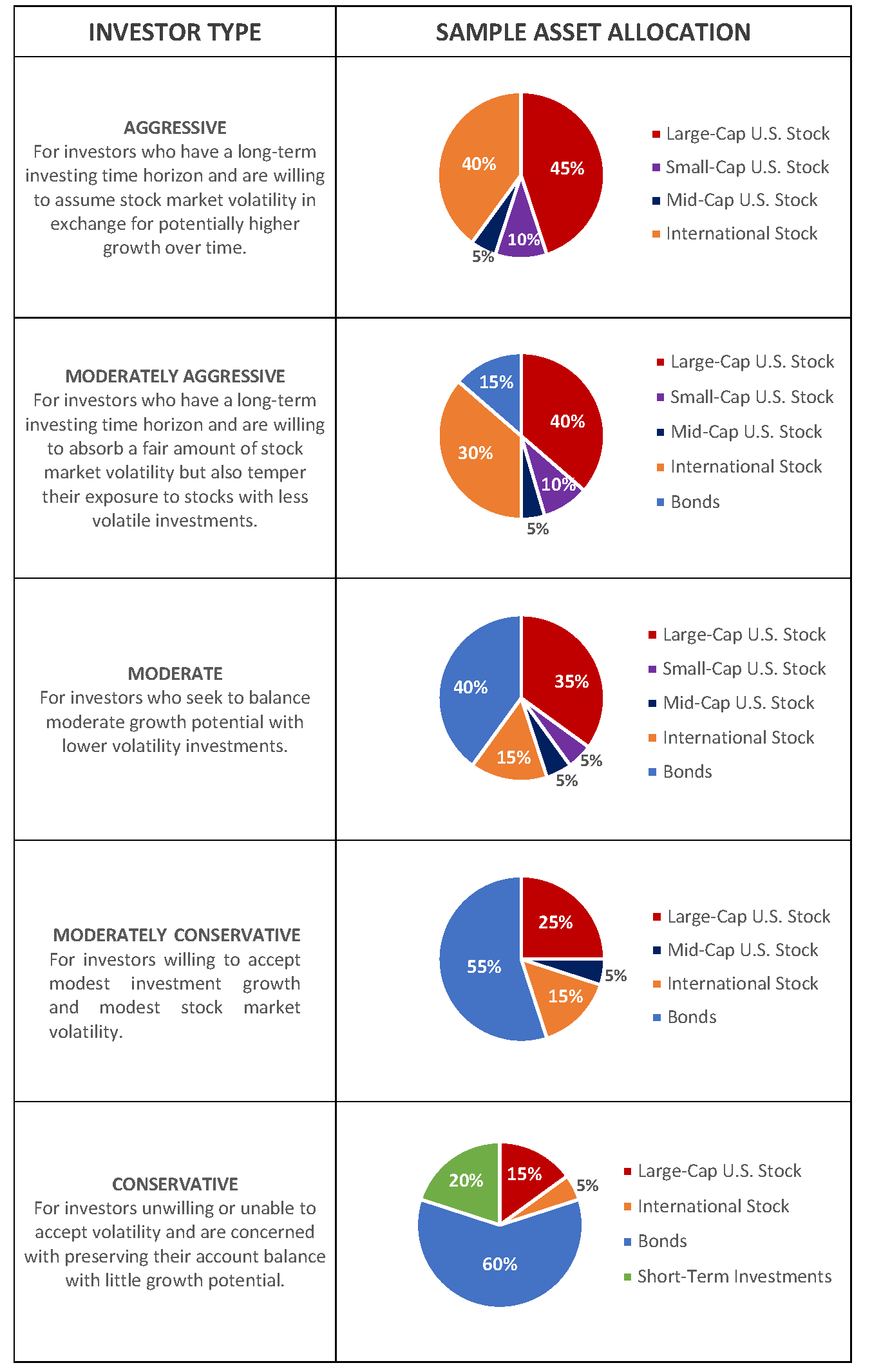

Look, nobody actually enjoys staring at a pie chart of their retirement account on a Tuesday night. It’s tedious. But the reality is that 401k asset allocation by age is basically the only lever you have that actually moves the needle over thirty years, other than how much cash you're physically shoving into the account. Most people just click the "Target Date Fund" button and hope for the best.

Sometimes that works. Often, it doesn't.

