Math isn't always fun. Honestly, for most of us, it’s just a hurdle between where we are and where we want to be financially. But when you start talking about five-figure sums, like 40,000, that percentage isn't just a homework problem anymore. It's real money. It's a down payment. It's a tax bill. It's a massive discount on a luxury car that’s been sitting on the lot too long. So, let’s just get the answer out of the way first: 30 percent of 40000 is 12,000.

That’s a big number.

Think about it. If you’re looking at a $40,000 annual salary and someone says you’re losing 30% to taxes, benefits, and retirement, you’re looking at $12,000 out the door. You’re left with $28,000. That hurts. Or, if you’re a business owner with $40,000 in monthly revenue and your overhead is 30%, you're spending $12,000 just to keep the lights on and the staff paid before you even see a dime of profit. Understanding this specific calculation is vital because, in the world of finance, 30% is often used as a "golden rule" or a red-line threshold for everything from housing costs to debt-to-income ratios.

How to Calculate 30 Percent of 40000 Without Losing Your Mind

You don't need a PhD. You don't even really need a calculator if you know the shortcuts. Most people overcomplicate percentages because they try to do the whole thing at once. Don’t do that.

The easiest way to find 30% of any number is the 10% method. It’s basically a mental trick. To find 10% of 40,000, you just move the decimal point one spot to the left. Take 40,000.0 and jump that dot over. Now you have 4,000. That is 10%. Easy, right? Since 30% is just three times that amount, you just do $4,000 \times 3$.

Boom. $12,000$.

If you’re a fan of the "old school" way they taught us in middle school—the stuff that actually stuck—you can use the decimal multiplication method. You turn 30% into 0.30. Then you multiply: $40,000 \times 0.30 = 12,000$. It works every single time, whether you're calculating a commission on a $40,000 sales deal or trying to figure out how much of a $40,000 inheritance is going to the government.

✨ Don't miss: Cox Tech Support Business Needs: What Actually Happens When the Internet Quits

Why 30% is the Magic Number in Your Budget

Budgeting experts like Elizabeth Warren (who popularized the 50/30/20 rule) often point to 30% as the "wants" category. But more traditionally, financial institutions look at 30% as the limit for housing.

If you make $40,000 a year, banks generally don't want your mortgage or rent to exceed 30% of your gross income. That means your housing ceiling is $12,000 a year, or exactly $1,000 a month. In a lot of cities today, $1,000 a month for rent is a pipe dream. This is where the math gets messy. When your housing creeps up to 40% or 50%, that 30 percent of 40000 becomes a ghost—money you should have had for other things but had to dump into a roof over your head.

The Tax Reality of $40,000

Let's talk about the IRS. If you're a freelancer or an independent contractor in the United States, a common piece of advice is to set aside 30% of your gross income for taxes. It’s a safe bet. It covers your federal income tax, the self-employment tax (which is a hefty 15.3% on its own), and usually leaves a little cushion for state taxes.

If you land a contract worth $40,000, you cannot—I repeat, cannot—spend all of it. If you do, come April, you are going to be in a world of hurt. You need to take that $12,000 and move it into a high-yield savings account immediately. It’s not your money. It’s the government’s money that you’re just holding onto for a while. Seeing $40,000 in your bank account feels like winning the lottery, but knowing that 30 percent of 40000 is 12,000 keeps you from making a massive financial blunder.

Business Margins and the 30% Threshold

In the world of retail and SaaS (Software as a Service), margins are everything. If you’re running a business and your cost of goods sold (COGS) is 70%, your gross margin is 30%.

On a $40,000 project, a 30% margin means you’ve cleared $12,000 after paying for materials and direct labor. For many industries, a 30% margin is actually considered quite healthy. However, if you're in consulting, you might find that 30% is actually on the low side. Many high-end consultants aim for 50% to 70% margins.

🔗 Read more: Canada Tariffs on US Goods Before Trump: What Most People Get Wrong

But let’s look at the flip side: debt.

If you have $40,000 in total available credit across all your credit cards, and you’ve spent $12,000, your credit utilization is exactly 30%. This is a huge deal for your credit score. FICO and other scoring models love to see utilization at 30% or lower. Once you cross that $12,000 mark on a $40,000 limit, your credit score might start to take a dip. It’s a weird psychological barrier that lenders use to judge how "risky" you are.

Real World Examples of $12,000 (30% of $40k)

Numbers are abstract until you put them into context. What does $12,000 actually look like in 2026?

- A Solid Used Car: You can still find a very reliable 5-to-7-year-old sedan for twelve grand.

- A Luxury Vacation: A family of four can do a pretty spectacular two-week trip to Europe or Japan for $12,000 if they aren't flying first class.

- Emergency Fund: For most single people, $12,000 covers 3 to 6 months of living expenses.

- The "Gap" in College Tuition: If a state school costs $25,000 a year and you have $13,000 in scholarships, that 30% of a $40,000 total four-year bill is what you're scrambling to find.

