Money talk is usually pretty dry, but if you’re staring at your 2024 returns right now, it suddenly feels a lot more personal. Most couples I talk to think that if they "land" in a specific tax bracket, every single dollar they earned is taxed at that high rate.

That's just not how it works.

The IRS uses a progressive system. Think of it like a series of buckets. You fill the 10% bucket first. When that's full, you move to the 12% bucket. You only pay the higher rate on the money that spills over into the next one. Understanding the 2024 federal income tax brackets married filing jointly is basically about knowing how big those buckets are and which one you’re currently pouring money into.

The 2024 Numbers You Actually Need

For the 2024 tax year—the one you're likely dealing with in early 2026—the IRS adjusted the thresholds by about 5.4% to account for inflation. This was actually a good thing for most of us. It meant you could earn more money without being pushed into a higher bracket, a phenomenon tax nerds call "bracket creep."

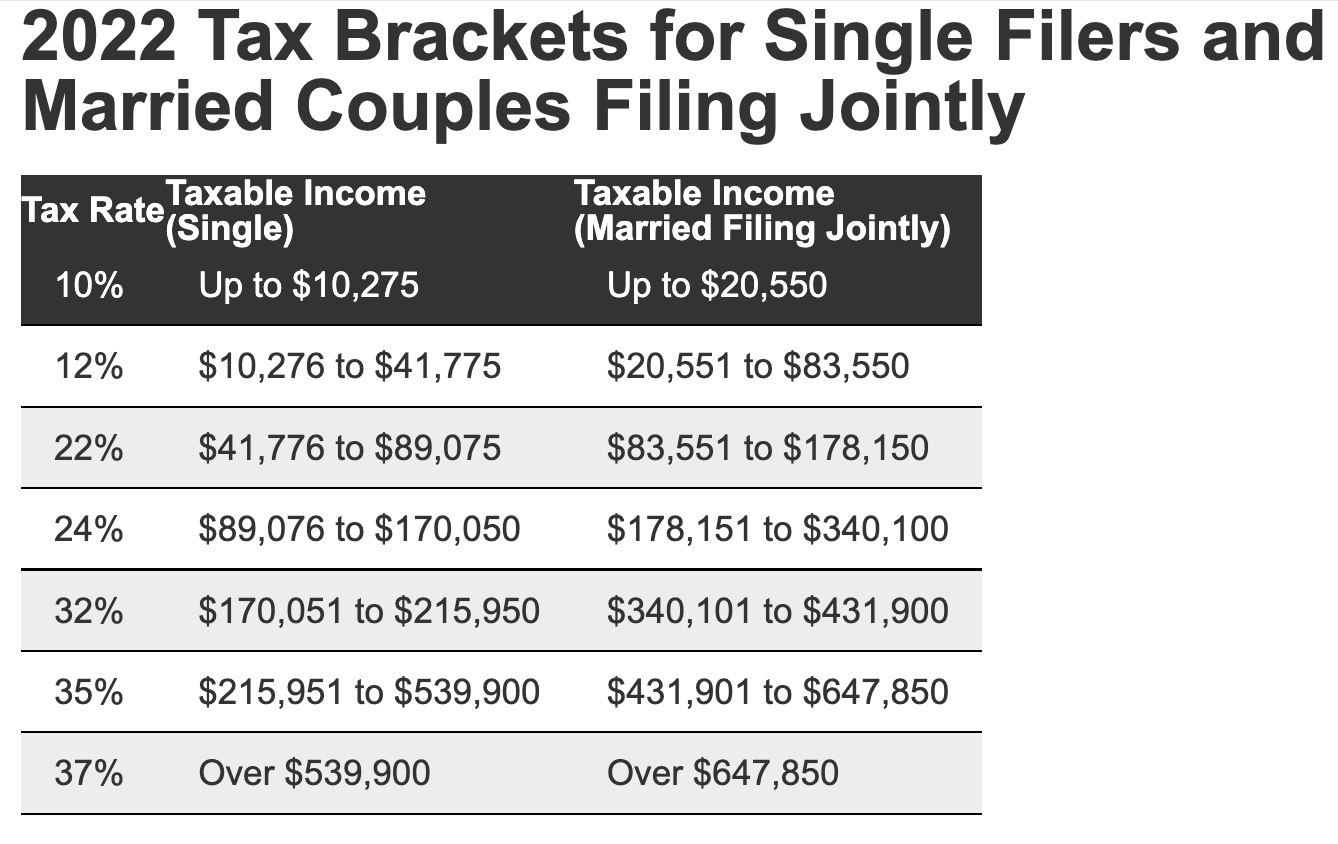

If you’re married and filing a joint return, here is how the rates break down for your taxable income:

You’ll pay 10% on everything from $0 up to $23,200.