Asset allocation isn't some static "set it and forget it" thing, even though Wall Street tries to sell it that way. It’s about risk capacity. Not just how much risk you think you can stomach when the market is green, but how much your timeline can actually handle when the S&P 500 decides to take a 20% haircut in a single month. If you’re 25, a market crash is a clearance sale. If you’re 64 and retiring in six months? That same crash is a structural threat to your ability to buy groceries in ten years.

The Rule of 100 (And Why It’s Kinda Broken)

You’ve probably heard the old-school math. Subtract your age from 100, and that’s the percentage of stocks you should own. If you’re 40, you keep 60% in stocks and 40% in bonds.

Honestly? That’s way too conservative for 2026.

We’re living longer. Inflation is stickier than it used to be. Many experts, including those at Vanguard and BlackRock, have started suggesting the "Rule of 110" or even 120. If you follow the Rule of 100 at age 30, you’re putting 30% of your money into bonds. In a world where equities have historically outperformed fixed income by a massive margin over long horizons, that 30% bond allocation is basically a tax on your future wealth. You're trading huge potential gains for "safety" you don't actually need yet.

Your 20s: The Era of Pure Aggression

When you're in your 20s, time is your greatest asset. You have what economists call high "human capital" (decades of future earnings) and low "financial capital."

Because you won't touch this money for 40 years, your 401k asset allocation by age should be heavily skewed toward equities. We're talking 90% to 100% stocks. Some people get jittery seeing their $5,000 balance drop to $3,500, but in the grand scheme? It doesn't matter. You want volatility. Volatility is the price you pay for the returns that compound into a million-dollar nest egg.

Focus on low-cost index funds. Total Stock Market or S&P 500 funds are the bread and butter here. Maybe throw in 15-20% international exposure because, let’s face it, the U.S. won’t always be the only game in town. Avoid "thematic" funds like AI-only or Green Tech ETFs in your 401k. They’re too concentrated. You want the whole haystack, not the needle.

✨ Don't miss: Wells Fargo Says CFPB Has Terminated Its 2022 Sentences: What It Really Means for You

The 30s and 40s: The "Messy Middle" of Allocation

This is where things get complicated. You probably have a mortgage. Maybe kids. Your 401k balance is starting to look like actual money—maybe it’s six figures now. When you see a 10% dip on a $200,000 balance, that’s $20,000 vanishing. That hurts more than the $1,500 dip you felt in your 20s.

But here is the kicker: You still have 20 to 30 years left.

Most people start getting defensive too early. They see a big number and want to protect it. That’s a mistake. If you shift to a 50/50 stock-bond split at age 42, you are severely handicapping your growth during your peak earning years.

A realistic 401k asset allocation by age for a 40-year-old might look like:

- 70% U.S. Large Cap/Total Market

- 15% International Developed Markets

- 5% Emerging Markets

- 10% Total Bond Market or TIPS (Treasury Inflation-Protected Securities)

Bonds are finally paying something again, thanks to the rate hikes we've seen over the last few years. But they are still there for stability, not growth. Think of them as the ballast on a ship. They won't make the ship go faster, but they keep it from tipping over when the waves get choppy.

The Danger of "Lifestyle Creep" in Your Portfolio

It's easy to think you're diversified because you own five different funds. But if those five funds all hold Apple, Microsoft, and Nvidia as their top three holdings, you aren't diversified. You're just overlapping. This is a common trap in 401k plans where the "Growth Fund," the "Large Cap Fund," and the "S&P 500 Index" are basically the same thing under different names.

Check your "overlap." If your 401k provider has a tool like Morningstar’s X-Ray, use it. You might find that 40% of your entire net worth is tied up in five tech companies. That’s fine when tech is booming, but it’s a nightmare when the sector rotates.

The 50s: The Glide Path Begins

Now we’re talking about the "Red Zone." This is the 5-10 years before retirement and the 5 years after. This is where 401k asset allocation by age becomes a matter of survival.

Ever heard of "Sequence of Returns Risk"?

It’s the risk that the market crashes right as you start taking withdrawals. If you retire with $1 million and the market drops 20% in Year 1, you don't just lose $200,000. You're also forced to sell shares at the bottom to pay your bills. That can spiral a portfolio into a death loop from which it never recovers.

✨ Don't miss: How to refund in PayPal: The simple truth about getting your money back

By age 55, you should probably be looking at a 60/40 or 65/35 split. You’re building a "cash bucket" or a bond ladder. The goal is to have 2-3 years of living expenses in very safe, liquid assets (like a Money Market Fund or Short-term Treasuries) so that if the stock market pukes, you don't have to sell your stocks at a loss. You just live off the cash until things settle down.