Common Misconceptions About Calculating Percentages

People often get confused when they try to "reverse" the math. For example, if you have $40,000 and it increases by 30%, you don't just have $12,000. You have $52,000.

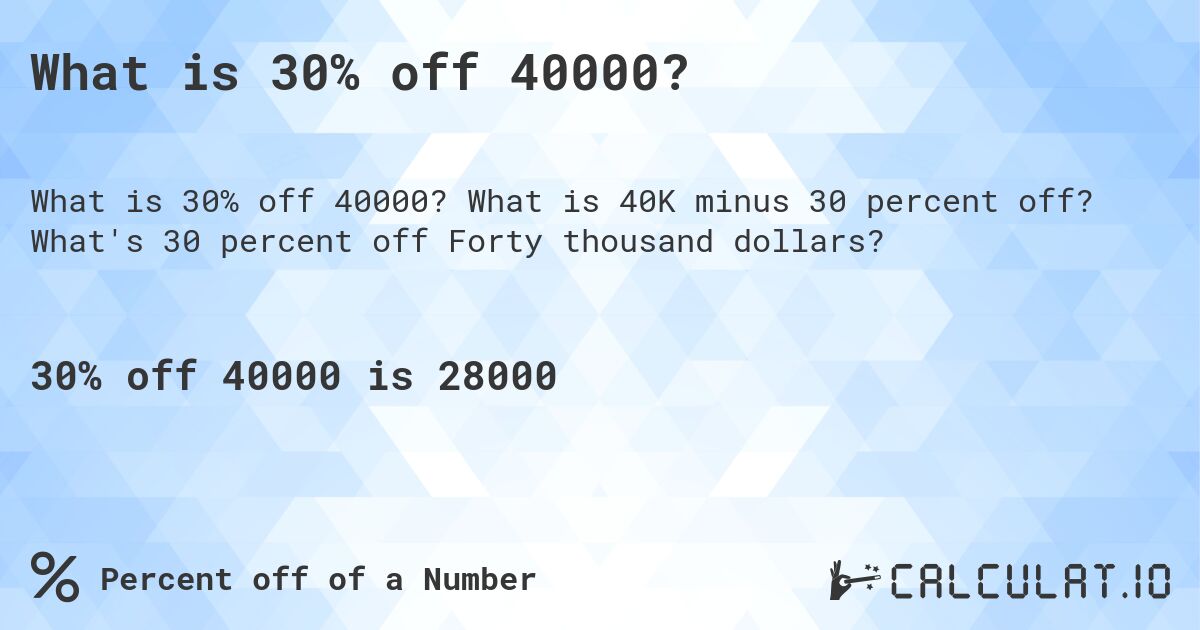

But if you have $40,000 and it decreases by 30%, you’re down to $28,000.

The most common mistake? Calculating 30% and then forgetting to subtract or add it back to the original sum depending on the context. If a store says "30% off" a $40,000 item (maybe a high-end watch or a tractor), the $12,000 is your savings, not your price tag. You're still paying $28,000. Don't let the excitement of a "12,000 discount" blind you to the fact that you're still dropping nearly thirty grand.

💡 You might also like: Bank of America Orland Park IL: What Most People Get Wrong About Local Banking

Actionable Steps for Managing a $12,000 Sum

Whether you just saved it, owe it, or need to invest it, here is how you should handle that 30% chunk of $40,000.

1. The "Tax Bucket" Strategy

If that $12,000 is for taxes, do not keep it in your checking account. Use a separate bank—literally a different institution—to remove the temptation. Look for a high-yield savings account (HYSA) that’s currently yielding 4% or 5%. Over a year, that $12,000 tax obligation could earn you an extra $500 to $600 in interest. That's a free car payment or a nice dinner just for being organized.

2. The Credit Score Pivot

If you have $40,000 in debt and you're trying to figure out your first milestone, aim for the 30% mark. Getting your debt down to $12,000 (if you started higher) or keeping it below $12,000 (if you have high limits) is the single fastest way to manipulate your credit score upward.

3. Investment Compounding

If you invest $12,000 (the 30%) and leave it alone in a total stock market index fund for 20 years at a 7% average return, it grows to about $46,000. Think about that. The 30% "slice" eventually becomes larger than the original $40,000 "pie." This is why understanding these numbers early matters.

4. Negotiation Leverage

When you’re negotiating a $40,000 salary or contract, and you want a raise, asking for "30% more" sounds way more aggressive than asking for $12,000, even though they are the same thing. Conversely, if you're a freelancer and a client asks for a discount, knowing that a 30% haircut takes you from $40k to $28k helps you realize how much work you’re actually giving away for free.

Calculating 30 percent of 40000 is a simple math problem, but the implications of that $12,000 figure reach into almost every corner of your financial life. From the rent you pay to the taxes you owe, that 30% slice is often the difference between being "in the black" or "in the red." Keep that 10% trick (moving the decimal) in your back pocket, and you'll never be caught off guard in a negotiation or a budget meeting again.