Once you cross that, the 12% rate kicks in for income between $23,201 and $94,300.

🔗 Read more: Price of Tesla Stock Today: Why Everyone is Watching January 28

If you're doing well and your taxable income is between $94,301 and $201,050, that portion is taxed at 22%.

Moving up, the 24% bracket covers income from $201,051 to $383,900.

The 32% tier starts at $383,901 and goes to $487,450.

For the high earners, the 35% rate applies to income between $487,451 and $731,200.

And finally, anything over $731,200 is hit with the top 37% rate.

Standard Deductions: The "Invisible" Income

Before you even look at those brackets, you have to subtract your deductions. Most people take the standard deduction because, honestly, it’s huge now. For 2024, the standard deduction for married couples filing jointly is $29,200.

💡 You might also like: GA 30084 from Georgia Ports Authority: The Truth Behind the Zip Code

Basically, if you and your spouse together earned $100,000 in 2024, you don't start paying taxes on $100,000. You subtract that $29,200 first. That leaves you with $70,800 in taxable income.

That $70,800 is what actually matters for the brackets. In this example, you wouldn’t even touch the 22% bracket. You’d be firmly in the 12% tier. It's a massive difference.

The Effective Rate vs. The Marginal Rate

This is where people get confused. Your "marginal" rate is the highest bracket your last dollar fell into. If your taxable income is $100,000, your marginal rate is 22%.

But your "effective" rate is the actual percentage of your total income that goes to the IRS. Because your first $23,200 was only taxed at 10%, your overall average—your effective rate—is much lower than 22%.

I've seen couples stress out because a $5,000 bonus "pushed them into the next bracket." They think their whole salary is now being taxed more. Nope. Only that $5,000 bonus is being taxed at the new, higher rate. You still keep the vast majority of that money.

Why Filing Jointly Usually Wins (But Not Always)

Most of the time, filing jointly is a slam dunk. The brackets for joint filers are exactly double the brackets for single filers in the lower tiers. It’s designed to be fair.

📖 Related: Jerry Jones 19.2 Billion Net Worth: Why Everyone is Getting the Math Wrong

However, there are "marriage penalties" that still exist in the very high-income ranges or when both spouses earn very high, similar salaries. For instance, the 37% bracket for joint filers starts at $731,200, but for two single people, it would start at $609,350 each ($1,218,700 combined). If you’re both pulling in $500,000, you might actually pay more as a married couple than you would as two single people. Kinda weird, right?

There are also specific situations involving student loan repayments (like IBR plans) where filing separately might save you more on the loan side than you lose on the tax side. It's rare, but it happens.

Strategies to Stay in a Lower Bracket

If you realize you’re just a few thousand dollars into the 22% or 24% bracket, you can actually pull yourself back down.

- 401(k) and 403(b) Contributions: This is the easiest way. If you put money into a traditional 401(k), the IRS acts like you never earned it. It lowers your taxable income dollar-for-dollar.

- HSA Funding: If you have a high-deductible health plan, the Health Savings Account is a "triple-threat" tax advantage. It reduces your taxable income now, grows tax-free, and stays tax-free when you spend it on healthcare.

- Charitable Giving: If you itemize (meaning your deductions total more than $29,200), those year-end donations to your favorite non-profit aren't just good for the soul—they’re good for the bottom line.

Actionable Next Steps for Your 2024 Filing

First, pull your W-2s and 1099s. Don't guess.

Second, calculate your "Adjusted Gross Income" (AGI). This is your total income minus those "above-the-line" deductions like 401(k) contributions or student loan interest.

Third, subtract your standard deduction ($29,200) or your itemized deductions.

Now, look at the 2024 federal income tax brackets married filing jointly again. Find where that final number sits. If you’re right on the edge of a higher bracket, you can’t change your 401(k) contributions for 2024 anymore—that ship sailed on December 31st. But, you might still be able to contribute to a traditional IRA or an HSA until the tax deadline in April 2025 to lower that 2024 taxable income.

Check with a CPA if your situation involves business income or complex investments, but for the average couple, knowing these levels is the best way to stop overpaying and start planning.