Why Target Date Funds Might Be Sabotaging You

Target Date Funds (TDFs) are the most popular way people handle 401k asset allocation by age. You pick the "2050 Fund" and it automatically shifts from stocks to bonds as you get older.

Sounds great, right?

The problem is that TDFs are "one size fits all." They don't know if you have a massive pension. They don't know if you’re planning to work until you're 75. They don't know if you have a rental property bringing in $3,000 a month.

If you have a guaranteed pension, your 401k can actually afford to be more aggressive because your "bond-like" income is already covered by the pension. If you use a TDF, it might be shifting you into bonds you don't need, which kills your upside. You have to look at your whole picture, not just the 401k in a vacuum.

The 60s and Beyond: It’s Not Just About Bonds

Retirement doesn't mean you stop investing. If you retire at 65, you might live until 95. That’s a 30-year investment horizon. You cannot afford to be 100% in bonds or CDs. You’ll lose all your purchasing power to inflation.

A common strategy now is the "Bucket Method."

- Bucket 1: 2 years of cash/cash equivalents for immediate spending.

- Bucket 2: 5-7 years of bonds and income-producing assets.

- Bucket 3: The rest in stocks for long-term growth.

As you spend from Bucket 1, you refill it with gains from Bucket 3 or interest from Bucket 2. This creates a psychological buffer. When the news says the Dow is down 800 points, you can tell yourself, "That’s okay, my spending money for the next two years is sitting in a boring savings account. I can wait for the market to recover."

🔗 Read more: The Lady Boss From Betrayal to Beloved: Why This Workplace Evolution Is Actually Happening

Real World Nuance: The Tax Man Cometh

Your 401k asset allocation by age should also consider the type of account you're using. Is it a Traditional 401k or a Roth 401k?

In a Roth, you’ve already paid the taxes. Every dollar of growth is yours to keep. Generally, you want your highest-growth assets (stocks) in your Roth accounts and your lower-growth assets (bonds) in your Traditional accounts. Why? Because when you eventually withdraw from the Traditional 401k, the government takes a cut of every dollar. You’d rather they take a cut of a smaller "bond" pie than a massive "tech stock" pie.

Specific Asset Classes to Watch

Don't just think "Stocks" vs "Bonds." There are sub-layers.

Small Cap Value: Historically, small companies that are undervalued have outperformed the S&P 500 over very long periods, though they can go through decade-long droughts. Adding 5-10% here can juice returns for younger investors.

REITs (Real Estate Investment Trusts): Many 401ks offer a real estate fund. These are great for diversification because they don't always move in lockstep with the stock market. Plus, they pay dividends.

International: Don't ignore the world. Western Europe, Japan, and emerging markets like India offer different growth profiles.

Actionable Steps for Your 401k Today

Stop overthinking and start auditing. Here is how you actually fix your allocation without hiring a guy in a suit who charges you 1% of your net worth.

1. Log in and check your "Expense Ratios."

If you are paying more than 0.50% for any fund in your 401k, you’re probably getting ripped off. Look for the "Index" versions of those funds. An S&P 500 index fund should cost you around 0.03% to 0.10%. Over 30 years, that fee difference can be worth six figures.

2. Rebalance once a year.

If your goal is 80% stocks and 20% bonds, and the stock market has a huge year, you might end up at 85/15. This means you are now riskier than you intended to be. Sell some stocks (at a high!) and buy some bonds (at a low). This forces you to "buy low, sell high" automatically.

3. Adjust for your personal "Sleep Factor."

The math might say you should be 100% stocks, but if you're going to panic-sell during a recession, then 100% stocks is the wrong allocation for you. An imperfect portfolio you stick with is infinitely better than a "perfect" portfolio you abandon when things get scary.

4. Check your beneficiary designations.

This has nothing to do with asset allocation, but honestly, people forget it all the time. If you got divorced or your situation changed, make sure the money is actually going to the right person.

5. Increase your contribution by 1% today.

Allocation matters, but the savings rate is the engine. If you're 30 and you increase your contribution from 6% to 7%, the compounding effect of that 1% over 35 years is staggering.

Investing is mostly about managing your own psychology. Your 401k asset allocation by age is just a framework to keep you from doing something stupid when the market gets emotional. Keep it simple. Keep the fees low. Stay the course.