates.

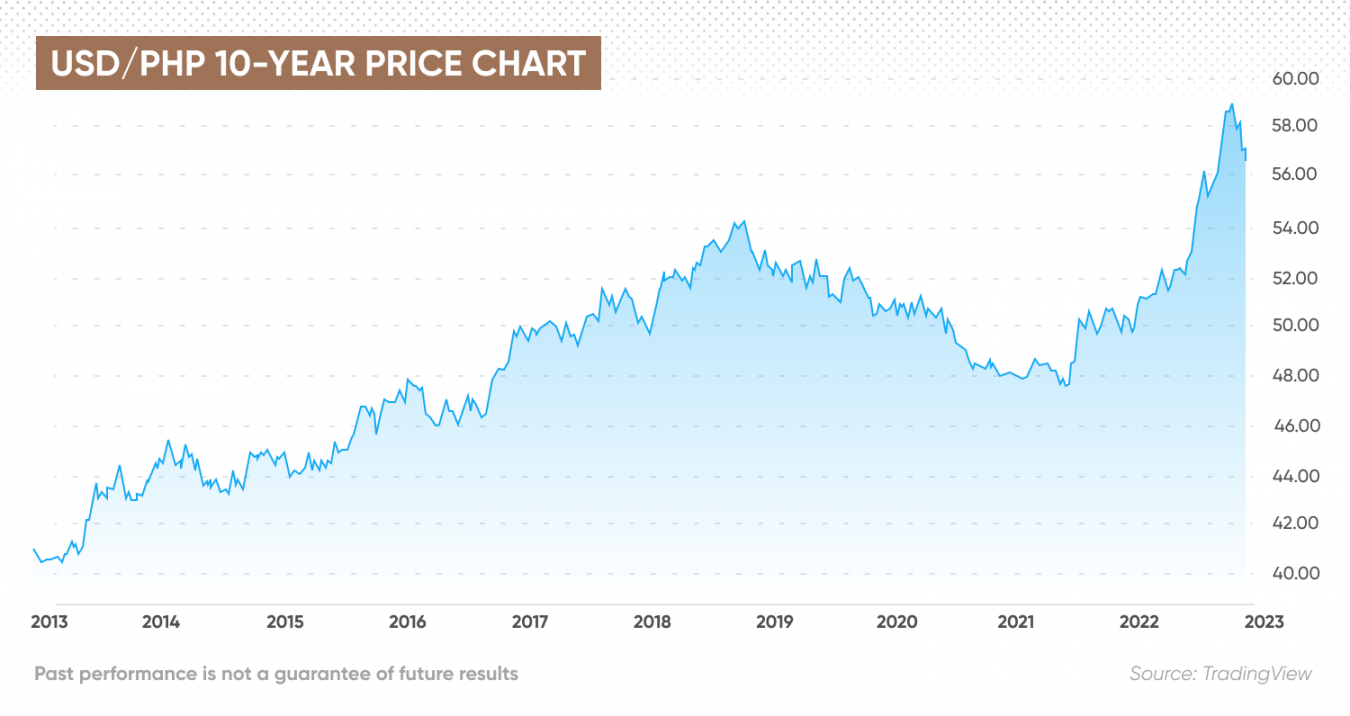

Let's get the raw math out of the way first. At the start of 2026, the Philippine Peso has been hovering around the 55 to 58 range against the Greenback. So, 8 million PHP to USD usually lands you somewhere between $138,000 and $145,000.

But wait.

If you go to a major bank like BDO or BPI and ask for that rate, they’ll laugh at you. Or rather, they’ll give you a "retail rate" that shaves off a couple of thousand dollars. That’s the first thing people get wrong about high-value currency conversion. They look at the mid-market rate on Google and think that's what they're getting. It isn't.

The Brutal Reality of the 8 Million PHP to USD Exchange

Why does the rate jump around so much? Honestly, it’s mostly about the "carry trade" and overseas Filipino workers (OFWs). When the US Federal Reserve keeps interest rates high, investors pull their money out of emerging markets like the Philippines and park it in US Treasuries. This makes the dollar stronger and your 8 million pesos worth less.

Then you have the holiday spikes. During Christmas or Easter, millions of Filipinos send money home. This massive influx of dollars being converted into pesos actually strengthens the PHP temporarily. If you are trying to convert 8 million PHP to USD during these windows, you might actually get a slightly better deal because the peso is in high demand locally.

Think about the scale here. We aren't talking about a vacation budget. $140,000 is a house in many parts of the US. It’s a Ferrari Roma. It’s a massive seed round for a tech startup in Cebu. When you move this much capital, a difference of just 50 centavos in the exchange rate translates to roughly 70,000 pesos—or about $1,200. That’s a lot of money to lose just because you picked the wrong day to click "transfer."

Where the Money Goes: Fees and "Hidden" Spreads

Most people use Western Union or Wise for small amounts. But for 8 million pesos? You’re entering the world of wire transfers and telegraphic transfers (TT).

Banks are notorious for this. They’ll tell you there is a "zero commission" fee. Don't believe them. They just bake the fee into the exchange rate. If the "real" rate is 56.00, they might offer you 56.80 when you're buying dollars. On an 8 million PHP to USD transaction, that "small" spread is a silent killer.

Real-World Purchasing Power: Manila vs. Los Angeles

Context matters. In Makati or BGC, 8 million pesos is significant. You could buy a high-end one-bedroom condo in a prime development like those by Ayala Land or Rockwell. You’re living the good life. You’ve got enough for a nice SUV and a few years of luxury expenses.

🔗 Read more: Why the Bay Haas Building in Mobile AL is the Talk of the City Right Now

Move that same value to the US? That $140,000 feels very different. In San Francisco or New York, that’s barely a down payment on a studio apartment. However, if you’re looking at real estate in the Midwest or parts of the South, you might still be able to buy a modest home outright. It’s a fascinating study in "lifestyle arbitrage." The moment you convert 8 million PHP to USD, you are effectively trading a "king-like" status in a developing economy for a "solid middle-class" status in a developed one.

Understanding the BSP’s Role

The Bangko Sentral ng Pilipinas doesn't just let the peso float freely. They practice what’s called a "managed float." If the peso starts dropping too fast against the dollar—making imports like oil and rice too expensive—the BSP will step in. They’ll sell off some of their US dollar reserves to buy up pesos and stabilize the price.

This is crucial for anyone holding 8 million pesos. You have to watch the inflation reports. If Philippine inflation is rampant, the BSP is pressured to raise interest rates. Higher rates usually mean a stronger peso. If you see the BSP getting aggressive, it might be worth holding onto your pesos a bit longer before flipping them to USD.

The Impact of Geopolitics

We can't ignore the South China Sea or the shifting alliances in Southeast Asia. Foreign direct investment (FDI) reacts to stability. When tensions rise, the "risk-off" sentiment takes over. Investors get scared, they sell their Philippine assets, and they move into the "safe haven" of the US dollar. In these moments, your 8 million PHP to USD conversion rate will tank.

I’ve seen traders lose 2% of their value in a single afternoon because of a headline. It's nerve-wracking.

How to Actually Convert Large Sums Without Getting Ripped Off

If you genuinely have 8 million pesos and need dollars, do not just walk into a bank branch. Talk to the manager. Ask for the "preferred" or "corporate" rate. For an amount this size, banks have leeway to tighten the spread.

- Check the Interbank Rate: Use platforms like Bloomberg or Reuters to see what the big banks are charging each other. This is your baseline.

- Avoid Weekends: Never convert currency on a Saturday or Sunday. Markets are closed, so providers add a "buffer" to protect themselves against price swings when markets open on Monday. This buffer comes out of your pocket.

- Look at Multi-Currency Accounts: Services like Wise or Revolut (if available in your region for these amounts) often provide much better rates than traditional brick-and-mortar banks like Metrobank or PNB.

- Tax Implications: Moving 8 million pesos across borders triggers AML (Anti-Money Laundering) flags. Be ready with your Source of Funds (SOF) documents. Whether it’s from a property sale, an inheritance, or business profits, you need a paper trail or the receiving bank in the US will freeze the funds.

The Psychology of the Exchange

There's a mental trap here. People wait for the "perfect" rate. They see the peso at 56 and think, "I'll wait for 54." Then it hits 58. Now they're paralyzed. They don't want to trade at 58 because they "missed" 56.

This is a gambler's fallacy. If you need the money in USD for a specific purpose—like tuition, a business investment, or a property closing—it’s often better to scale in. Convert 2 million pesos now, 2 million next week, and so on. This "dollar-cost averaging" protects you from the absolute worst spikes in the market.

The Future Outlook for the Peso

Looking ahead through 2026, the Philippine economy remains one of the faster-growing ones in Asia. However, it's heavily dependent on imported fuel. If global oil prices spike, the peso usually suffers. Conversely, the continued growth of the BPO (Business Process Outsourcing) sector provides a steady floor of dollar inflows.

Basically, the peso is a "high-beta" currency. It moves a lot. If the US economy enters a soft landing, the dollar might weaken, giving your 8 million pesos more "punch" when converted. If we see a global recession, expect the dollar to reign supreme, leaving your PHP stash looking a bit thinner.

Actionable Steps for Large Currency Transfers

- Verify the Mid-Market Rate: Check a reliable source to know the "true" value of 8 million PHP to USD before talking to any provider.

- Gather Your Documents: Ensure you have the Deed of Sale, Tax Returns, or Bank Statements ready to prove where the 8 million came from.

- Compare Three Providers: Get a quote from your primary bank, a secondary bank, and a digital specialized FX provider.

- Negotiate the Spread: Explicitly ask for a "tightened spread" based on the volume of the transaction.

- Watch the Calendar: Avoid major Philippine or US holidays when liquidity is low and volatility is high.

Moving 8 million pesos is a major financial event. Treat it with the technical respect it deserves. Don't let a bank's "convenience" cost you a year's worth of savings in hidden fees. Focus on the timing, the spread, and the documentation, and you'll come out on the other side with your capital intact.

***